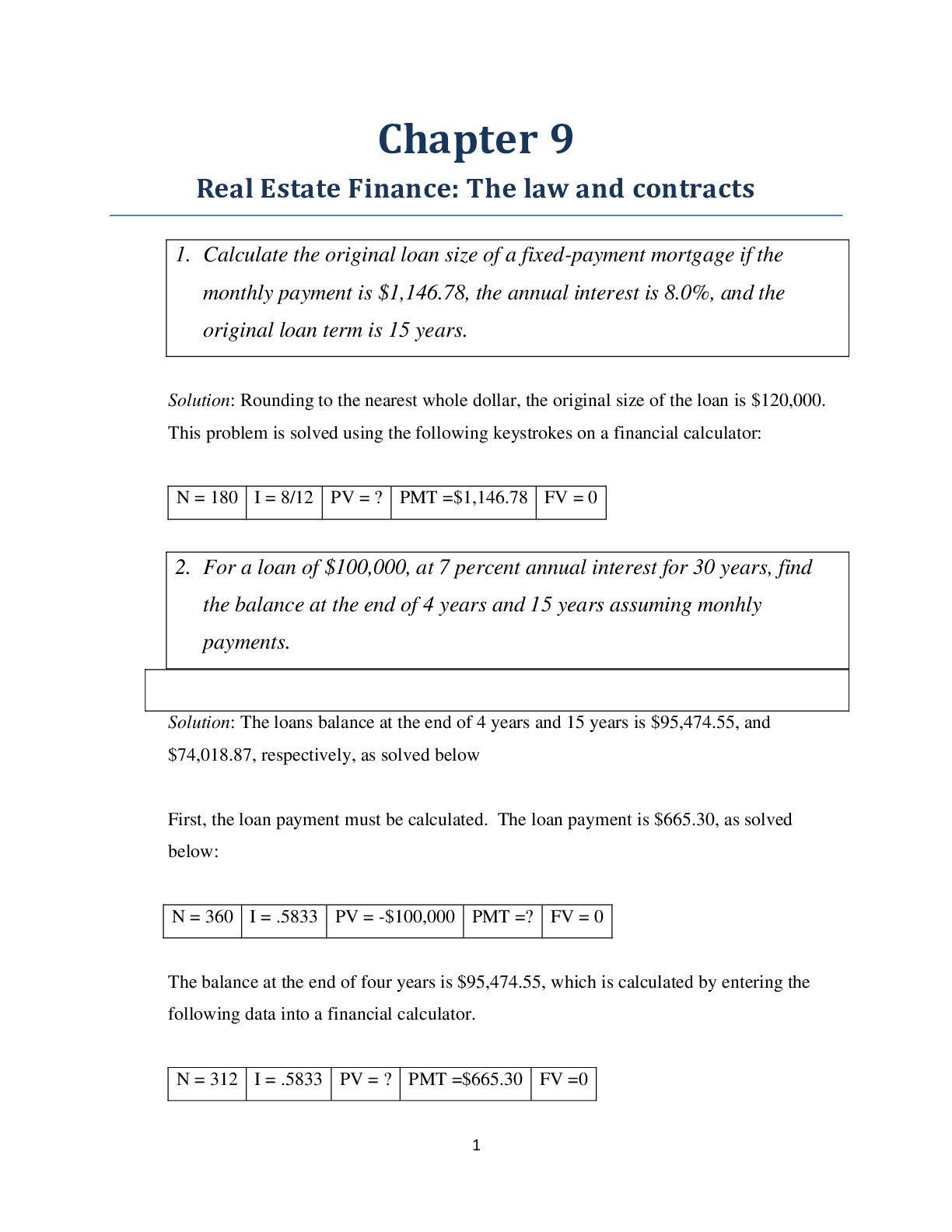

Finance > QUESTIONS & ANSWERS > FSA3e Test BankB Mod14 091712. Module 14 Operating-Income-Based Valuation (All)

FSA3e Test BankB Mod14 091712. Module 14 Operating-Income-Based Valuation

Document Content and Description Below

Learning Objectives – coverage by question True/False Multiple Choice Exercises Problems Essays LO1 – Define equity valuation models and explain the information required to value equity secur... ities. 1 1, 2 LO2 – Describe and apply the residual operating income model to value equity securities. LO3 – Explain how equity valuation models can aid managerial decisions. Test Bank, Module 14 14-1Module 14: Operating-Income-Based Valuation True/False Topic: Weighted Average Cost of Capital LO: 2 1. The weighted average cost is computed as: WACC=(rd × % of debt) + (re × % of net income) Answer: False Rationale: Discount rate WACC = (rd × % of debt) + (re × % of equity) Topic: RNOA, WACC, and Company Value LO: 2 2. All else equal, when WACC is higher than RNOA, the company’s market value is increasing. Answer: False Rationale: For a given level of NOA, company value increases when RNOA > WACC. Topic: Residual Operating Income (ROPI) Valuation Model LO: 2 3. Differing accrual accounting policies have an impact on the estimated value of equity when using the ROPI model. Answer: False Rationale: Expected ROPI offsets different levels of NOA resulting from differing accounting policies, leaving estimated value unaffected by accounting policies. Topic: Company Value under ROPI Model LO: 2 4. The residual operating income (ROPI) model estimates firm value as the current book value of net operating assets plus the present value of expected residual operating income. Answer: True Rationale: The ROPI model estimates firm value as the current book value of net operating assets plus the present value of expected ROPI. Topic: ROPI Valuation Model LO: 2 5. The residual operating income (ROPI) model focuses on net income which is a more accurate measure of future profitability than expected cash flows. Answer: False Rationale: NOPAT is the key value driver of the ROPI model. ©Cambridge Business Publishers, 2013 14-2 Financial Statement Analysis & Valuation 3rd EditionTopic: Insights from ROPI Model LO: 3 6. The power of the residual operating income (ROPI) model is that it allows managers to focus on either the income statement or balance sheet to increase firm value. Answer: False Rationale: The ROPI model focuses managers’ attention on both the income statement and the balance sheet. Test Bank, Module 14 14-3Multiple Choice Topic: Earnings and Equity Values LO: 1 1. On April 24, 2009, Ford Motor Company reported a net loss of $1.4 billion for the fiscal quarter. That day, Ford’s stock price climbed from $4.49 per share to $5.00. This demonstrates that: A) Equity valuation models are not related to company earnings B) Dividends are unrelated to earnings C) Equity valuation models can be irrational D) The net loss was smaller than investors expected E) All of the above Answer: D Rationale: Equity valuation models are based on expected future earnings. The loss that Ford reported was less than investors expected, so in a way, it was good news. Topic: Projecting Revenue One Year Out – Numerical calculations required LO: 2 2. Following is information from Morse Inc. for 2012. Total 2012 revenue $219,138 Total revenue growth rate 17.9% Terminal revenue growth rate 7.1% Net operating profit margin (NOPM) 9.8% Net operating asset turnover (NOAT) 2.12 Projected 2013 total revenue would be: A) $258,364 B) $234,696 C) $185,868 D) $240,614 E) None of the above Answer: A Rationale: $219,138 × 1.179 = $258,364 14-4 Financial Statement Analysis & Valuation 3rd EditionTopic: Projecting Net Operating Profit After-Tax (NOPAT) – Numerical calculations required LO: 2 3. Following is information from Hewlett Packard for 2011 ($ in millions). Total revenue $127,245 Projected revenue growth rate 1.0% Net operating profit margin (NOPM) 5.9% Net operating assets (NOA) $62,249 Net operating asset turnover (NOAT) 2.04 Projected net operating profit after tax (NOPAT) for 2012 is: A) $7,583 million B) $7,950 million C) $3,684 million D) $8,258 million E) None of the above Answer: A Rationale: $127,245 million × 1.01 × 0.059 = $7,583 million Topic: Projecting Net Operating Profit After-Tax (NOPAT) – Numerical calculations required LO: 2 4. Following is information from American Eagle Outfitters for 2011 ($ in thousands). Total revenue $3,159,818 Total revenue growth rate 6.5% Net operating profit margin (NOPM) 4.7% Net operating profit after tax (NOPAT) $148,063 Net operating asset turnover (NOAT) 4.16 Projected net operating assets (NOA) for 2012 is: A) $ 795,272 thousand B) $ 716,001 thousand C) $1,253,293 thousand D) $ 808,944 thousand E) None of the above Answer: D Rationale: $3,159,818 thousand × 1.065 / 4.16 = $808,944 thousand 3 Test Bank, Module 14 14-5Topic: Net Operating Profit After-Tax LO: 2 5. Which of the following items should not be included in net operating profit after tax (NOPAT)? A) Revenue B) Cost of Goods Sold C) Selling, General & Administrative Expenses D) Decrease in Accounts Receivable E) None of the above Answer: D Rationale: Accounts Receivable is an asset and is not included in the calculations of NOPAT. Reductions in accounts receivable are a component of the statement of cash flows. Topic: ROPI Valuation Model LO: 2 6. Which of the following descriptions of the residual operating income (ROPI) model is inaccurate? A) ROPI analysis focuses on the amount by which shareholder value is created during a period. B) ROPI is positive when NOPAT is higher than WACC × NOABeg. C) ROPI is useful as a management tool as it forces managers to pay attention to both the income statement and the balance sheet. D) One critique of the ROPI model is that it focuses managers’ attention solely on short-term operating assets and neglects investment in long-term operating assets. E) None of the above Answer: D Rationale: ROPI= NOPAT- (WACC × NOABeg) NOA is the book value of all net operating assets at the beginning of the current period. This includes current and long-term operating assets. Managers must, therefore, focus on both short-term and long-term operating assets. [Show More]

Last updated: 1 year ago

Preview 1 out of 25 pages

.png)

Buy this document to get the full access instantly

Instant Download Access after purchase

Add to cartInstant download

We Accept:

Reviews( 0 )

$15.00

Document information

Connected school, study & course

About the document

Uploaded On

Apr 30, 2022

Number of pages

25

Written in

Additional information

This document has been written for:

Uploaded

Apr 30, 2022

Downloads

0

Views

77