Financial Accounting > TEST BANK > Certified Management Accountant (CMA) CMA-Part-I-Question-Bank-WILEY 2022. Contains over 1500 Q&A in (All)

Certified Management Accountant (CMA) CMA-Part-I-Question-Bank-WILEY 2022. Contains over 1500 Q&A in 535 Pages.

Document Content and Description Below

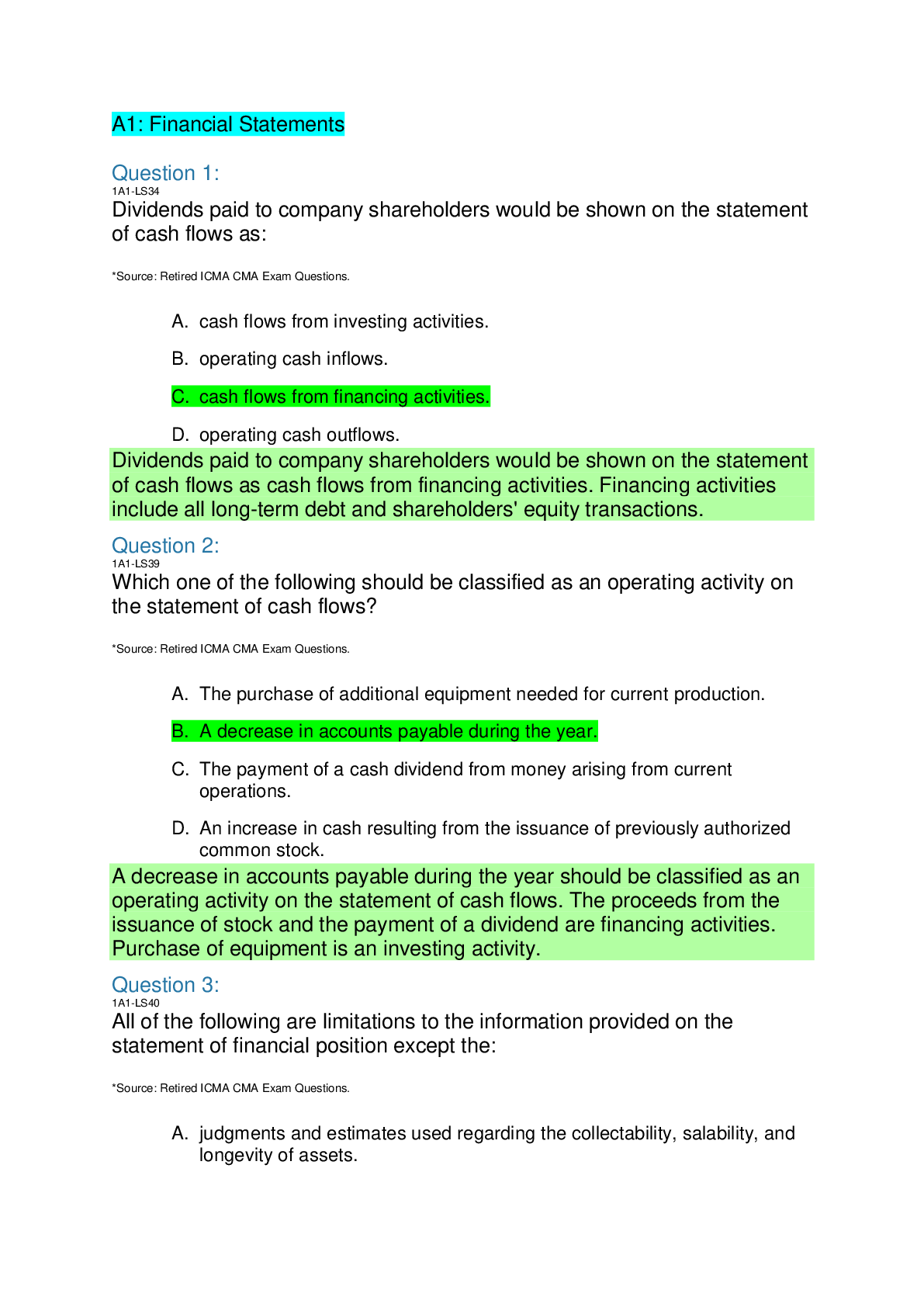

CMA-Part-I-Question-Bank-WILEY (Contains over 1500 Q&A in 535 Pages) A1: Financial Statements A1: Financial Statements Question 1: 1A1-LS34 Dividends paid to company shareholders would be shown o... n the statement of cash flows as: *Source: Retired ICMA CMA Exam Questions. A. cash flows from investing activities. B. operating cash inflows. C. cash flows from financing activities. D. operating cash outflows.Dividends paid to company shareholders would be shown on the statement of cash flows as cash flows from financing activities. Financing activities include all long-term debt and shareholders' equity transactions. Question 2: 1A1-LS39 Which one of the following should be classified as an operating activity on the statement of cash flows? *Source: Retired ICMA CMA Exam Questions. A. The purchase of additional equipment needed for current production. B. A decrease in accounts payable during the year. C. The payment of a cash dividend from money arising from current operations. D. An increase in cash resulting from the issuance of previously authorized common stock.A decrease in accounts payable during the year should be classified as an operating activity on the statement of cash flows. The proceeds from the issuance of stock and the payment of a dividend are financing activities. Purchase of equipment is an investing activity. Question 3: 1A1-LS40 All of the following are limitations to the information provided on the statement of financial position except the: *Source: Retired ICMA CMA Exam Questions. A. judgments and estimates used regarding the collectability, salability, and longevity of assets. B. lack of current valuation for most assets and liabilities. C. omission of items that are of financial value to the business such as the worth of the employees. D. quality of the earnings reported for the enterprise.Earnings for the enterprise are reported on the income, not the statement of financial position (i.e. the balance sheet). Question 4: 1A1-CQ09 Pierre Company had the following transactions during the fiscal year ending December 31, year 3: • Sold a delivery van with a net book value of $5,000 for $6,000 cash, reporting a gain of $1,000. • Paid interest to bondholders for the amount of $275,000 • Declared dividends on December 31, year 3, of $.08 per share on the 1.3 million shares outstanding, payable to shareholders of record on January 31, year 4. No dividends were declared or paid in prior years. • Accounts receivable decreased from $70,000 on December 31, year 2 to $60,000 on December 31, year 3. • Accounts payable increased from $40,000 on December 31, year 2 to $45,000 on December 31, year 3. • The cash balance was $150,000 on December 31, year 2, and $177,500 on December 31, year 3. Which of the answers below describes the correct entry for Pierre Company's statement of cash flows on December 31, year 3 using the indirect method? A. The decrease of $10,000 in accounts receivable is reported as a $10,000 decrease in the operating section of the statement of cash flows. B. The $104,000 dividend payout is represented as an outflow of funds in the financing section. C. Financing activities include the $1,000 gain from the sale of the delivery van. D. The $1,000 gain from the sale of the delivery van is included in operating activities as a deduction.Under the indirect method of cash flow statement preparation, net operating cash flow is determined by adjusting net income. Using the indirect method, the full $6,000 received for the asset sale is included in the investing activities section. Since the $1,000 gain is already included in net income it must be deducted so as not to be double counted. Question 5: 1A1-CQ10 Pierre Company had the following transactions during the fiscal year ending December 31, year 3: • Sold a delivery van with a net book value of $5,000 for $6,000 cash, reporting a gain of $1,000. • Paid interest to bondholders for the amount of $275,000 • Declared dividends on December 31, year 3, of $.08 per share on the 1.3 million shares outstanding, payable to shareholders of record on January 31, year 4. No dividends were declared or paid in prior years. • Accounts receivable decreased from $70,000 on December 31, year 2 to $60,000 on December 31, year 3. • Accounts payable increased from $40,000 on December 31, year 2 to $45,000 on December 31, year 3.The cash balance was $150,000 on December 31, year 2, and $177,500 on December 31, year 3 What is the net effect of taking the total cash provided (used) by operating activities, adding it to the cash provided (used) by investing activities, and adding that to the cash provided (used) by financing activities? A. Positive cash flow of $27,500. B. Negative cash flow of $371,000. C. Positive cash flow of $22,500. D. Negative cash flow of $366,000.The total cash provided (used) by the three activities (operating, investing, and financing) should equal the increase or decrease in cash for the year. The difference between the beginning balance of cash of $150,000, and the ending balance of cash of $177,500 is equal to $27,500. Question 6: 1A1-CQ13 An item of inventory purchased for $30 had been incorrectly written down at the end of last year to a current replacement cost of $22. The item is currently selling for $60, its normal selling price. The error will affect the financial statements in which of the following ways? A. The income for this year will be overstated. B. The income for this year will be unaffected. C. The cost of sales for this year will be overstated. D. The income for last year is overstated.Since the inventory item had been incorrectly valued at $22 instead of $30 at the end of the previous year, the current-year cost would have been lower by $8, resulting in higher (overstated) net income for the year. Income for the prior year was correspondingly understated. Question 7: 1A1-LS30 When using the statement of cash flows to evaluate a company's continuing solvency, the most important factor to consider is the cash: *Source: Retired ICMA CMA Exam Questions. A. flows from (used for) investing activities. B. balance at the end of the period. C. flows from (used for) operating activities. D. flows from (used for) financing activities.When using the statement of cash flows to evaluate a company's continuing solvency, the most important factor to consider is the cash flows from (used for) operating activities since over time, cash flow from operations has to cover everything. Question 8: 1A1-CQ08 Pierre Company had the following transactions during the fiscal year ending December 31, year 3: • Sold a delivery van with a net book value of $5,000 for $6,000 cash, reporting a gain of $1,000. • Paid interest to bondholders for the amount of $275,000. • Declared dividends on December 31, year 3, of $.08 per share on the 1.3 million shares outstanding, payable to shareholders of record on January 31, year 4. No dividends were declared or paid in prior years. • Accounts receivable decreased from $70,000 on December 31, year 2 to $60,000 on December 31, year 3. • Accounts payable increased from $40,000 on December 31, year 2 to $45,000 on December 31, year 3. • The cash balance was $150,000 on December 31, year 2, and $177,500 on December 31, year 3 Pierre Company prepared its statement of cash flows using the direct method on December 31, year 3. The interest paid to bondholders is reported: A. As an outflow of cash in the investing activities section. B. As an outflow of cash in the operating activities section. C. As an outflow of cash in the financing activities section. D. As an outflow of cash in the debt servicing activities section.This is a payment of interest on a debt obligation, the payment of interest to bondholders is considered a cash outflow from an operating activity. Question 9: 1A1-W009 Suzanne Rogers, a financial analyst, is analyzing Capital One's stock. She is more interested in estimating the cash flows it can generate. From the financial analyst's perspective, which of the following balance sheet reporting is best suited to avoid adjustments? A. Inventory reported at current market value; fixed assets reported at historical cost. B. Inventory reported at replacement cost; fixed assets reported at market value. C. Inventory reported at historical cost; fixed assets reported at market value. D. Inventory reported at historical cost; fixed assets reported at fair value.The current market value of inventory closely reflects the value at which it can be sold. Fixed assets reported at historical cost will help to estimate depreciation expense correctly to estimate the tax shield from depreciation. Question 10: 1A1-CQ12 At the end of the current fiscal year, XL Company reported net income of $40,000. In addition, the following information is available. Using the indirect method, what amount should be reported as cash flow from financing activities on XL's Statement of Cash Flows for the current fiscal year? A. ($6,500). B. ($9,500). C. ($39,500). D. ($20,500).The cash flow provided from financing activities is computed by taking the Increase in notes payable of $1,500, adding the increase in additional paidin capital of $3,000, less the decrease in long-term debt of $12,000, plus the increase in common stock of $1,000, less the entire amount of the cash dividends paid (not the increase/decrease from prior year) of $33,000. Question 11: 1A1-LS31 A statement of financial position provides a basis for all of the following except: *Source: Retired ICMA CMA Exam Questions. A. evaluating capital structure. B. assessing liquidity and financial flexibility. C. determining profitability and assessing past performance. D. computing rates of return.A statement of financial position provides a basis for computing rates of return, evaluating capital structures, and assessing liquidity and financial flexibility. The income statement determines profitability and assesses past performance. Question 12: 1A1-W020 Juan Baker Inc. filed a suit against Foster Desserts in the second quarter of the current year and claimed damages worth $15,000. There was also a pending litigation against Juan Baker Inc. for $12,000 to its suppliers for supplying lower-quality goods. The company was expecting to win the suit against Foster Desserts. For presenting the financial statements for the year, Juan Baker's accountant realized a net gain of $3,000 as other comprehensive income. As per U.S. GAAP, how should this information be presented? A. The accountant should recognize contingent liability of $12,000 and disclose contingent gains of $15,000 as footnotes. B. This information should not be presented as part of financial statements but should be disclosed in footnotes to financial statements. C. The accountant should realize net gain of $3,000 as part of gains from extraordinary items. D. This information should not be presented in financial statements but should be disclosed in the directors' responsibility statement.Accounting recognition is not given to gain contingencies to avoid the premature recognition of income before its realization. However, loss contingencies must be recognized when it is both probable that a loss has been incurred and the amount of the loss is reasonably estimable. Question 13: 1A1-CQ07 Which of the following financial statement changes would best represent the impact of incurring and paying interest on a note payable for the period: A. Effect on Equity Section of the Balance Sheet: No effect Statement of Cash Flows Direct Method: Outflow from Operating Activities. B. Effect on Equity Section of the Balance Sheet: Decrease Statement of Cash Flows Direct Method: Outflow from Operating Activities. C. Effect on Equity Section of the Balance Sheet: No effect Statement of Cash Flows Direct Method: Outflow from Financing Activities. D. Effect on Equity Section of the Balance Sheet: Decrease Statement of Cash Flows Direct Method: Outflow from Financing Activities.Interest incurred during the reporting period on a note payable is considered an “interest expense” on the income statement which reduces net income, and in turn, decreases the equity section of the balance sheet. Interest expense paid is considered an operating activity as it is used to pay for the day-to-day operating activities of the organization. Therefore, for statement of cash flow purposes, interest expense paid would be classified as an outflow from operating activities. Question 14: 1A1-W019 Perry Avon Corp. is engaged in the manufacture of cargo ships. The company wants to avail itself of a long-term loan from Wealth Bank and has provided the following information. The current assets, as per last year's balance sheet, include inventory of cargo ships of $2,250,000 and $300,000 of accounts receivable. The amount of inventory includes cargo ships lying in stock for 18 months, and the amount of accounts receivable includes accounts due for 90 days. The company grants a credit period of 60 days to its customers. The bank manager decided to grant the loan, as the current ratio of the company was 9.44. As per the bank's credit policy, a company is eligible to avail itself of loans if its current ratio is more than 2.5. However, the bank's credit analyst disapproved the manager's decision, as he recalculated the current ratio to be 1.11 based on some adjustments. Which of the following, if true, will support the credit analyst's decision? A. The credit analyst did not consider the accounts receivable for the calculation of current ratio as they should be classified as bad debts. B. The current liabilities were inflated due to the principal payment of loans in the previous year. The bank manager ignored this fact. C. The credit analyst did not consider the impact of an increase in inventory and accounts receivable due to inventory worth $10,000 purchased on credit. D. The credit analyst feels that the company's liquidity is overstated because of the inclusion of cargo ships as current assets.The inventory of cargo ships has been lying in stock for 18 months. Therefore, considering the value of inventory in the calculation of current ratio will not provide a true picture of the company's liquidity. Question 15: 2A4-CQ19 Selected financial information for Kristina Company for the year just ended is shown below. Kristina's cash flow from investing activities for the year is: *Source: Retired ICMA CMA Exam Questions. A. $1,220,000. B. $1,300,000. C. $(1,500,000). D. $2,800,000.The cash flow from investing activities is calculated as cash received from the sale of available-for-sale Securities minus cash paid for the acquisition of land or $2,800,000 - 1,500,000= $1,300,000. Question 16: 2A4-CQ22 Selected financial information for Kristina Company for the year just ended is shown below. Assuming the indirect method is used, Kristina's cash flow from operating activities for the year is: *Source: Retired ICMA CMA Exam Questions. A. $1,700,000. B. $2,400,000. C. $2,000,000. D. $3,100,000.Net income 2,000,000 + depreciation 400,000 - increase in accounts receivable 300,000 + decrease in inventory 100,000 + increase in accounts payable 200,000 - gain on sale of securities 700,00 = 1,700,000 cash flow from operating activities. Question 17: 1A1-LS33 All of the following are elements of an income statement except: *Source: Retired ICMA CMA Exam Questions. A. gains and losses. B. shareholders' equity. C. expenses. D. revenue.Shareholders' equity does not appear on an income statement. It appears on the balance sheet. Revenue, expenses, gains and losses all appear on an income statement. Question 18: 1A1-W025 While approving the financial statements for the current year, the management accountant of Rachael Groups discovered that sales were overstated. Which of the following is the most likely reason for the overstatement? A. Sales returns recorded are more than actual returns. B. Abnormal losses are not accounted for. C. General sales tax collected from customers was not accounted for. D. The last in, first out method is used for valuation of inventory.Usually sales tax is included in the selling price of a product. The sales account should be adjusted for the amount of sales tax collected, and it should be recorded as a liability. Question 19: 2A4-CQ16 Carlson Company has the following payments recorded for the current period. The total amount of the above items to be shown in the Operating Activities Section of Carlson's Cash Flow Statement should be: *Source: Retired ICMA CMA Exam Questions. A. $150,000. B. $250,000. C. $750,000. D. $350,000.Interest paid on bank loans are considered an operating activity. Operating cash flows include interest and dividends received and interest and income taxes paid as well as normal operating inflows and outflows. Dividends paid are a financial activities. Purchase of equipment is an investing activity. Question 20: 1A1-W008 Which of the following is a reason why a company provides prior years' financial information along with the current year's information? A. Doing this helps the users of financial statements in measuring the reliability of information provided in the financial statements. B. Doing this allows management accountants to determine the trend in an increase in resource requirement for future periods. C. Doing this allows analysts to easily compare past performance to present performance and determine its future success. D. This form of presentation of financial statements helps in prioritizing one type of revenue or gain over another to avoid classification problems.Most entities provide prior years' financial statement information alongside the current year's information for comparison as this allows analysts to easily compare past performance to present performance and make a determination of future success. Question 21: 1A1-W016 The following information is extracted from the financial statements of BrentPage. Net income | $25,000 Depreciation on equipment | 2,000 Dividend income | 3,500 Interest income | 3,000 Increase in current assets | 5,400 Increase in current liabilities | 500 Loans granted to subsidiaries | 12,000Assuming the company follows U.S. GAAP, calculate the cash flow from operating activities. A. $32,900 B. $10,100 C. $28,600 D. $22,100The correct answer is $22,100. CFO = Net income + Depreciation - Increase in current assets + Increase in current liabilities = $25,000 + $2,000 - $5,400 + $500 = $22,100 Question 22: 1A1-W017 "Employing different accounting methods will yield different net incomes." How is this factor a limitation of financial statements? A. Choice between cash-based accounting and accrual accounting for financial reporting allows companies to smooth earnings for a longer period. B. The flexibility of employing different methods for presentation of financial statements can lead to inaccurate disclosure of information. C. Change in net income due to change in accounting methods affects the determination of future performance of a company. D. Difference in results due to change in accounting methods makes it difficult for users to compare the performance of different entities.Employing different accounting methods will yield different net incomes. Each choice of two or more accounting methods will further change the results reported, making the task of comparing different entities very difficult, even when these methods are disclosed. Question 23: 1A1-LS29 The statement of shareholders' equity shows a: *Source: Retired ICMA CMA Exam Questions. A. reconciliation of the beginning and ending balances in the Retained Earnings account. B. reconciliation of the beginning and ending balances in shareholders' equity accounts. C. computation of the number of shares outstanding used for earnings per share calculations. D. listing of all shareholders' equity accounts and their corresponding dollar amounts.The purpose of the statement of shareholders' equity is to reconcile the beginning and ending balances in shareholders' equity accounts. Question 24: 2A4-CQ20 For the fiscal year just ended, Doran Electronics had the following results. Doran's net cash flow from operating activities is: *Source: Retired ICMA CMA Exam Questions. A. $1,018,000. B. $928,000. C. $986,000. D. $1,074,000.The net cash flow from operating activities is calculated as Net income + Depreciation expense + Increase in accounts payable - Increase in accounts receivable + Increase in deferred income tax liability or ($920,000 + 110,000 + 45,000 -73,000 + 16,000) = $1,018,000. Question 25: 1A1-LS35 All of the following are classifications on the Statement of Cash Flows except: *Source: Retired ICMA CMA Exam Questions. A. investing activities. B. equity activities. C. operating activities. D. financing activities.The classifications on the Statement of Cash Flows are operating activities, investing activities and financing activities. Question 26: 1A1-LS43 When a fixed asset is sold for less than book value, which one of the following will decrease? *Source: Retired ICMA CMA Exam Questions. A. Current ratio. B. Total current assets. C. Net working capital. D. Net profit.When a fixed asset is sold for less than book value, a loss occurs decreasing net profit. Question 27: 1A1-LS38 Kelli Company acquired land by assuming a mortgage for the full acquisition cost. This transaction should be disclosed on Kelli's Statement of Cash Flows as a(n): *Source: Retired ICMA CMA Exam Questions. A. operating activity. B. noncash financing and investing activity. C. financing activity. D. investing activity.Acquiring a mortgage would require a noncash financing disclosure on the statement of cash flows. The land itself is an investment and would be accounted for as an investing activity. Question 28: 1A1-W004 The cash flow from operations for Charlene Energy Inc. is $25,000 for the current year. If the amortization expense increases by $5,000 and other factors remain same, under which of the following assumptions will the cash flow from operations remain unaffected? A. A change in amortization method will not have a retrospective effect. B. The company has an infinite life. C. The company is operating in a tax-free environment. D. The company can change the depreciation method during a financial year.Cash inflow from amortization arises because of the tax shield. In a tax-free environment, a change in amortization will not affect the cash flows from operations. Question 29: 2A4-CQ13 Larry Mitchell, Bailey Company's controller, is gathering data for the Statement of Cash Flows for the most recent year end. Mitchell is planning to use the direct method to prepare this statement, and has made the following list of cash inflows for the period. — Collections of $100,000 for goods sold to customers. — Securities purchased for investment purposes with an original cost of $100,000 sold for $125,000. — Proceeds from the issuance of additional company stock totaling $10,000. The correct amount to be shown as cash inflows from operating activities is: *Source: Retired ICMA CMA Exam Questions. A. $225,000. B. $135,000. C. $100,000. D. $235,000.When using the direct method, collections of $100,000 for goods sold to customers would be classified as an operating activity. The cash sale of securities is an investing activity. The issuance of stock for cash is a financing activity. Question 30: 1A1-W001 The multi-step income statement, with additional income statement items, for Harrington Technologies Inc. is given below. Net sales | $2,000,000 Less: Cost of goods sold | 890,000 Gross profit | 1,110,000 Less: Transportation and travel | 45,000 Depreciation | 68,000 Pension contributions | 21,000 Operating income | 976,000 Less: Discontinued operations | 76,000 Income before taxes | 900,000 Less: Tax expense @ 30% | 270,000 Net income | $630,000Glen Hamilton, a financial analyst, analyzed the company's financial statements and concluded that the real net income should be $683,200 instead of $630,000. Which of the following arguments is most likely to support his conclusion? A. $53,200 due from a client was written off as irrecoverable after the finalization of accounts for the current period. B. The company valued its inventory using the specific identification method, whereas the financial analyst used the last in, first out (LIFO) method for the current period. C. The company might have liquidated its LIFO reserve. D. The company has included expenses in relation to discontinued operations as part of income from continued operations.Revenue and expenses from discontinued operations do not form part of income from continued operations. In this case, the analyst has excluded discontinued operations since it is a nonrecurring item. Question 31: 1A1-W021 Why is it important for a financial analyst to scrutinize footnotes? A. Footnotes provide vital information about a company's liquidity position, trend in revenue from different demographic regions, and changes in capital structure. B. Footnotes provide significant information about noncash investing and financing activities, such as the issuing of stock for fixed assets. C. Footnotes detail the executive compensation details and shareholders' voting procedures and information. D. Footnotes provide significant information about mergers and acquisitions a company is targeting in the current year.The statement of cash flows requires footnote disclosure of any significant noncash investing and financing activities, such as the issuing of stock for fixed assets or the conversion of debt to equity. Question 32: 1A1-W023 Rita Williams and Sasha Ortiz recently joined Flifund Financials, a fund management company. They are assigned to value the stock of Probe Systems. Rita's estimate of assets and liabilities is higher than Sasha's estimate. Which of the following will most likely undermine Rita's estimation? A. The company has no operating lease. B. The company has purchased a high amount inventory on credit. C. The company has an off-balance sheet transaction. D. The company has no debt.Some transactions, like operating leases, can be recorded in a way that avoids reporting liabilities and assets on the balance sheet. Here, Rita might have discovered the use of the operating lease by Probe Systems and hence valued Probe's assets and liabilities higher. Question 33: 2A4-CQ21 Three years ago, James Company purchased stock in Zebra Inc. at a cost of $100,000. This stock was sold for $150,000 during the current fiscal year. The result of this transaction should be shown in the Investing Activities Section of James' Statement of Cash Flows as: *Source: Retired ICMA CMA Exam Questions. A. $50,000. B. $100,000. C. $150,000. D. Zero.The amount shown is the investing section would be the amount the stock was sold for during the current fiscal year. Question 34: 2A4-CQ17 Barber Company has recorded the following payments for the current period. The amount to be shown in the Financing Activities Section of Barber's Cash Flow Statement should be: *Source: Retired ICMA CMA Exam Questions. A. $600,000. B. $500,000. C. $300,000. D. $900,000.Both dividends paid to Barber shareholders and the repurchase of Barber Company stock are financing activities. Financing activities include longterm debt and equity cash transactions. Interest paid is included in operating cash flows. Question 35: 1A1-LS36 The sale of available-for-sale securities should be accounted for on the statement of cash flows as a(n): *Source: Retired ICMA CMA Exam Questions. A. investing activity. B. financing activity. C. noncash investing and financing activity. D. operating activity.Cash flows from the investment in or disposal of available-for-sale securities will be accounted for in the statement of cash flows as an investing activity. Question 36: 1A1-W022 The management accountant of Kathryn Software decided to alter the financial statements due to an event. Which of the following is the most likely reason for her decision? A. The event provides evidence about a loss of expected income due to inefficient collection efforts. B. The company has decided to shift the company's headquarters to a country that follows IFRS in the next year. C. The event provides additional evidence about conditions that existed as of the balance sheet date and alters the estimates used. D. There is a sharp decline in the stock price.If a subsequent event provides additional evidence about conditions that existed as of the balance sheet date and alters the estimates used in preparing the financial statements, then the financial statements should be adjusted. Question 37: 1A1-LS42 The presentation of the major classes of operating cash receipts (such as receipts from customers) less the major classes of operating cash disbursements (such as cash paid for merchandise) is best described as the: *Source: Retired ICMA CMA Exam Questions. A. indirect method of calculating net cash provided or used by operating activities. B. cash method of determining income in conformity with generally accepted accounting principles. C. direct method of calculating net cash provided or used by operating activities. D. format of the statement of cash flows.The direct method of calculating net cash provided or used by operating activities presents the major classes of operating cash receipts (such as receipts from customers) less the major classes of operating cash disbursements (such as cash paid for merchandise). Question 38: 1A1-LS37 A statement of cash flows prepared using the indirect method would have cash activities listed in which one of the following orders? *Source: Retired ICMA CMA Exam Questions. A. Operating, investing, financing. B. Investing, financing, operating. C. Financing, investing, operating. D. Operating, financing, investing. A statement of cash flows prepared using the indirect method would have cash activities listed first as operating, next as investing, and third as financing. Question 39: 1A1-W007 The management of Arthur Energy recognized a contingent liability of $50,000 in the current year. However, before the annual report was issued, the company resolved the issue, making a lump-sum payment of $42,000. The board of directors has decided to incorporate the transaction in the subsequent year's financial statements. Which of the following provisions of U.S. GAAP, if applicable, is likely to prove the management decision wrong? A. Loss contingencies must be recognized when it is probable that a loss has been incurred and the amount of the loss is reasonably estimable. B. Whenever GAAP or industry-specific regulations allow a choice between two or more accounting methods, the method selected should be disclosed. C. If an event alters the estimates used in preparing the financial statements, then the financial statements should be adjusted. D. If an event provides additional evidence about conditions that existed as of the balance sheet date and alters the estimates used, then the financial statements should be adjusted.In this case, the amount of contingent liability needs to be revised, as the estimate of the amount of liability has changed. The subsequent event provides evidence regarding conditions present on the balance sheet date. Therefore, the financial statements need to be adjusted. Question 40: 1A1-W0015 The following information is extracted from the financial statements of Foster Machines. Net income | $15,000 Depreciation on equipment | 2,500 Dividend income | 2,500 Interest income | 5,000 Increase in accounts receivable | 8,000 Increase in current liabilities | 6,500 Redemption of bonds | 7,500The cash flows from operations were calculated to be $23,500. Assuming that the company follows U.S. GAAP, which of the following is a potential error in the calculation of cash flow from operations? A. Dividend income and interest income were added back to net income to calculate cash flows from operations. B. Redemption of bonds was included in cash flow from operations. C. Increase in accounts receivable was added to net income whereas it should have been deducted. D. Depreciation on equipment was not added back to net income for calculating cash flows from operations.As per U.S. GAAP, dividend income and interest income are included in the calculation of net income. Hence, dividend income and interest income, being operating activities, should not be added back to net income. Question 41: 1A1-LS28 Which one of the following would result in a decrease to cash flow in the indirect method of preparing a statement of cash flows? *Source: Retired ICMA CMA Exam. Questions. A. Decrease in income taxes payable. B. Proceeds from the issuance of common stock. C. Amortization expense. D. Decrease in inventories.When using the indirect method, a decrease to cash flow would occur when a business pays off its liabilities; therefore, a decrease in income taxes payable would result in a decrease to cash when using the indirect method. Question 42: 1A1-W024 As per U.S. GAAP, extraordinary items are: A. Material items that are both unusual in nature and infrequent in occurrence. B. Material items that are either unusual in nature and infrequent in occurrence. C. Material items that are both unusual in nature and frequent in occurrence. D. Material events with an uncertain outcome dependent on the occurrence or nonoccurrence of one or more future events.Extraordinary items are material items that are both unusual in nature and infrequent in occurrence. Question 43: 1A1-W010 Following is an extract from the statement of shareholders' equity of Joyce Gregory Inc. prepared by the finance manager. Common stock shares | Common stock amount | Retained earnings | Other | equity Total Balance from previous year | 500,000 | $5,000,000 | $15,000,000 | – | $20,000,000 Net income | – | – | 100,000 | – | 100,000 Issuance of common stock | 1,000 | 10,000 | – | – | 10,000 Other comprehensive income | – | – | – | 10,000 | 10,000 Balance at the end of current year | 501,000 | $5,010,000 | $15,100,000 | $10,000 | $20,120,000The company's CFO did not approve the financial statements. Which of the following, if true, will support the CEO's decision? A. Net income should not be classified under retained earnings. B. Issuance of common stock should be part of retained earnings. C. Other comprehensive income will not be included as part of shareholders' equity. D. Cash flow from operations is not included in the calculation of shareholders' equity.Firms have the option of presenting the calculation of comprehensive income either as part of an income statement or as a separate statement of comprehensive income. Comprehensive income can no longer be presented as a part of the statement of shareholders' equity. Question 44: 1A1-LS44 Stanford Company leased some special-purpose equipment from Vincent Inc. under a long-term lease that was treated as an operating lease by Stanford. After the financial statements for the year had been issued, it was discovered that the lease should have been treated as a capital lease by Stanford. All of the following measures relating to Stanford would be affected by this discovery except the: *Source: Retired ICMA CMA Exam Questions. A. accounts receivable turnover. B. net income percentage. C. debt/equity ratio. D. fixed asset turnover.The accounts receivable turnover is sales divided by the average accounts receivable balance. The classification of a lease would not affect either sales or accounts receivable. Question 45: 1A1-W003 The cash flows and net income from four business segments for Taylor Laboratories Inc. have been provided. Segment 1 | Segment 2 | Segment 3 | Segment 4 Cash flow from operations | $3,000 | $(250) | $(3,000) | $2,000 Cash flow from investing activities | (4,000) | 6,000 | 8,000 | (3,000) Cash flow from financing activities | 1,080 | (1,000) | (1,000) | 1,080 Net income | 1,500 | 1,750 | 2,375 | 1,500Based on the information, which segment should be discontinued by the company? A. Segment 3, because cash used in operations is high and cash inflow is predominantly from investing activities. B. Segment 1, because net income is lowest and requires high investments. C. Segment 4, because net income and cash inflow from operations are low. D. Segment 2, because cash used in operations is low and cash flow from investing activities is not properly utilized.Segment 3 should be discontinued because the major portion of the segment's income could be from the sale of its assets. Question 46: 1A1-W013 Which of the following is true of an income statement presented as per U.S. GAAP? A. It reconciles beginning and ending balances of stockholders' equity. B. Bank overdrafts are always included as a component of selling, general, and administrative expenses. C. Financial measures of contractual agreements such as pension obligations, lease contracts, and stock option plans are required to be disclosed on income statement as a separate line item. D. Disclosure of extraordinary items reported on an income statement is restricted to items that are both unusual and infrequent. Material items that are both unusual in nature and infrequent in occurrence require a separate section in the income statement, shown net of tax. Question 47: 1A1-W005 The following information is extracted from the latest financial information of Hines Materials Inc. Tax rate | 30% Net income | $15,000 Cash flow from operations | $45,000Additional information: 1) | The tax rate for the coming year is expected to increase by 2%. 2) | The company is planning to purchase equipment worth $500,000 in the first quarter of next year. 3) | A 15% increase in capacity is expected with the use of new equipment.Considering the given factors, which of the following would be an ideal strategy to decrease the tax liability for the next year? A. Defer the purchase of equipment to next year to take advantage of a tax-loss carryforward. B. Depreciate the asset using the double-declining balance method to show higher cash flows from operations in initial years. C. Prepare the cash flow statement using the direct method to show lower cash from operations and lower net income. D. Defer the purchase of equipment to next year if a deferred tax liability can be reasonably estimated.Depreciating the equipment using double-declining balance method will result in higher depreciation in the initial years and lower net income. Therefore, the net tax liability of the company will decrease. Question 48: 2A4-AT01 The Smalltown Technology Corporation has prepared the following information. Calculate the cash flow from operating activities in Current year. A. $1,250. B. $1,880. C. $1,190. D. $1,550.Cash flow from operations can be determined by the indirect method (the reconciliation of net income to cash flow from operations). Cash flow from operations using the indirect method is calculated as: Cash flow from operations (indirect method) = net income + non-cash debits in income statement - non-cash credits in income statement + increases in current liabilities (except dividends payable) + decreases in current assets (except cash and cash equivalents) - decreases in current liabilities (except dividends payable) - increases in current assets (except cash and cash equivalents) Therefore, Smalltown's cash flow from operations can be calculated as: Cash flow from operations (indirect method) = $730 net income + $1,150 depreciation + $100 increase in accounts payable - $30 decrease in accrued liabilities - $200 increase in accounts receivable - $200 increase in inventory = $1,550. Question 49: 1A1-W011 According to US GAAP, which of the following statements is true of comprehensive income? A. Firms should report comprehensive income as a separate line item after net income in the income statement. B. Any realized or unrealized gain on an asset should be included as part of comprehensive income, whereas realized or unrealized losses should be excluded from comprehensive income. C. Firms have the option of presenting the calculation of comprehensive income either as part of an income statement or as a separate statement of comprehensive income. D. Comprehensive income can be presented as a part of the statement of shareholders' equity.Comprehensive income can no longer be presented as a part of the statement of shareholders' equity. Firms have the option of presenting the calculation of comprehensive income either as part of an income statement or as a separate statement of comprehensive income. Question 50: 1A1-W014 How does the balance sheet help users? A. It depicts the true value of an entity. B. It measures the nonfinancial performance of an entity. C. It shows the financial performance of an entity for a specific period. D. It assesses an entity's liquidity, solvency, financial flexibility, and operating capability.The balance sheet assesses an entity's liquidity, solvency, financial flexibility, and operating capability. Question 51: 2A4-CQ18 Selected financial information for Kristina Company for the year just ended is shown below. Kristina's cash flow from financing activities for the year is: *Source: Retired ICMA CMA Exam Questions. A. $(80,000). B. $3,520,000. C. $800,000. D. $720,000.The answer is calculated as the cash receivable from the issue of common stock + cash paid for dividends or $800,000 + 80,000 = $720,000. Financing activities include long-term debt and equity cash transactions. The cash acquisition of land and the cash sale of available-for-sale securities are investing transactions. Question 52: 1A1-LS32 The financial statement that provides a summary of the firm's operations for a period of time is the: *Source: Retired ICMA CMA Exam Questions. A. statement of financial position. B. statement of retained earnings. C. statement of shareholders' equity. D. income statement.The financial statement that provides a summary of the firm's operations for a period of time is the income statement. It shows revenues, expenses, gains, losses, and taxes for the period. Question 53: 1A1-LS41 The most commonly used method for calculating and reporting a company's net cash flow from operating activities on its statement of cash flows is the: *Source: Retired ICMA CMA Exam Questions. A. direct method. B. single-step method. C. multiple-step method. D. indirect method.The most commonly used method for calculating and reporting a company's net cash flow from operating activities on its statement of cash flows is the indirect method. The direct method is rarely used because when it is used, the indirect method must be disclosed, However, use of the indirect method does not require disclosure of the direct method. Question 54: 1A1-W018 McCarthy Corp. is issuing its first financial statements. The CFO of the company is of the view that all assets shall be recorded at historical cost throughout the life of the organization. Which of the following is the best critique of such a disclosure? A. Historical value assumes that the value of an asset is the amount that would have to be paid to replace the asset on the balance sheet date. B. Historical value takes into account the effects of inflation on the asset; therefore, the value fluctuates in each period. C. Historical value does not take into account the effect of depreciation; therefore, the true value of the asset cannot be determined. D. Historical value is less relevant for assessing a company's current financial position.Most asset accounts of a nonfinancial nature are reported at historical cost. While historical cost measures are considered reliable because the amounts can be verified, they are also considered less relevant than fair value or current market value measures would be for assessing a firm's current financial position. Question 55: 1A1-W002 The current ratio for Garrett Inc. for the previous five years is as follows. Year 1 | Year 2 | Year 3 | Year 4 | Year 5 Current Ratio | 5 | 4.5 | 4.9 | 1.2 | 4.2Which of the following factors is the most likely reason for the low current ratio in Year 4? A. Materials were purchased on credit in Year 4 for which payment is due. B. Long-term debts were due for repayment in Year 4. C. The company reduced its credit period in Year 4. D. Working capital in Year 4 decreased due to an increase in accounts payable.The current portion of long-term debt is included in current liabilities in the year of repayment. Hence, the principal amount for long-term debts might have been due in Year 4 and classified as current liabilities. Question 56: 1A1-LS27 The financial statements included in the annual report to the shareholders are least useful to which one of the following? *Source: Retired ICMA CMA Exam Questions. A. Competing businesses. B. Stockbrokers. C. Managers in charge of operating activities. D. Bankers preparing to lend money.Generally, the financial statements included in the annual report to the shareholders are most useful to external stakeholders such as stockbrokers, bankers preparing to lend money, and competing businesses. Therefore, these reports are least useful to managers in charge of operating activities. Question 57: 2A4-CQ15 Atwater Company has recorded the following payments for the current period. The amount to be shown in the Investing Activities Section of Atwater's Cash Flow Statement should be: *Source: Retired ICMA CMA Exam Questions. A. $500,000. B. $900,000. C. $300,000. D. $700,000.Purchasing another company's stock would be classified as an investing activity. The other two transactions are financing transactions. Question 58: 2A4-CQ14 During the year, Deltech Inc. acquired a long-term productive asset for $5,000 and also borrowed $10,000 from a local bank. These transactions should be reported on Deltech's Statement of Cash Flows as: *Source: Retired ICMA CMA Exam Questions. A. Outflows for Financing Activities, $5,000; Inflows from Investing Activities, $10,000. B. Inflows from Investing Activities, $10,000; Outflows for Financing Activities, $5,000. C. Outflows for Operating Activities, $5,000; Inflows from Financing Activities, $10,000. D. Outflows for Investing Activities, $5,000; Inflows from Financial Activities, $10,000.Purchasing a long-term assets would be classified as an outflows for Investing Activities. Borrowing money would be classified as a inflow from Financial Activities. Question 59: 1A1-W006 The financial accountant of Eva Wolfe Corp. has ascertained the cash flows from operations as follows. Net income | $15,000 Depreciation on equipment | 2,500 Dividend income | 2,500 Interest income | 5,000 Increase in current assets | 8,000 Increase in current liabilities | 6,500 Cash flow from operations | $16,000The management accountant of the company argues that the cash flow from operations should be $8,500. Which of the following statements, if true, will undermine the management accountant's calculation? A. The company operates in a tax-free environment. B. Dividend income and interest income, already included in net income, are considered cash flow from operating activities. C. Cash flow from operations is ascertained using the direct method. D. Depreciation on equipment should not be added back to net income for calculating cash flow from operations.Investing cash inflows result from sales of property, plant, and equipment; sales of investments in another entity's debt or equity securities; or collections of the principal on loans to another entity. However, dividend income and interest income are included in cash flow from operating activities. Hence, the management accountant might have incorrectly calculated the cash flow from operations as follows: $15,000 + $2,500 - ($8,000 - $6,500) - ($2,500 + $5,000) = $8,500. Question 60: 1A1-W012 The following information is available for Matthews Holdings Inc.: Net sales | $25,000 Depreciation | 2,000 Cost of goods sold | 3,500 Gain on sale of asset | 3,000 Loss from discontinued operations | 5,400 Gain from extraordinary items | 500Calculate the income from continuing operations. A. $22,500 B. $17,100 C. $17,600 D. $23,000Income from continuing operations is calculated as: Net sales | $25,000 Less: Cost of goods sold | 3,500 Less: Depreciation | 2,000 Add: Gain on sale of asset | 3,000 $22,500Question 61: 1A1-CQ06 Silver Streak Enterprises (SSE) began manufacturing latex-based paint in 1978. In 2008, the company developed a new high quality paint which maintains its luster for over 50 years. Due to the success of this new product, sales of the original latex-based paint have declined significantly such that the company has decided to phase out the product in early 2009. Mikayla Andrews is the accounting manager and her primary responsibilities include the preparation and analysis of the annual financial statements. Mikayla has begun analyzing the annual financial transactions and wants to ensure that the operations are presented accurately for the fiscal year ending December 31, 2009. The following transactions have raised questions for Mikayla: 1. SSE invented its new high quality paint in 2008 and received a patent in the same year. In 2008, the company expected that the new patent would have a useful-life of ten years; however, due to innovations by its competitors, SSE has determined that the useful-life of the patent will be reduced to six years beginning in 2009. 2. The year-end physical count of inventory has found $24,000 of the obsolete latex-based paint product which must be written off as obsolete. 3. SSE is a defendant in a lawsuit concerning the durability of its old paint product line. Corporate lawyers believe that the lawsuit against Silver Streak will probably result in a settlement of $50,000 in mid-2010. 4. Silver Streak is also a plaintiff in a lawsuit against a competitor for stealing the manufacturing process of their new product line. Corporate lawyers believe that the lawsuit could likely result in a favorable judgment in the amount of $150,000 in 2010. Explain how each of the four transactions above will affect Silver Streak's Income Statement: A. Transaction 1 would decrease operating income. Transaction 2 would be classified as an “other expense” and would decrease Income Before Taxes. Transaction 3 is a loss contingency that can be reasonably estimated and would appear on the income statement. Transaction 4 is a gain contingency that can be reasonably estimated and would be recorded on the income statement. B. Transaction 1 would decrease operating income. Transaction 2 would be classified as a “cost of goods sold” and would decrease operating income. Transaction 3 is a loss contingency that can be reasonably estimated and would appear on the income statement. Transaction 4 is a contingency that may result in a gain and would be recorded in the financial statements. C. Transaction 1 would decrease operating income. Transaction 2 would be classified as an “other expense” and would decrease Income Before Taxes. Transaction 3 is a loss contingency that may result in a settlement and should appear in the notes but not in the financial statements. Transaction 4 is a contingency that may result in a gain but will not be recorded in the financial statements. D. Transaction 1 would decrease operating income. Transaction 2 would classify as “other expense” and decrease Income Before Taxes. Transaction 3 is a loss contingency that can be reasonably estimated and would appear on the income statement. Transaction 4 is a contingency that may result in a gain but would not be recorded in the financial statements.Transaction 1: The change in useful life is a change in estimates that affects present and future periods only. There will be an increase in amortization that would be reported in operating expenses thus causing a decline in operating income. Change in amortizations will be reflected on current and future financial statements. Transaction 2: As there is obsolete inventory, the category “other expense” is affected on the income statement. Transaction 3: This loss contingency is probable and can be reasonably estimated, and therefore should appear on the income statement as an “other gain or loss”. This loss contingency should also appear in the footnotes to the financial statements. Transaction 4: According to SFAS 5 “Accounting for Contingencies”, contingencies that may result in gains are usually not reflected in the financial statements. Therefore, since the financial impact would not be realizable until received, not including the potential gain from the lawsuit in the financial statements is the proper handling for this year. Question 62: 1A1-CQ11 At the end of the current fiscal year, XL Company reported net income of $40,000. In addition, the following information is available: Using the indirect method, what amount should be reported as cash flow from operating activities on XL's Statement of Cash Flows for the current fiscal year? A. $47,500. B. $49,500. C. $32,500. D. $34,500.The cash flow provided from operating activities is computed by taking the net income of $40,000, less the increase in accounts receivable of $3,000 and less the prepaid expenses increase of $1,500, plus the decrease inventories of $4,500, plus the increase in accounts payable of $7,500. A2: Recognition, Measurement, Valuation, and Disclosure Question 1: 1A2-W002 Claire Enterprises has $150,000 in accounts receivable at the end of Year 1, and it estimates its bad debts to be 5% of the receivables. Hence, the accountant reports $7,500 as bad debts and the net realizable value as $142,500. Under which of the following circumstances will the amount of bad debts reported most likely reduce? A. If the company shortens the credit period allowed. B. If the company lengthens the credit period allowe [Show More]

Last updated: 11 months ago

Preview 1 out of 535 pages

Document information

Connected school, study & course

About the document

Uploaded On

Jun 11, 2022

Number of pages

535

Written in

Additional information

This document has been written for:

Uploaded

Jun 11, 2022

Downloads

1

Views

68