Auditing > TEST BANK > Test Bank For Auditing, and Assurance Services An Integrated Approach 16th Edition By Arens Elder Be (All)

Test Bank For Auditing, and Assurance Services An Integrated Approach 16th Edition By Arens Elder Beasley

Document Content and Description Below

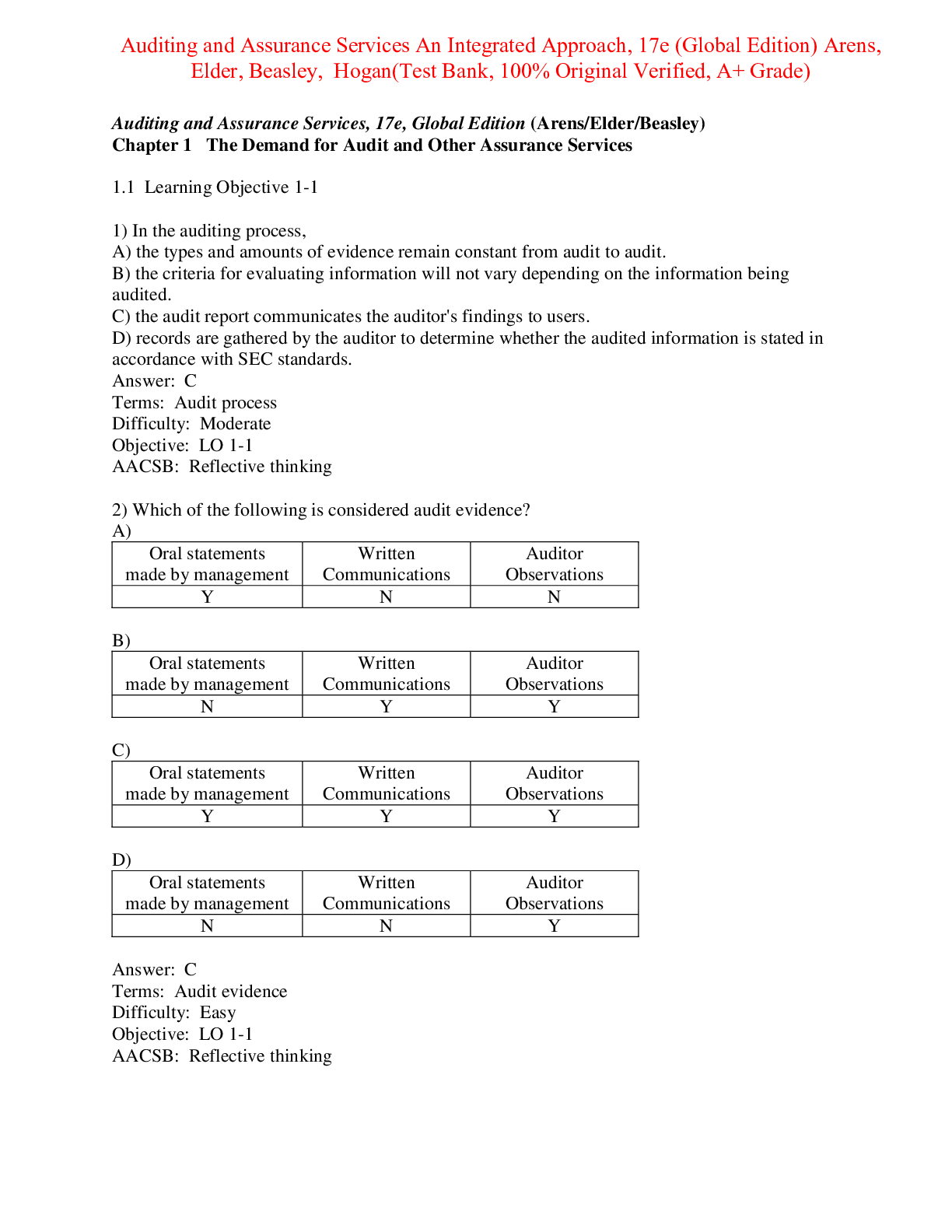

Part 1: The Auditing Profession Chapter 1: The Demand for Audit and Other Assurance Services · Nature of Auditing · Distinction Between Auditing and Accounting · ... Economic Demand for Auditing · Assurance Services · Types of Audits · Types of Auditors · Certified Public Accountant Chapter 2: The CPA Profession · Certified Public Accounting Firms · Structure of CPA Firms · Sarbanes—Oxley Act and Public Company Accounting Oversight Board · Securities and Exchange Commission · American Institute of Certified Public Accountants (AICPA) · International and U.S. Auditing Standards · Organization of U.S. Auditing Standards · Quality Control Chapter 3: Audit Reports · Standard Unmodified Opinion Audit Report for Nonpublic Entities · Conditions for Standard Unmodified Opinion Audit Report · Standard Audit Report and Report on Internal Control Over Financial Reporting Under PCAOB Auditing Standards · Unmodified Opinion Audit Report with Emphasis-of-Matter Explanatory Paragraph or Nonstandard Report Wording · Modifications to the Opinion in the Audit Report · Materiality · Discussion of Conditions Requiring a Modification of Opinion · Auditor’s Decision Process for Audit Reports · International Accounting and Auditing Standards Chapter 4: Professional Ethics · What Are Ethics? · Ethical Dilemmas · Special Need for Ethical Conduct in Professions · Code of Professional Conduct · Independence Rule · Sarbanes—Oxley and Related Independence Requirements · Other Rules of Conduct · Enforcement Chapter 5: Legal Liability · Changed Legal Environment · Distinguishing Business Failure, Audit Failure, and Audit Risk · Legal Concepts Affecting Liability · Liability to Clients · Liability to Third Parties Under Common Law · Civil Liability Under the Federal Securities Laws · Criminal Liability · The Profession’s Response to Legal Liability Part 2: The Audit Process Chapter 6: Audit Responsibilities and Objectives · Objective of Conducting an Audit of Financial Statements · Management’s Responsibilities · Auditor’s Responsibilities · Professional Skepticism · Professional Judgment · Financial Statement Cycles · Setting Audit Objectives · Management Assertions · Transaction-Related Audit Objectives · Balance-Related and Presentation and Disclosure-Related Audit Objectives · How Audit Objectives Are Met Chapter 7: Audit Evidence · Nature of Evidence · Audit Evidence Decisions · Persuasiveness of Evidence · Types of Audit Evidence · Analytical Procedures · Common Financial Ratios · Audit Documentation Chapter 8: Audit Planning and Materiality · Planning · Accept Client and Perform Initial Audit Planning · Understand the Client’s Business and Industry · Perform Preliminary Analytical Procedures · Materiality · Materiality for Financial Statements as a Whole · Determine Performance Materiality · Estimate Misstatement and Compare with Preliminary Judgment Chapter 9: Assessing the Risk of Material Misstatement · Audit Risk · Risk Assessment Procedures · Considering Fraud Risk · Identification of Significant Risks · Audit Risk Model · Assessing Acceptable Audit Risk · Assessing Inherent Risk · Relationship of Risks to Evidence and Factors Influencing Risks · Relationship of Risk and Materiality to Audit Evidence Chapter 10: Assessing and Responding to Fraud Risks · Types of Fraud · Conditions for Fraud · Assessing the Risk of Fraud · Corporate Governance Oversight to Reduce Fraud Risks · Responding to the Risk of Fraud · Specific Fraud Risk Areas · Responsibilities When Fraud Is Suspected · Documenting the Fraud Assessment Chapter 11: Internal Control and Coso Framework · Internal Control Objectives · Management and Auditor Responsibilities for Internal Control · COSO Components of Internal Control · Internal Controls Specific to Information Technology · Impact of IT Infrastructure on Internal Control Chapter 12: Assessing Control Risk and Reporting on Internal Controls · Obtain and Document Understanding of Internal Control · Assess Control Risk · Tests of Controls · Decide Planned Detection Risk and Design Substantive Tests · Auditor Reporting on Internal Control · Evaluating, Reporting, and Testing Internal Control for Nonpublic and Smaller Public Companies · Impact of IT Environment on Control Risk Assessment and Testing Chapter 13: Overall Audit Strategy and Audit Program · Types of Tests · Selecting Which Types of Tests to Perform · Evidence Mix · Design of the Audit Program · Summary of Key Evidence-Related Terms · Summary of the Audit Process Part 3: Application of the Audit Process to the Sales and Collection Cycle Chapter 14: Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transaction · Accounts and Classes of Transactions in the Sales and Collection Cycle · Business Functions in the Cycle and Related Documents and Records · Methodology for Designing Tests of Controls and Substantive Tests of Transactions for Sales · Sales Returns and Allowances · Methodology for Designing Tests of Controls and Substantive Tests of Transactions for Cash Receipts · Audit Tests for Uncollectible Accounts · Effect of Results of Tests of Controls and Substantive Tests of Transactions Chapter 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions · Representative Samples · Statistical Versus Nonstatistical Sampling and Probabilistic Versus Nonprobabilistic Sample Selection · Sample Selection Methods · Sampling for Exception Rates · Application of Nonstatistical Audit Sampling · Statistical Audit Sampling · Application of Attributes Sampling Chapter 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable · Methodology for Designing Tests of Details of Balances · Designing Tests of Details of Balances · Confirmation of Accounts Receivable · Developing Tests of Details Audit Program Chapter 17: Audit Sampling for Tests of Details of Balances · Comparisons of Audit Sampling for Tests of Details of Balances and for Tests of Controls and Substantive Tests of Transactions · Nonstatistical Sampling · Monetary Unit Sampling · Variables Sampling · Illustration Using Difference Estimation Part 4: Application of the Audit Process to Other Cycles Chapter 18: Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable · Accounts and Classes of Transactions in the Acquisition and Payment Cycle · Business Functions in the Cycle and Related Documents and Records · Methodology for Designing Tests of Controls and Substantive Tests of Transactions · Methodology for Designing Tests of Details of Balances for Accounts Payable Chapter 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts · Types of Other Accounts in the Acquisition and Payment Cycle · Audit of Property, Plant, and Equipment · Audit of Prepaid Expenses · Audit of Accrued Liabilities · Audit of Income and Expense Accounts Chapter 20: Audit of the Payroll and Personnel Cycle · Accounts and Transactions in the Payroll and Personnel Cycle · Business Functions in the Cycle and Related Documents and Records · Methodology for Designing Tests of Controls and Substantive Tests of Transactions · Methodology for Designing Substantive Analytical Procedures and Tests of Details of Balances Chapter 21: Audit of the Inventory and Warehouse Cycle · Business Functions in the Cycle and Related Documents and Records · Parts of the Audit of Inventory · Audit of Cost Accounting · Substantive Analytical Procedures · Physical Observation of Inventory · Audit of Pricing and Compilation · Integration of the Tests Chapter 22: Audit of the Capital Acquisition and Repayment Cycle · Accounts in the Cycle · Notes Payable · Owners’ Equity Chapter 23: Audit of Cash and Financial Instruments · Types of Cash and Financial Instruments Accounts · Cash in the Bank and Transaction Cycles · Audit of the General Cash Account · Fraud-Oriented Procedures · Audit of Financial Instruments Accounts Part 5: Completing the Audit Chapter 24: Completing the Audit · Perform Additional Tests for Presentation and Disclosure · Review for Contingent Liabilities and Commitments · Review for Subsequent Events · Final Evidence Accumulation · Evaluate Results · Issue the Audit Report · Communicate with the Audit Committee and Management · Subsequent Discovery of Facts Part 6: Other Assurance and Nonassurance Services Chapter 25: Other Assurance Services · Review, Compilation, and Preparation Services · Review of Interim Financial Information for Public Companies · Attestation Engagements · Reports on Controls at Service Organizations (SOC Reports) · Prospective Financial Statements · Agreed-Upon Procedures Engagements · Other Audits or Limited Assurance Engagements Chapter 26: Internal and Governmental Financial Auditing and Operational Auditing · Internal Financial Auditing · Governmental Financial Auditing Operational Auditing [Show More]

Last updated: 9 months ago

Preview 1 out of 789 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jul 21, 2023

Number of pages

789

Written in

Additional information

This document has been written for:

Uploaded

Jul 21, 2023

Downloads

0

Views

125

.png)