Finance > QUESTIONS & ANSWERS > tutorial question on return, risk, and security market line with solution 2 - COMM 2202tutorial ques (All)

tutorial question on return, risk, and security market line with solution 2 - COMM 2202tutorial question on return, risk, and security market line with solution 2

Document Content and Description Below

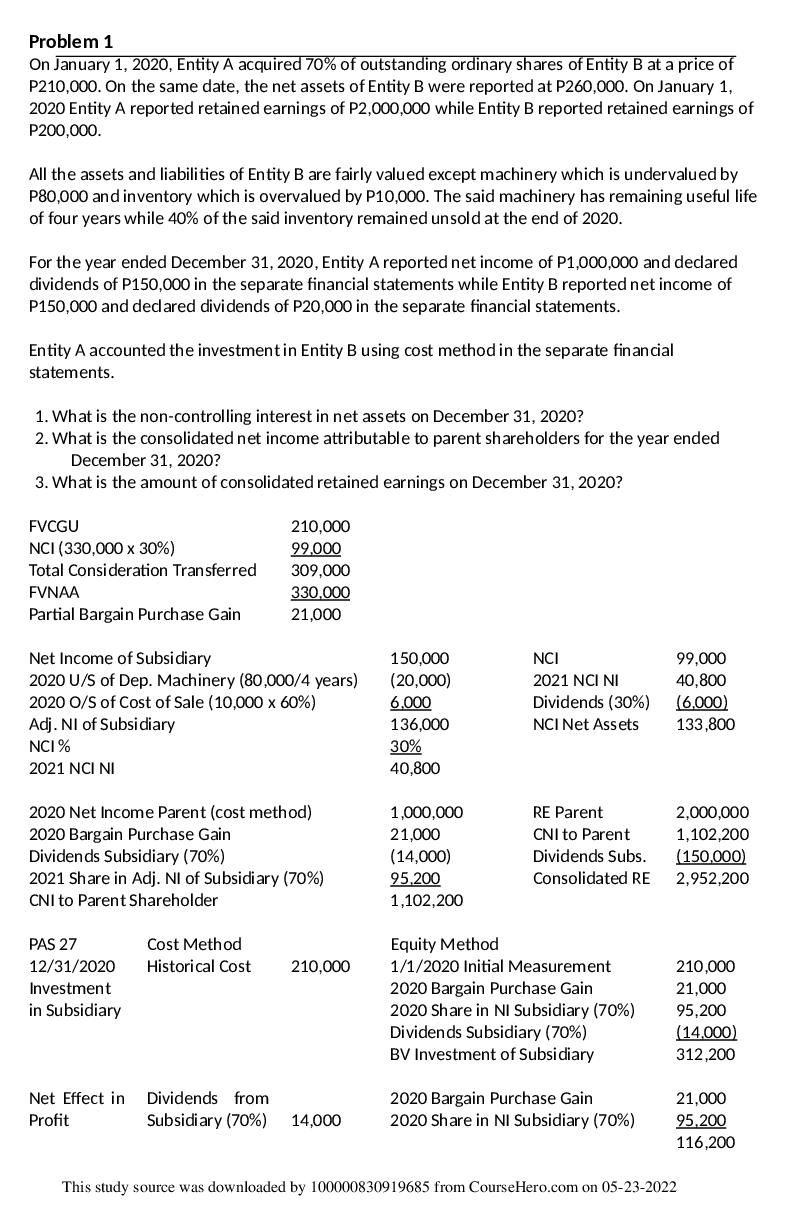

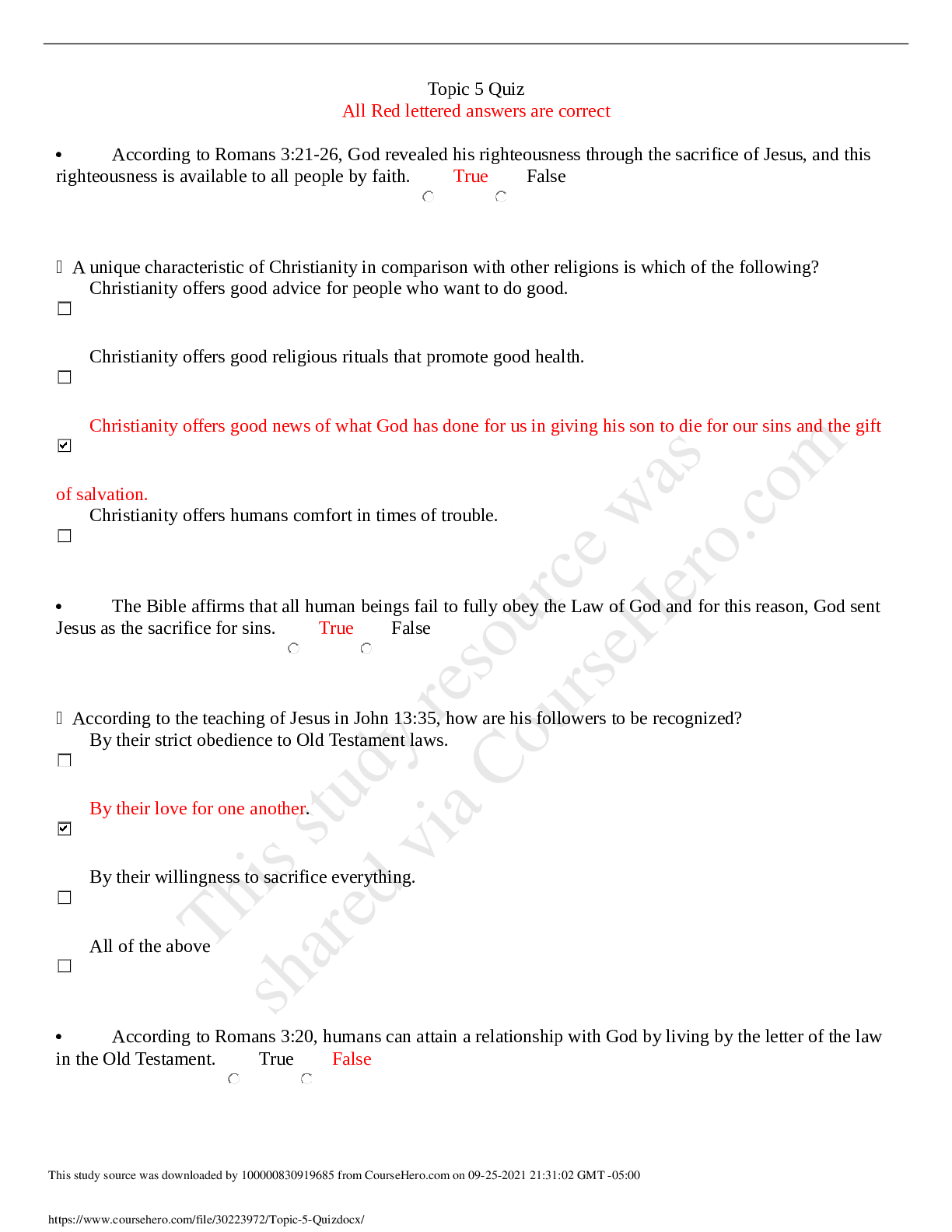

Chapter 13 Questions and Problems The TA will discuss the following questions in the tutorial session on November 22, 2013 9. Returns and Variances (LO1, 2) Consider the following information: Sta... te of economy Probability of state Rate of Return if State Occurs A B C Boom 0.65 0.07 0.15 0.33 Bust 0.35 0.13 0.03 -0.06 a. What is the expected return on an equally weighted portfolio of these three stocks? b. What is the variance of a portfolio invested 20 percent each in A and B and 60 percent in C? 9. (LO1, 2) a. To find the expected return of the portfolio, we need to find the return of the portfolio in each state of the economy. This portfolio is a special case since all three assets have the same weight. To find the expected return in an equally weighted portfolio, we can sum the returns of each asset and divide by the number of b. What is the variance of this portfolio? The standard deviation? 10. (LO1, 2) a. This portfolio does not have an equal weight in each asset. We first need to find the return of the portfolio in each state of the economy. To do this, we will multiply the return of each asset by its portfolio weight and then sum the products to get the portfolio return in each state of the economy. Doing so, we get: Boom: E(Rp) = .30(.35) + .40(.45) + .30(.27) = .3660 or 36.60% Good: E(Rp) = .30(.16) + .40(.10) + .30(.08) = .1 [Show More]

Last updated: 1 year ago

Preview 1 out of 4 pages

.png)

Buy this document to get the full access instantly

Instant Download Access after purchase

Add to cartInstant download

We Accept:

Reviews( 0 )

$7.00

Document information

Connected school, study & course

About the document

Uploaded On

Apr 06, 2021

Number of pages

4

Written in

Additional information

This document has been written for:

Uploaded

Apr 06, 2021

Downloads

0

Views

40

.png)