Financial Accounting > TEST BANK > University of Minnesota, Duluth ACCT 3201 Chapter 8 Flexible Budgets, Overhead Cost Variances, and M (All)

University of Minnesota, Duluth ACCT 3201 Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control TESTBANK-GRADED A+

Document Content and Description Below

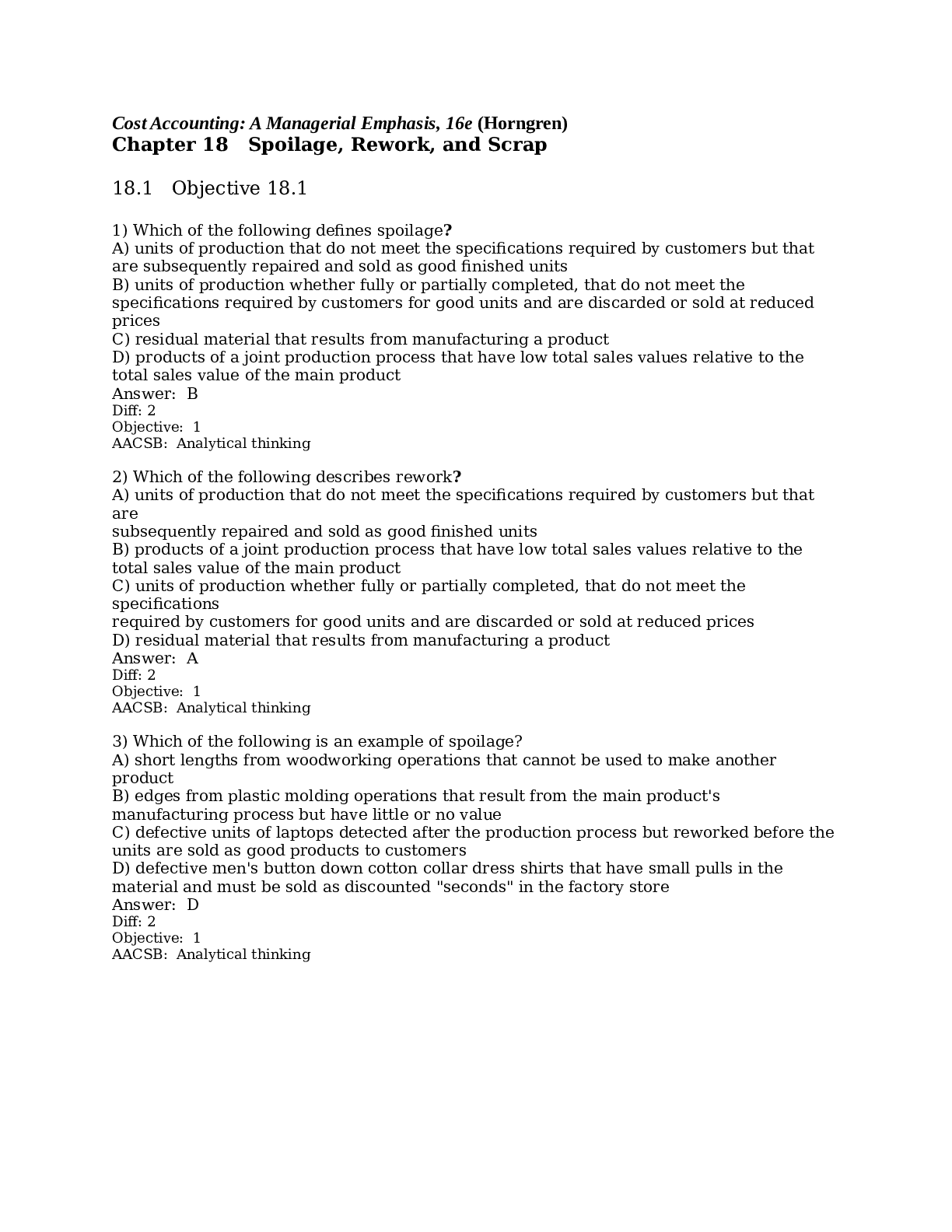

Cost Accounting: A Managerial Emphasis, 16e (Horngren) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control 8.1 Objective 8.1 1) Compared to variable overhead costs planning... , fixed overhead cost planning has an additional strategic issue beyond undertaking only essential activities and efficient operations. That additional requirement is best described as: A) focusing on the highest possible quality B) increasing the linearity between total costs and volume of production C) choosing the appropriate level of capacity that will benefit the company in the long-run D) identifying essential value-adding activities Answer: C Diff: 2 Objective: 1 AACSB: Analytical thinking 2) Effective planning of variable overhead costs means that managers must A) increase the expenditures in the variable overhead budgets B) focus on activities that add value for the customer and eliminate nonvalue-added activities C) increase the linearity between total costs and volume of production D) identify the product advertising requirements and factor those into the variable overhead budget Answer: B Diff: 1 Objective: 1 AACSB: Analytical thinking 3) Which of the following is a true statement of energy costs? A) Energy costs are not controllable B) Strategies to reduce energy costs will not impact variable cost budgets. C) Energy costs are a fixed cost of doing business for a manufacturer. D) Energy costs are a growing component of variable overhead costs. Answer: D Diff: 2 Objective: 1 AACSB: Analytical thinking 4) Fixed overhead costs include ________. A) the cost of sales commissions B) Leasing of machinery used in a factory C) energy costs D) indirect materials Answer: B Diff: 1 Objective: 1 AACSB: Analytical thinking5) Effective planning of fixed overhead costs includes ________. A) planning day-to-day operational decisions B) eliminating value-added costs C) determining which products are to be produced D) choosing the appropriate level of investment in productive assets Answer: D Diff: 2 Objective: 1 AACSB: Analytical thinking 6) Effective planning of variable overhead costs includes ________. A) choosing the appropriate level of investment B) eliminating value-added costs C) redesigning products or processes to use fewer resources D) reorganizing management structure Answer: C Diff: 2 Objective: 1 AACSB: Analytical thinking 7) Most of the decisions determining the level of fixed overhead costs to be incurred will be made ________. A) by the end of a budget period B) by the middle of a budget period C) on a day-to-day ongoing basis D) at the start of a budget period Answer: D Diff: 1 Objective: 1 AACSB: Analytical thinking 8) The major challenge when planning fixed overhead is ________. A) calculating total costs B) calculating the cost-allocation rate C) choosing the appropriate level of capacity D) choosing the appropriate planning period Answer: C Diff: 1 Objective: 1 AACSB: Analytical thinking 9) An effective plan for variable overhead costs will eliminate activities that do not add value. Answer: TRUE Diff: 1 Objective: 1 AACSB: Analytical thinking10) At the start of the budget period, management will have made most decisions regarding the level of fixed overhead costs to be incurred. Answer: TRUE Diff: 2 Objective: 1 AACSB: Analytical thinking 11) The planning of fixed overhead costs differs from the planning of variable overhead costs in terms of timing. Answer: TRUE Diff: 2 Objective: 1 AACSB: Analytical thinking 12) The costs related to buildings (such as rent and insurance), equipment (such as lease payments or straight-line depreciation), and salaried labor in a factory are all examples of cost items that would be part of the fixed overhead budget. Answer: TRUE Explanation: The costs mentioned are all fixed overhead costs. Diff: 1 Objective: 1 AACSB: Analytical thinking 8.2 Objective 8.2 1) Which of the following mathematical expression is used to calculate budgeted variable overhead cost rate per output unit? A) Budgeted output allowed per input unit × Budgeted variable overhead cost rate per input unit B) Budgeted input allowed per output unit ÷ Budgeted variable overhead cost rate per input unit C) Budgeted output allowed per input unit ÷ Budgeted variable overhead cost rate per input unit D) Budgeted input allowed per output unit × Budgeted variable overhead cost rate per input unit Answer: D Diff: 2 Objective: 2 AACSB: Analytical thinking 2) While calculating the costs of products and services, a standard costing system ________. A) allocates overhead costs on the basis of the actual overhead-cost rates B) uses standard costs to determine the cost of products C) does not keep track of overhead cost D) traces direct costs to output by multiplying the standard prices or rates by the actual quantities Answer: B Diff: 2 Objective: 2 AACSB: Analytical thinking3) Which of the following best defines standard costing? A) It is the same as actual costing but done in real time. B) It is a system that traces direct cost to output by multiplying actual process or rates by actual quantities of inputs + allocates overhead by on the basis of actual quantities of the allocation base used. C) It is a system that traces direct costs to output produced by multiplying the standard prices or rates by the standard quantities of inputs allowed for the actual output produced. D) It is a system that allocates overhead costs on the basis of standard overhead cost rates times the actual quantities of the allocation based used. Answer: C Diff: 1 Objective: 2 AACSB: Analytical thinking 4) Which of the following is the mathematical expression for the budgeted fixed overhead cost per unit of cost allocation base? A) Budgeted fixed overhead cost per unit of cost allocation base = Actual total costs in fixed overhead cost pool ÷ Budgeted total quantity of cost allocation base B) Budgeted fixed overhead cost per unit of cost allocation base = Budgeted total costs in fixed overhead cost pool ÷ Budgeted total quantity of cost allocation base C) Budgeted fixed overhead cost per unit of cost allocation base = Actual total costs in fixed overhead cost pool ÷ Actual total quantity of cost allocation base D) Budgeted fixed overhead cost per unit of cost allocation base = Budgeted total costs in fixed overhead cost pool ÷ Actual total quantity of cost allocation base Answer: B Diff: 2 Objective: 2 AACSB: Analytical thinking 5) In flexible budgets the costs that are not "flexed" because they remain the same within a relevant range of activity (such as sales or output) are called ________. A) total overhead costs B) total budgeted costs C) fixed costs D) variable costs Answer: C Diff: 1 Objective: 2 AACSB: Analytical thinking6) Really Great Corporation manufactures industrial-sized landscaping trailers and uses budgeted machine-hours to allocate variable manufacturing overhead. The following information pertains to the company's manufacturing overhead data: Budgeted output units 40,000 units Budgeted machine-hours 10,000 hours Budgeted variable manufacturing overhead costs for 40,000 units$310,000 Actual output units produced 36,500 units Actual machine-hours used 14,600 hours Actual variable manufacturing overhead costs $350,400 What is the budgeted variable overhead cost rate per output unit? A) $9.60 B) $12.40 C) $7.75 D) $31.00 Answer: C Explanation: Machine hour per unit = 10,000 ÷ 40,000 = 0.25 Budgeted cost per machine hour = $310,000 ÷ 10,000 = $31.00 Budgeted cost per unit = $31.00 × 0.25 = $7.75 Diff: 2 Objective: 2 AACSB: Application of knowledge 7) Home Plate Corporation manufactures baseball uniforms and uses budgeted machinehours to allocate variable manufacturing overhead. The following information pertains to the company's manufacturing overhead data: Budgeted output units 7,000 units Budgeted machine-hours 19,000 hours Budgeted variable manufacturing overhead costs for 7,000 units$119,000 Actual output units produced 6,000 units Actual machine-hours used 18,000 hours Actual variable manufacturing overhead costs $108,000 What is the budge [Show More]

Last updated: 1 year ago

Preview 1 out of 71 pages

Instant download

Buy this document to get the full access instantly

Instant Download Access after purchase

Add to cartInstant download

Also available in bundle (2)

Cost Accounting: A Managerial Emphasis, 16e (Horngren) QUESTIONS AND ANSWERS-A COMPREHENSIVE COLLECTION CO,PLETE FOR EXAM PREPARATION- GRADED A+

Cost Accounting: A Managerial Emphasis, 16e (Horngren) QUESTIONS AND ANSWERS-A COMPREHENSIVE COLLECTION CO,PLETE FOR EXAM PREPARATION- GRADED A+

By d.occ 2 years ago

$53

13

ACCOUNTING QUESTIONS, SOLUTIONS & EXPLANATIONS-VERIFIED BY EXPERTS-A COMPLETE GUIDE FOR EAXAM PREPARATION-GRADED A+

ACCOUNTING QUESTIONS, SOLUTIONS & EXPLANATIONS-VERIFIED BY EXPERTS-A COMPLETE GUIDE FOR EAXAM PREPARATION-GRADED A+

By d.occ 2 years ago

$45

8

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jul 09, 2021

Number of pages

71

Written in

Additional information

This document has been written for:

Uploaded

Jul 09, 2021

Downloads

0

Views

64