Management > QUESTIONS & ANSWERS > Georgia Institute Of TechnologyMGT 6203MGT6203Final_ExtraCreditQns LATEST FOR 2021/2022 (All)

Georgia Institute Of TechnologyMGT 6203MGT6203Final_ExtraCreditQns LATEST FOR 2021/2022

Document Content and Description Below

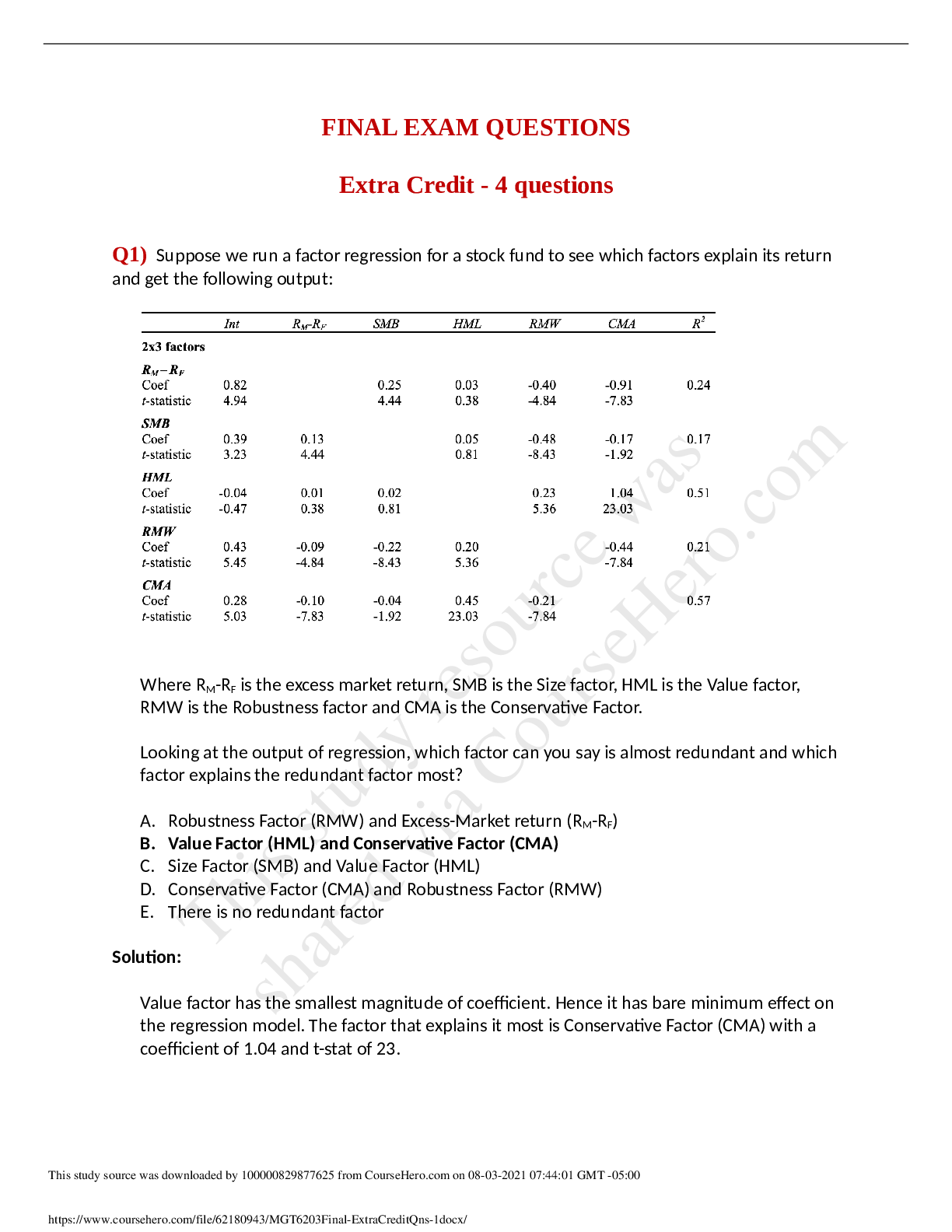

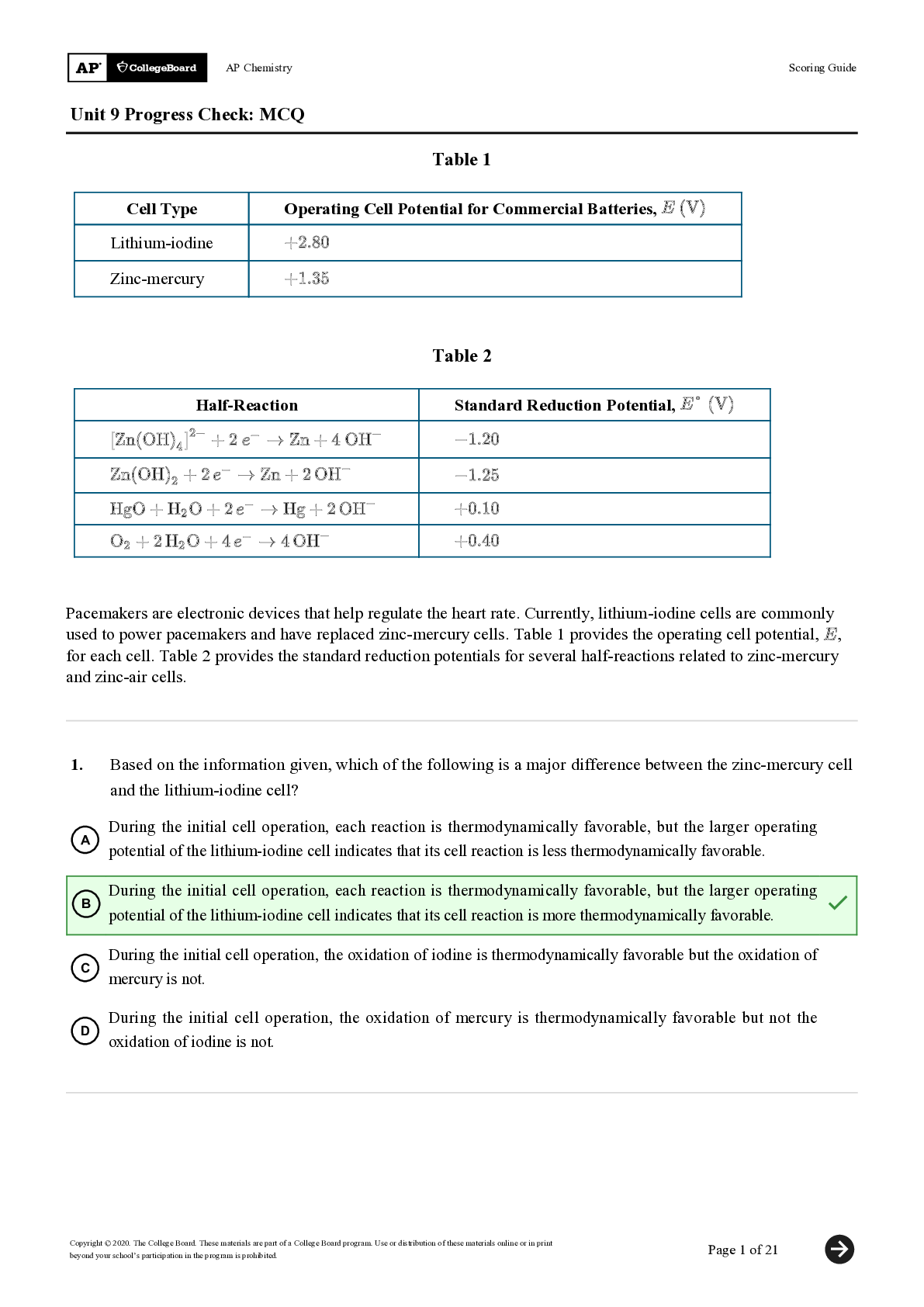

FINAL EXAM QUESTIONS Extra Credit - 4 questions Q1) Suppose we run a factor regression for a stock fund to see which factors explain its return and get the following output: Where RM-RF is the exc ess... market return, SMB is the Size factor, HML is the Value factor, RMW is the Robustness factor and CMA is the Conservative Factor. Looking at the output of regression, which factor can you say is almost redundant and which factor explains the redundant factor most? A. Robustness Factor (RMW) and Excess-Market return (RM-RF) B. Value Factor (HML) and Conservative Factor (CMA) C. Size Factor (SMB) and Value Factor (HML) D. Conservative Factor (CMA) and Robustness Factor (RMW) E. There is no redundant factor Solution: Value factor has the smallest magnitude of coefficient. Hence it has bare minimum effect on the regression model. The factor that explains it most is Conservative Factor (CMA) with a coefficient of 1.04 and t-stat of 23. [Show More]

Last updated: 1 year ago

Preview 1 out of 3 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Aug 03, 2021

Number of pages

3

Written in

Additional information

This document has been written for:

Uploaded

Aug 03, 2021

Downloads

0

Views

26

.png)