Microeconomics > EXAM > Foundations of Microeconomics Scarcity, Choice, and Opportunity Cost. 25 Questions and Answers. Nich (All)

Foundations of Microeconomics Scarcity, Choice, and Opportunity Cost. 25 Questions and Answers. Nichols College; MICROECONO Graded 100%.

Document Content and Description Below

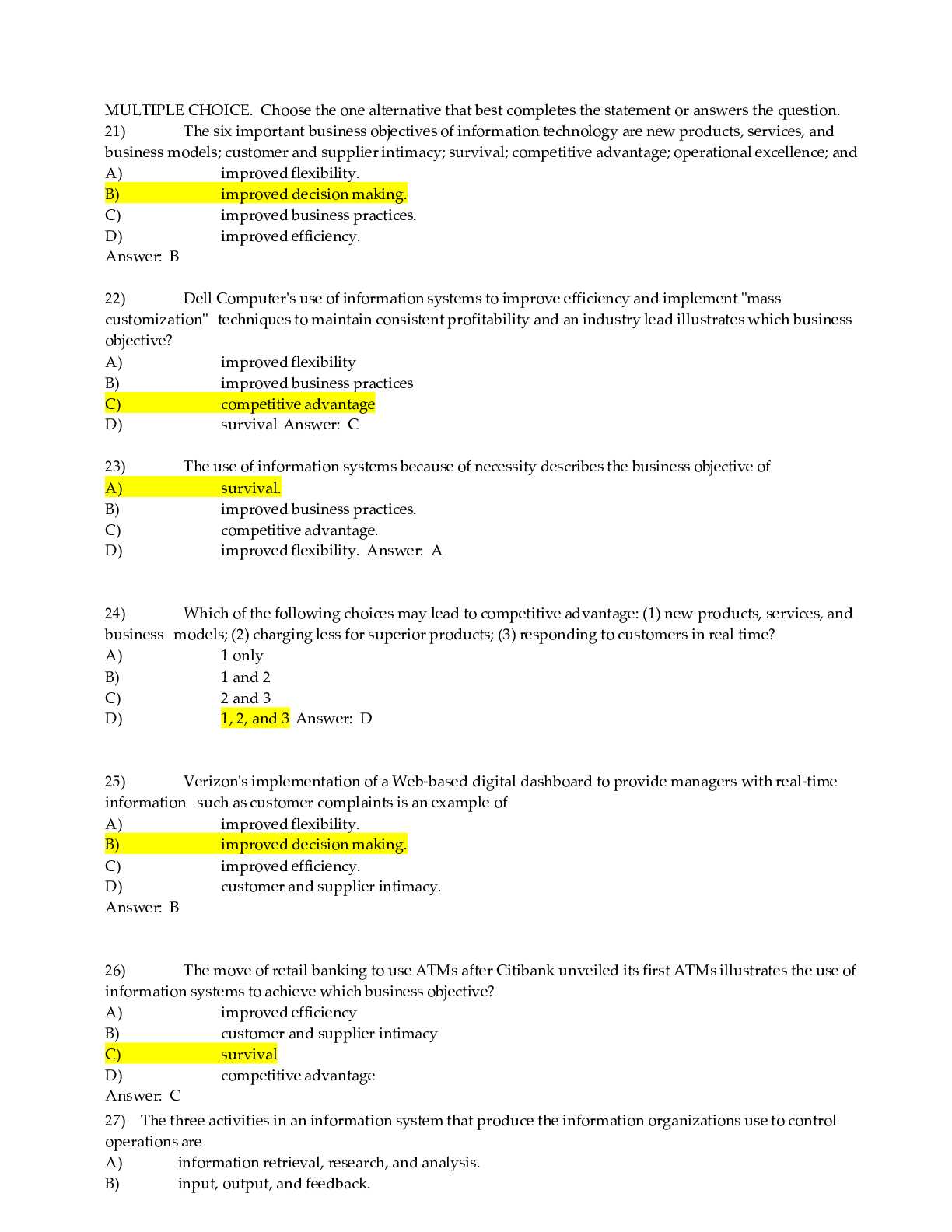

Foundations of Microeconomics Scarcity, Choice, and Opportunity Cost People respond to incentives blank_______. A by ignoring negative incentives and responding to positive incentives only B only ... when they are irrational C by calculating their individual costs and benefits and determining which is greater D when they have low incomes Because the resources immediately available for use are limited, blank_______. A only the wealthiest people will get everything they want B people must make choices about resource use C eventually population growth will exceed resource availability, leading to famine and starvation D markets can become arenas for vicious competition between producers and consumers An incentive blank_______. A is the opposite of a tradeoff / B could be a reward but could not be a punishment C could be either a reward or a punishment D could be a punishment but could not be a reward In economics, the opportunity cost of doing something is blank_______. A total costs B the money, out-of-pocket expenditure C the value of the next best opportunity not taken D the value that you place on the opportunity taken The optimal amount of studying is determined by comparing the blank_______. A marginal benefit and the total cost of studying B marginal benefit and the total benefit of studying C marginal benefit and the marginal cost of studying / D total benefit and marginal cost of studying Supply and Demand For any good or service, we can represent the quantity demanded under various prices by blank_________. A a demand curve B a point on a demand curve C the value of goods and services purchased and held by consumers D the intercept on the Y-axis Potatoes are used in the production of potato chips. Suppose the price of potatoes falls. Then,_______. A it is likely that the demand for potato chips will fall B it is likely that a movement along the supply curve of potato chips will occur C it is unlikely that there will be a change in demand or supply / D it is likely an outward shift in the supply curve of potato chips Given that digital music players are used to play music downloaded from the Internet, a fall in the price of digital music players will lead to blank_______. A an increase in the price of broadband plans B an increase in the price of personal laptops C an increase in the demand for downloaded songs D a decrease in the price of a song download Which of the following would necessarily cause a decrease in the price of a product? A An increase in the number of buyers and a decrease in the price of an input. B An increase in the number of buyers and a decrease in the number of firms producing the product. C A decrease in the price of a substitute product and an improvement in production technology. D An increase in average income and an improvement in production technology. Suppose the price of hamburgers rises, and you observe that as a result, the demand for hotdogs rises. This makes hotdogs and hamburgers blank_______. A normal goods / B complements C substitutes D inferior goods Elasticity Suppose the demand is perfectly inelastic. The implication would be that the smallest change in price would result in________. A no change in quantity B a small change in quantity C no change in price D a small change in price For goods and services that have an elastic demand, if price is increased, total revenue_______. A does not change B is not a function of price / C decreases D increases Goods and services that are independent of each other have a cross elasticity of demand that is ________. A negative B positive C 0 D positive infinity A perfectly elastic demand is a ___________curve. A vertical B horizontal C negative D positive Which of the following products is likely to have the most elastic demand? / A Cigarettes B Coca Cola C Life-saving medicine D Gasoline Production and Costs What of the following statements best summarizes the law of diminishing marginal returns? A As more labor is hired, the length of time that defines the short run diminishes. B In the short run, as more labor is hired, output diminishes. C In the short run, the amount of labor a firm will hire diminishes as output increases. / D In the short run, as more labor is hired, output increases at a diminishing rate. A legal entity, in its own right, that can be closely held (with few shareholders) or widely held (with hundreds of thousands of shareholders is called________. A sole proprietorship B partnership C cooperative D corporation All other inputs remaining the same, the additional output that may result from an additional unit of labor is________. A marginal cost B marginal product C marginal revenue D marginal utility Average total costs is equal to which of the following? A The sum of average variable costs, average fixed costs, and marginal costs / B The product of average variable costs and quantity produced C Total variable costs divided by total marginal costs D The sum of average variable costs and average fixed costs Profit maximization occurs when_____________. A firm expands output until marginal revenue is exceeded by marginal cost B a firm expands output until marginal revenue is equal to marginal cost C the price in the market is equal to the firm’s marginal revenue D total costs equal total revenue / Powered by TCPDF (www.tcpdf.org) [Show More]

Last updated: 11 months ago

Preview 1 out of 9 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Nov 09, 2021

Number of pages

9

Written in

Additional information

This document has been written for:

Uploaded

Nov 09, 2021

Downloads

0

Views

161