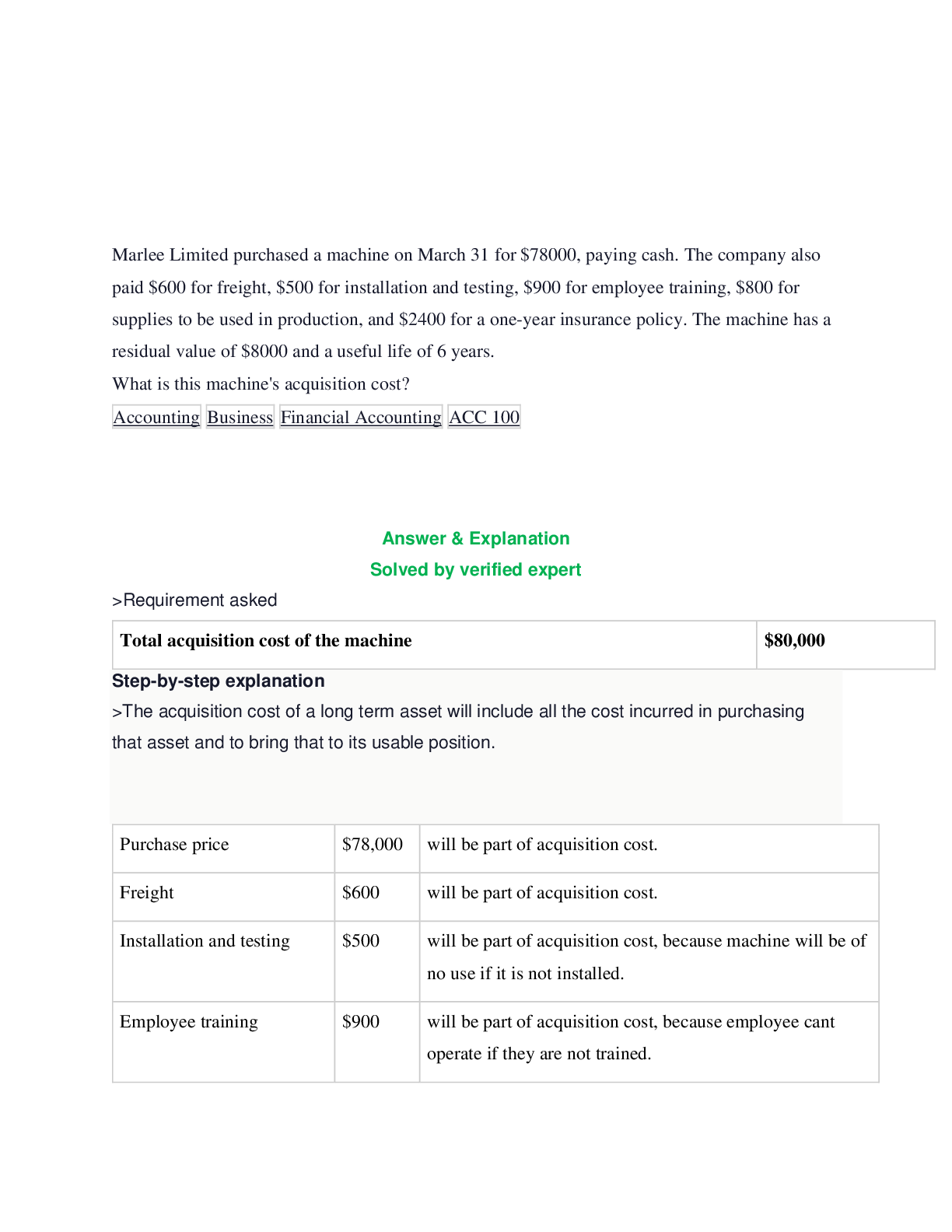

Accounting > QUESTIONS & ANSWERS > Questions and Answers >Business Financial ACCOUNTING 101 (All)

Questions and Answers >Business Financial ACCOUNTING 101

Document Content and Description Below

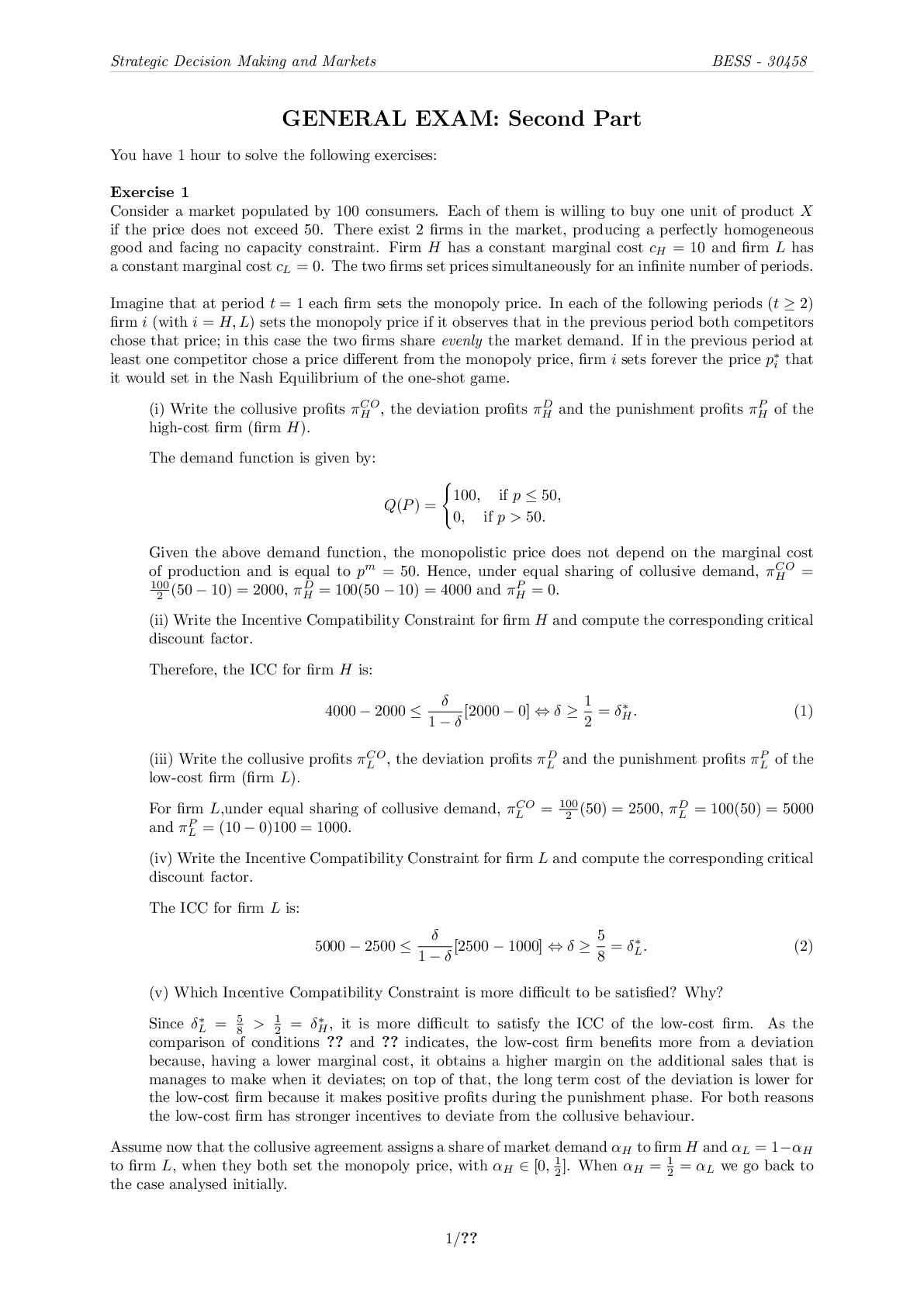

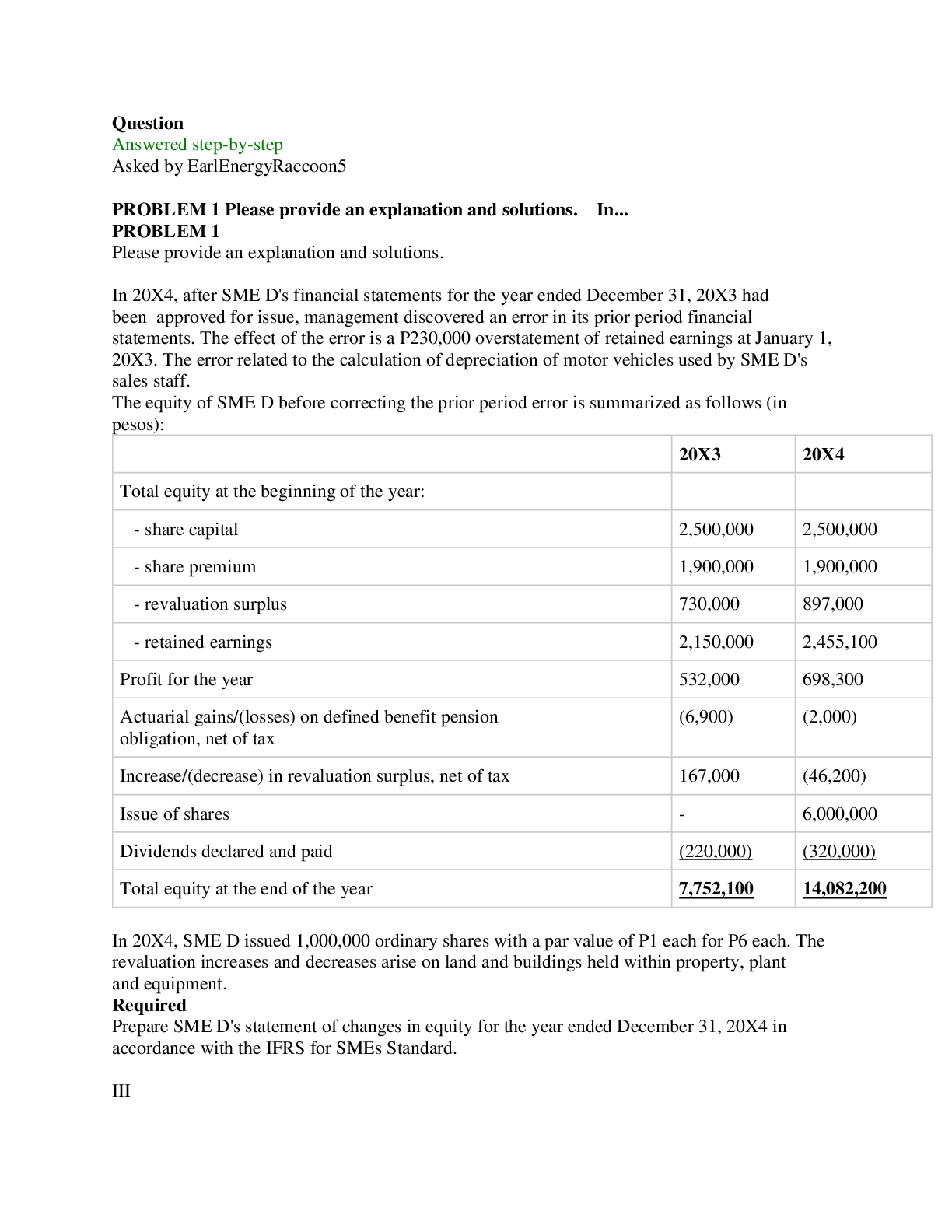

In 20X4, after SME D's financial statements for the year ended December 31, 20X3 had been approved for issue, management discovered an error in its prior period financial statements. The effect of t... he error is a P230,000 overstatement of retained earnings at January 1, 20X3. The error related to the calculation of depreciation of motor vehicles used by SME D's sales staff. The equity of SME D before correcting the prior period error is summarized as follows (in pesos): 20X3 20X4 Total equity at the beginning of the year: - share capital 2,500,000 2,500,000 - share premium 1,900,000 1,900,000 - revaluation surplus 730,000 897,000 - retained earnings 2,150,000 2,455,100 Profit for the year 532,000 698,300 Actuarial gains/(losses) on defined benefit pension obligation, net of tax (6,900) (2,000) Increase/(decrease) in revaluation surplus, net of tax 167,000 (46,200) Issue of shares - 6,000,000 Dividends declared and paid (220,000) (320,000) Total equity at the end of the year 7,752,100 14,082,200 In 20X4, SME D issued 1,000,000 ordinary shares with a par value of P1 each for P6 each. The revaluation increases and decreases arise on land and buildings held within property, plant and equipment. Required Prepare SME D's statement of changes in equity for the year ended December 31, 20X4 in accordance with the IFRS for SMEs Standard. IIISME A has a new accountant who has prepared the following draft consolidated statement of financial position at December 31, 20X1. The draft statement of financial position contains a number of errors. Assume that all items have been correctly recognized and that all the errors are presentational. SME A Draft statement of financial position For the year ended December 20X1 (in thousand pesos) Cash 200 Cash equivalents 30 Non-controlling interests' share of profit for the year 120 Dividends declared by SME A 100 Trade receivable 1,900 Inventory, cost 1,000 Inventory, fair value less costs to complete and sell 180 Investment property, fair value 2,500 Property, plant and equipment, cost 4,324 Total assets 10,354 Long-term debt (P500 principal due on January 1 each year) 2,300 Interest accrued on long-term debt (due in less than 12 months) 230 Share capital 1,500 Retained earnings at the beginning of the year 1,910 Profit for the year 1,000 Non-controlling interest 730 Accumulated depreciation on property, plant and equipment 1,450 Provision for doubtful receivables 200 Trade payables 250 Accrued expenses 4 Warranty provision (expires 12 months after the date of sale) 400Environmental provision (restoration is expected to take place in 20X9) 280 Dividends payable 100 Total liabilities and equity 10,354 Required Prepare, in compliance with the IFRS for SMEs Standard, schedules of the following sections of the consolidated statement of financial position at December 31, 20X1. 1. Current assets 2. Non-current assets 3. Current liabilities 4. Non-current liabilities 5. Shareholders' equity broken down into (a) equity attributable to owners of the parent, (and (b) non-controlling interest. Accounting Business Financial ACCOUNTING 101 Share Question [Show More]

Last updated: 1 year ago

Preview 1 out of 6 pages

Buy this document to get the full access instantly

Instant Download Access after purchase

Add to cartInstant download

We Accept:

Reviews( 0 )

$4.00

Document information

Connected school, study & course

About the document

Uploaded On

Jan 15, 2023

Number of pages

6

Written in

Additional information

This document has been written for:

Uploaded

Jan 15, 2023

Downloads

0

Views

62