Economics > STUDY GUIDE > ECON 213 Questions and Answers Latest Updated 2020/2021 Best Study Guide (All)

ECON 213 Questions and Answers Latest Updated 2020/2021 Best Study Guide

Document Content and Description Below

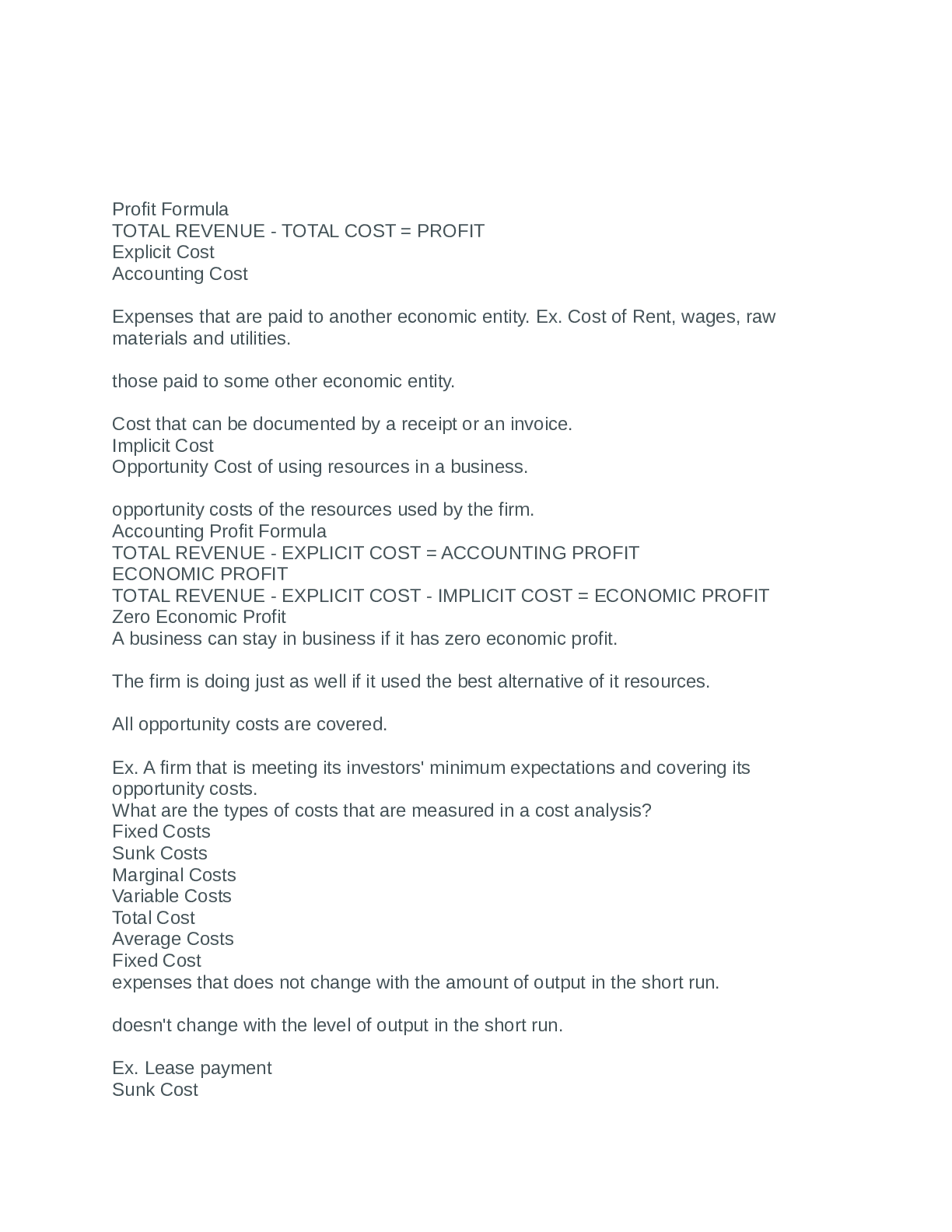

Profit Formula TOTAL REVENUE - TOTAL COST = PROFIT Explicit Cost Accounting Cost Expenses that are paid to another economic entity. Ex. Cost of Rent, wages, raw materials and utilities. those pa... id to some other economic entity. Cost that can be documented by a receipt or an invoice. Implicit Cost Opportunity Cost of using resources in a business. opportunity costs of the resources used by the firm. Accounting Profit Formula TOTAL REVENUE - EXPLICIT COST = ACCOUNTING PROFIT ECONOMIC PROFIT TOTAL REVENUE - EXPLICIT COST - IMPLICIT COST = ECONOMIC PROFIT Zero Economic Profit A business can stay in business if it has zero economic profit. The firm is doing just as well if it used the best alternative of it resources. All opportunity costs are covered. Ex. A firm that is meeting its investors' minimum expectations and covering its opportunity costs. What are the types of costs that are measured in a cost analysis? Fixed Costs Sunk Costs Marginal Costs Variable Costs Total Cost Average Costs Fixed Cost expenses that does not change with the amount of output in the short run. doesn't change with the level of output in the short run. Ex. Lease payment Sunk Cost a cost that can't be recovered. Ex. Tuition payment (no refund) Variable Cost expenses that increase with the amount of production. These include Raw materials, utilities, and labor wages because greater output requires more resources to be used. increase as the level of production increases. Total Cost The sum of Fixed and Variable costs. Used in the Profit formula Marginal Cost The cost of producing one more unit of a good. The additional cost of producing one more unit of a good Average Cost Used to determine the overall efficiency of a business. Includes average fixed cost, average variable cost, and average total cost. AVERAGE "VARIABLE" COST = "VARIABLE" COST/ OUTPUT Profit-Maximizing Rule Profit is maximized when marginal cost equals marginal revenue. If a business has revenue of $100,000, explicit costs of $50,000, and implicit costs of $60,000, it is earning an economic profit. True or False False Because economic profit includes both explicit costs (paid to another economic entity) and implicit costs (the opportunity cost, not otherwise captured, of resources supporting the business), this example would produce a loss ($100,000 − $50,000 − $60,000 = − $10,000). When a business sells an excess factory, it is incurring a sunk cost. True or False False Because this business is recovering at least a portion of its fixed costs by selling the factory, the fixed costs associated with the factory are not a sunk cost. Sunk costs are not recoverable. If a firm's total cost increases by $25 when it produces an additional unit of output, an economist would say that the marginal cost for that unit is $25. True or false True The marginal cost for a unit of output is the additional cost the firm incurs to produce that additional unit. How would a business owner use information about marginal revenue versus marginal cost and price versus average total cost? A business would use the information about marginal revenue vs marginal cost to determine whether or not their profit is maximized. A business would use the information regarding price vs average total cost to evaluate whether or not the business is profitable. The profit maximizing rule (marginal revenue equal to marginal cost) tells the business owner the level of output and price that will maximize the firm's profits, though not its level of profits (or losses). Price less average total cost indicates to the business owner the level of profit (or loss) per unit of output the firm is realizing. A firm that is generating zero economic profit after implicit costs are factored in is earning: implicit profits. normal profits. explicit profits. economic profits. normal profits. A firm that is generating zero economic profit after implicit costs are factored in is earning normal profits. Total output divided by the number of workers is: total product. marginal product. average product. total cost. average product. Average product is calculated by dividing the total output by the number of workers. What illustrates the lowest unit cost at which any particular output can be produced in the long run? short-run average total cost short-run average fixed cost long-run average fixed cost long-run average total cost long-run average total cost The long-run average total cost is the lowest unit cost at which any particular output can be produced in the long run, when a firm is able to adjust all of the factors of production. A corporation: is subject to unlimited liability. is a business in which stockholders' risk is limited to loss of their investment. is a business in which stockholders' risk is not limited to loss of their investment. has the same liability as a partnership. is a business in which stockholders' risk is limited to loss of their investment. A corporation is a business structure that has most of the legal rights of individuals and can issue stock to raise capital. Its stockholders' risk is limited to loss of their investment A company has diminishing marginal returns. If the third worker adds 7 units to total production, how much does the fourth worker add to total production? between 7 and 15 units between 1 and 6 units 8 units no units between 1 and 6 units Diminishing marginal returns occur when an additional worker adds to total output but at a diminishing rate. economies of scale When a firm has economies of scale, its long-run average total costs decrease with increased output. Economies of scale can result from specialization of labor and management, better use of capital, and increased possibilities for making several products that utilize complementary production techniques. A firm is an economic institution that transforms _____ into outputs for consumers. inputs revenue explicit costs profit inputs A firm is an economic institution that transforms inputs, or factors of production, into outputs for consumers. Smaller plants will have _____ short-run average costs at lower levels of output as (than) medium-size or large plants. the same higher lower Smaller plants will have no short-run average costs lower Smaller plants will have lower short-run average costs at lower levels of output. Which of the following is an explicit cost? wages the owner could have made at his or her old job depreciation of a work truck interest that could have been e [Show More]

Last updated: 1 year ago

Preview 1 out of 161 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Dec 19, 2021

Number of pages

161

Written in

Additional information

This document has been written for:

Uploaded

Dec 19, 2021

Downloads

0

Views

109

.png)