Business > QUESTIONS & ANSWERS > ACCT 201A Exam II Review test solution docs (All)

ACCT 201A Exam II Review test solution docs

Document Content and Description Below

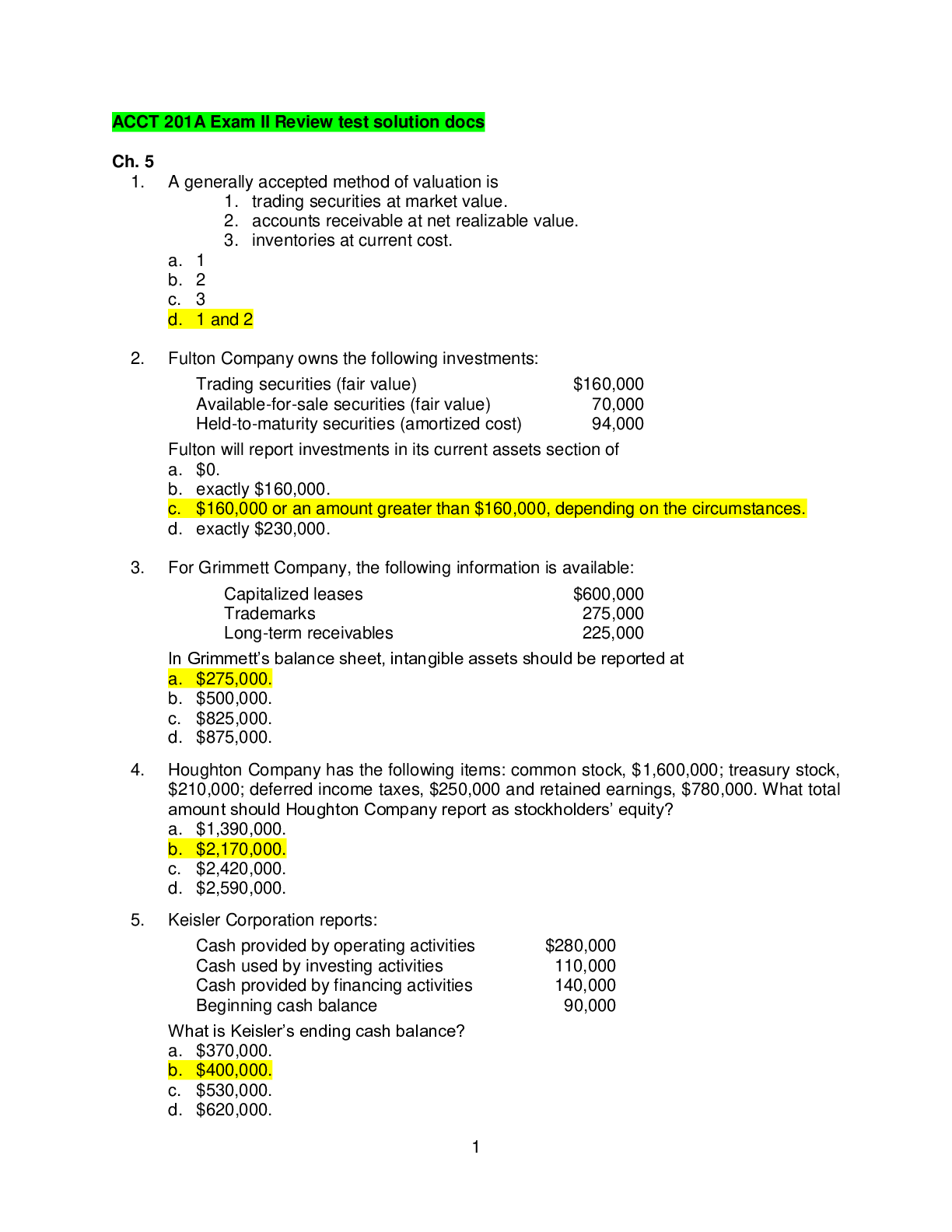

ACCT 201A Exam II Review test solution docs Ch. 5 1. A generally accepted method of valuation is 1. trading securities at market value. 2. accounts receivable at net realizable value. 3. inv... entories at current cost. a. 1 b. 2 c. 3 d. 1 and 2 2. Fulton Company owns the following investments: Trading securities (fair value) $160,000 Available-for-sale securities (fair value) 70,000 Held-to-maturity securities (amortized cost) 94,000 Fulton will report investments in its current assets section of a. $0. b. exactly $160,000. c. $160,000 or an amount greater than $160,000, depending on the circumstances. d. exactly $230,000. 3. For Grimmett Company, the following information is available: Capitalized leases $600,000 Trademarks 275,000 Long-term receivables 225,000 In Grimmett’s balance sheet, intangible assets should be reported at a. $275,000. b. $500,000. c. $825,000. d. $875,000. 4. Houghton Company has the following items: common stock, $1,600,000; treasury stock, $210,000; deferred income taxes, $250,000 and retained earnings, $780,000. What total amount should Houghton Company report as stockholders’ equity? a. $1,390,000. b. $2,170,000. c. $2,420,000. d. $2,590,000. 5. Keisler Corporation reports: Cash provided by operating activities $280,000 Cash used by investing activities 110,000 Cash provided by financing activities 140,000 Beginning cash balance 90,000 What is Keisler’s ending cash balance? a. $370,000. b. $400,000. c. $530,000. d. $620,000. 6. During 2017 the DLD Company had a net income of $85,000. In addition, selectedaccounts showed the following changes: Accounts Receivable $3,000 increase Accounts Payable 1,000 increase Buildings 4,000 decrease Depreciation Expense 1,500 increase Bonds Payable 8,000 increase What was the amount of cash provided by operating activities? a. $84,500 b. $85,000 c. $86,500 d. $94,500 7. Harding Corporation reports the following information: Net income $530,000 Depreciation expense 140,000 Increase in accounts receivable 60,000 Harding should report cash provided by operating activities of a. $330,000. b. $450,000. c. $610,000. d. $730,000. 8. Packard Corporation reports the following information: Net cash provided by operating activities $335,000 Average current liabilities 150,000 Average long-term liabilities 100,000 Dividends declared 60,000 Capital expenditures 110,000 Payments of debt 35,000 Packard’s cash debt coverage is a. 1.34. b. 2.23. c. 3.35. d. 3.05. 9. Packard Corporation reports the following information: Net cash provided by operating activities $335,000 Average current liabilities 150,000 Average long-term liabilities 100,000 Dividends paid 60,000 Capital expenditures 110,000 Payments of debt 35,000 Packard’s free cash flow is a. $130,000. b. $165,000. c. $225,000. d. $275,000. 10. Huge Cart Inc. gives you the following information pertaining to the year 2017. Net sales $850,000 Cost of goods sold 500,000 Current assets 500,000 Current liabilities 250,000 Average total assets 1,000,000 Total liabilities 550,000 Net income 150,000 The asset turnover ratio of Huge Cart Inc. is a. 0.50 b. 0.15 c. 0.85 d. 1.18 11.Huge Cart Inc. gives you the following information pertaining to the year 2017. Net sales $850,000 Cost of goods sold 500,000 Current assets 500,000 Current liabilities 250,000 Average total assets 1,000,000 Total liabilities 550,000 Net income 150,000 The rate of return on assets Huge Cart Inc. is: a. 85.0%. b. 30.0%. c. 17.6%. d. 15.0%. MULTIPLE CHOICE—CPA Adapted 12. Stine Corp.'s trial balance reflected the following account balances at December 31, 2017: Accounts receivable (net) $38,000 Trading securities 12,000 Accumulated depreciation on equipment and furniture 30,000 Cash 32,000 Inventory 6,000 Equipment 50,000 Patent 8,000 Prepaid expenses 4,000 Land held for future business site 36,000 In Stine's December 31, 2017 balance sheet, the current assets total is a. $80,000. b. $64,000. c. $54,000. d. $92,000. Use the following information for questions 13 through 15. The following trial balance of Reese Corp. at December 31, 2017 has been properly adjusted except for the income tax expense adjustment. Reese Corp. Trial Balance December 31, 2017 Dr. Cr. Cash $ 875,000 Accounts receivable (net) 2,695,000 Inventory 2,085,000 Property, plant, and equipment (net) 7,566,000 Accounts payable and accrued liabilities $ 1,761,000 Income taxes payable 654,000 Deferred income tax liability 85,000 Common stock 2,350,000 Additional paid-in capital 3,680,000 Retained earnings, 1/1/17 3,490,000 Net sales and other revenues 13,560,000 Costs and expenses 11,180,000 Income tax expenses 1,179,000 $25,580,000 $25,580,000 Other financial data for the year ended December 31, 2017: • Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2019. • The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability. • During the year, estimated tax payments of $525,000 were charged to income tax expense. The current and future tax rate on all types of income is 30%. In Reese's December 31, 2017 balance sheet, 13. The current assets total is a. $6,180,000. b. $5,655,000. c. $5,505,000. d. $5,055,000. 14. The current liabilities total is a. $1,910,000. b. $1,975,000. c. $2,435,000. d. $2,500,000. 15. The final retained earnings balance is a. $4,691,000. b. $4,776,000. c. $5,216,000. d. $5,145,000. 16. On January 4, 2017, Kiley Co. leased a building to Dodd Corp. for a ten-year term at an annual rental of $200,000. At inception of the lease, Kiley received $800,000 covering the first two years' rent of $400,000 and a security deposit of $400,000. This deposit will not be returned to Dodd upon expiration of the lease but will be applied to payment of rent for the last two years of the lease. What portion of the $800,000 should be shown as a current and long-term liability in Kiley's December 31, 2017 balance sheet? Current Liability Long-term Liability a. $0 $800,000 b. $200,000 $400,000 c. $400,000 $400,000 d. $400,000 $200,000 17. In a statement of cash flows, receipts from sales of property, plant, and equipment and other productive assets should generally be classified as cash inflows from a. operating activities. b. financing activities. c. investing activities. d. selling activities. 18. In a statement of cash flows, interest payments to lenders and other creditors should be classified as cash outflows for a. operating activities. b. borrowing activities. c. lending activities. d. financing activities. 19. In a statement of cash flows, proceeds from issuing equity instruments should be classified as cash inflows from a. lending activities. b. operating activities. c. investing activities. d. financing activities. 20. In a statement of cash flows, payments to acquire debt instruments of other entities (other than cash equivalents) should be classified as cash outflows for a. operating activities. b. investing activities. c. financing activities. d. lending activities. 21. Which of the following facts concerning fixed assets should be included in the summary of significant accounting policies? Depreciation Method Composition a. No Yes b. Yes Yes c. Yes No d. No No Problem 1—Balance sheet classifications. The various classifications listed below have been used in the past by Maris Company on its balance sheet. It asks your professional opinion concerning the appropriate classification of each of the items 1-14 below. a. Current Assets f. Current Liabilities b. Investments g. Long-Term Liabilities c. Plant and Equipment h. Common Stock and Paid-in Capital in Excess of Par d. Intangible Assets i. Retained Earnings e. Other Assets Indicate by letter how each of the following items should be classified. If an item need not be reported on the balance sheet, use the letter "X." A letter may be used more than once or not at all. If an item can be classified in more than one category, choose the category most favored by the authors of your textbook. f 1. Employees' payroll deductions. b 2. Cash in sinking fund. f 3. Rent revenue collected in advance. a/e 4. Equipment retired from use and held for sale. d 5. Patents. a 6. Payroll cash fund. x 7. Goods held on consignment. a 8. Accrued revenue on short-term investments. a 9. Advances to salespersons. g 10. Premium on bonds payable due two years from date. f 11. Bank overdraft. x 12. Salaries which company budget shows will be paid to employees within the next year. a 13. Work in process. i 14. Appropriation for bonded indebtedness. Problem 2 —Balance sheet computations. The following accounts appeared on the trail balance of Elbert Company at December 31, 2017. Notes Payable (short-term) $192,000 Accounts Receivable $518,400 Accumulated Depreciation - Bldg. 783,000 Prepaid Insurance 56,250 Supplies 37,800 Salaries and Wages Payable 34,200 Common Stock 1,125,000 Debt Investments (long-term) 281,400 Unappropriated Retained Earnings 318,000 Cash 170,250 Inventory 1,580,250 Bonds Payable Due 1/1/2025 1,200,000 Land 465,000 Allowance for Doubtful Accts. 7,800 Trading Securities 73,200 Copyrights 192,900 Interest Payable 5,700 Notes Receivable (due in 6 months) 138,000 Buildings 1,926,000 Income Taxes Payable 156,000 Accounts Payable 409,950 Preferred Stock 750,000 Additional Paid-in Capital 163,800 Appropriated Retained Earnings 294,000 Instructions Compute each of the following: 1. Total current assets 2. Total property, plant, and equipment 3. Total assets 4. Total current liabilities 5. Total stockholders’ equity 1. Total currents assets: $37,800 + $170,250 – $7,800 + $138,000 + $518,400 + $56,250 + $1,580,250 + $73,200 = $2,566,350 2.Total property, plant, and equipment: ($783,000) + $465,000 + $1,926,000 = $1,608,000 3.Total assets: $2,566,350 + $1,608,000 + $281,400 + $192,900 = $4,648,650 4. Total current liabilities $192,000 + 34,200 +156,000 + 5,700 + 409,950 = $797,850 5. Total stockholders’ equity $750,000 + 294,000 + 1,125,000 + 318,000 + 163,800 = $2,650,800 Problem 3—Statement of cash flows. For each event listed below, select the appropriate category which describes the effect of the event on a statement of cash flows: a. Cash provided/used by operating activities. b. Cash provided/used by investing activities. c. Cash provided/used by financing activities. d. Not a cash flow. c 1. Payment on long-term debt c 2. Issuance of bonds at a premium a 3. Collection of accounts receivable d 4. Cash dividends declared d 5. Issuance of stock to acquire land b 6. Sale of available-for-sale securities (long-term) a 7. Payment of employees' wages c 8. Issuance of common stock for cash a 9. Payment of income taxes payable b 10. Purchase of equipment c 11. Purchase of treasury stock (common) b 12. Sale of real estate held as a long-term investment Problem 4—Statement of cash flows. (L.O. 5) The information shown below is taken from the accounts of Waverly Corporation for the year ended December 31, 2017 Net income $314,000 Amortization of patent 12,000 Proceeds from issuance of common stock 103,000 Decrease in inventory 27,000 Sale of building at a $15,000 gain 85,000 Decrease in accounts payable 15,000 Purchase of equipment 185,000 Payment of cash dividends 24,000 Depreciation expense 55,000 Decrease in accounts receivable 23,000 Payment of mortgage 75,000 Increase in short-term notes payable 8,000 Sale of land at a $5,000 loss 40,000 Purchase of delivery van 33,000 Cash at beginning of year 205,000 Instructions Prepare a statement of cash flows for Robinson Corporation for the year ended December 31, 2017. Waverly Company Statement of Cash Flows For the Years Ended December 31, 2017 Cash flows from operating activities Net income....................................................................................$314,000 Adjustments to reconcile net income to net Cash provided by operating activities: Depreciation expense..........................................$55,000 Amortization expense...........................................12,000 Gain on sale of building........................................(15,000) Loss on sale of land.............................................5,000 Decrease in inventory..........................................27,000 Decrease in accounts payable.............................(15,000) Increase in short-term notes................................8,000 Decrease in accounts receivable.........................23,000 100,000 Net cash provided by operations...................................…………….414,000 Cash flows from investing activities Sale of building....................................................85,000 Sale of land .........................................................40,000 Purchase of equipment........................................(185,000) Purchase of delivery van......................................(33,000) Net cash used by investing activities...........................................(93,000) Cash flows from financing activities Issuance of common stock.....................................103,000 Payment of cash dividends.....................................(24,000) Payment of mortgage.............................................(75,000) Net cash provided by financing activities.…………………................4,000 Net increase in cash..........................................................................325,000 Cash at beginning of year.................................................................205,000 Cash at end of year............................................................................530,000 Ch. 6 1. Al Darby wants to withdraw $20,000 (including principal) from an investment fund at the end of each year for five years. How should he compute his required initial investment at the beginning of the first year if the fund earns 10% compounded annually? a. $20,000 times the future value of a 5-year, 10% ordinary annuity of 1. b. $20,000 divided by the future value of a 5-year, 10% ordinary annuity of 1. c. $20,000 times the present value of a 5-year, 10% ordinary annuity of 1. d. $20,000 divided by the present value of a 5-year, 10% ordinary annuity of 1. 2. Sue Gray wants to invest a certain sum of money at the end of each year for five years. The investment will earn 6% compounded annually. At the end of five years, she will need a total of $40,000 accumulated. How should she compute her required annual invest-ment? a. $40,000 times the future value of a 5-year, 6% ordinary annuity of 1. b. $40,000 divided by the future value of a 5-year, 6% ordinary annuity of 1. c. $40,000 times the present value of a 5-year, 6% ordinary annuity of 1. d. $40,000 divided by the present value of a 5-year, 6% ordinary annuity of 1. MULTIPLE CHOICE—CPA Adapted 3. On January 1, 2017, Gore Co. sold to Cey Corp. $900,000 of its 10% bonds for $796,766 to yield 12%. Interest is payable semiannually on January 1 and July 1. What amount should Gore report as interest expense for the six months ended June 30, 2017? a. $39,838 b. $45,000 c. $47,806 d. $54,000 4. On May 1, 2017, a company purchased a new machine which it does not have to pay for until May 1, 2019. The total payment on May 1, 2019 will include both principal and interest. Assuming interest at a 10% rate, the cost of the machine would be the total payment multiplied by what time value of money factor? a. Future value of annuity of 1 b. Future value of 1 c. Present value of annuity of 1 d. Present value of 1 5. On January 1, 2017, Ball Co. exchanged equipment for a $600,000 zero-interest-bearing note due on January 1, 2020. The prevailing rate of interest for a note of this type at January 1, 2017 was 10%. The present value of $1 at 10% for three periods is 0.75. What amount of interest revenue should be included in Ball's 2018 income statement? a. $0 b. $45,000 c. $49,500 d. $60,000 6. For which of the following transactions would the use of the present value of an ordinary annuity concept be appropriate in calculating the present value of the asset obtained or the liability owed at the date of incurrence? a. A capital lease is entered into with the initial lease payment due one month subsequent to the signing of the lease agreement. b. A capital lease is entered into with the initial lease payment due upon the signing of the lease agreement. c. A ten-year 8% bond is issued on January 2 with interest payable semiannually on January 2 and July 1 yielding 7%. d. A ten-year 8% bond is issued on January 2 with interest payable semiannually on January 2 and July 1 yielding 9%. 7. On January 15, 2017, Dolan Corp. adopted a plan to accumulate funds for environmental improvements beginning July 1, 2021, at an estimated cost of $8,000,000. Dolan plans to make four equal annual deposits in a fund that will earn interest at 10% compounded annually. The first deposit was made on July 1, 2017. Future value factors are as follows: Future value of 1 at 10% for 5 periods 1.61 Future value of ordinary annuity of 1 at 10% for 4 periods 4.64 Future value of annuity due of 1 at 10% for 4 periods 5.11 Dolan should make four annual deposits of a. $1,423,234. b. $1,565,558. c. $1,724,137. d. $2,000,000. 8. On December 30, 2017, AGH, Inc. purchased a machine from Grant Corp. in exchange for a zero-interest-bearing note requiring eight payments of $150,000. The first payment was made on December 30, 2017, and the others are due annually on December 30. At date of issuance, the prevailing rate of interest for this type of note was 11%. Present value factors are as follows: Present Value of Ordinary Present Value of Period Annuity of 1 at 11% Annuity Due of 1 at 11% 7 4.712 5.231 8 5.146 5.712 On AGH's December 31, 2017 balance sheet, the net note payable to Grant is a. $706,800. b. $771,900. c. $785,325. d. $856,800. 9. On January 1, 2017, Ott Co. sold goods to Flynn Company. Flynn signed a zero-interest-bearing note requiring payment of $200,000 annually for seven years. The first payment was made on January 1, 2017. The prevailing rate of interest for this type of note at date of issuance was 10%. Information on present value factors is as follows: Present Value Present Value of Ordinary Period of 1 at 10% Annuity of 1 at 10% 6 .5645 4.3553 7 .5132 4.8684 Ott should record sales revenue in January 2017 of a. $1,071,048. b. $973,680. c. $871,060. d. $714,000. 10. On January 1, 2017, Haley Co. issued ten-year bonds with a face amount of $5,000,000 and a stated interest rate of 8% payable annually on January 1. The bonds were priced to yield 10%. Present value factors are as follows: At 8% At 10% Present value of 1 for 10 periods 0.463 0.386 Present value of an ordinary annuity of 1 for 10 periods 6.710 6.145 The total issue price of the bonds was a. $5,000,000. b. $4,900,000. c. $4,600,000. d. $4,388,000. 11. On July 1, 2017, Ed Wynne signed an agreement to operate as a franchisee of Kwik Foods, Inc., for an initial franchise fee of $900,000. Of this amount, $300,000 was paid when the agreement was signed and the balance is payable in four equal annual payments of $150,000 beginning July 1, 2018. The agreement provides that the down payment is not refundable and no future services are required of the franchisor. Wynne's credit rating indicates that he can borrow money at 14% for a loan of this type. Information on present and future value factors is as follows: Present value of 1 at 14% for 4 periods 0.59 Future value of 1 at 14% for 4 periods 1.69 Present value of an ordinary annuity of 1 at 14% for 4 periods 2.91 Wynne should record the acquisition cost of the franchise on July 1, 2017 at a. $654,000. b. $736,500. c. $900,000. d. $1,014,000. Problem 1—Calculate market price of a bond. On January 1, 2017 Lance Co. issued five-year bonds with a face value of $1,000,000 and a stated interest rate of 12% payable semiannually on July 1 and January 1. The bonds were sold to yield 10%. Present value table factors are: Present value of 1 for 5 periods at 10% .62092 Present value of 1 for 5 periods at 12% .56743 Present value of 1 for 10 periods at 5% .61391 Present value of 1 for 10 periods at 6% .55839 Present value of an ordinary annuity of 1 for 5 periods at 10% 3.79079 Present value of an ordinary annuity of 1 for 5 periods at 12% 3.60478 Present value of an ordinary annuity of 1 for 10 periods at 5% 7.72173 Present value of an ordinary annuity of 1 for 10 periods at 6% 7.36009 Calculate the issue price of the bonds. Ans: NA, LO: 5, Bloom: AP, Difficulty: Difficult, Min: 5, AACSB: Analytic, AICPA BB: None, AICPA FN: Measurement, AICPA PC: Problem Solving, IMA: Investment Decisions, IFRS: None Market interest rate = 10% Market interest rate for a semiannual period = 10% / 2 = 5% r = 0.05 (per semiannual period), n = 10 (semiannual periods) Present value of principal = $1,000,000 x Present value factor for a single payment (5%, 10 periods) = $1,000,000 x 0.61391 = $613,910 Interest payment each semiannual period = $1,000,000 x 6% = $60,000 (Coupon rate for a semiannual period = 12% / 2 = 6%.) Present value of interest payments = Interest payment each semiannual period x Present value factor for an ordinary annuity (5%, 10 periods) = ($1,000,000 x 6%) x 7.72173 = $463,304 Price of bonds = Present value of principal + Present value of interest payments = $613,910 + $463,304 = $1,077,214 Problem 2—Calculation of unknown rent and interest. Pine Leasing Company purchased specialized equipment from Wayne Company on December 31, 2016 for $900,000. On the same date, it leased this equipment to Sears Company for 5 years, the useful life of the equipment. The lease payments begin January 1, 2017 and are made every 6 months until July 1, 2021. Pine Leasing wants to earn 10% annually on its investment. Various Factors at 10% Periods Future Present Future Value of an Present Value of an or Rents Value of $1 Value of $1 Ordinary Annuity Ordinary Annuity 9 2.35795 .42410 13.57948 5.75902 10 2.59374 .38554 15.93742 6.14457 11 2.85312 .35049 18.53117 6.49506 Various Factors at 5% Periods Future Present Future Value of an Present Value of an or Rents Value of $1 Value of $1 Ordinary Annuity Ordinary Annuity 9 1.55133 .64461 11.02656 7.10782 10 1.62889 .61391 12.57789 7.72173 11 1.71034 .58468 14.20679 8.30641 Instructions (a) Calculate the amount of each rent. (b) How much interest revenue will Pine earn in 2017? Ans: NA, LO: 4, Bloom: AP, Difficulty: Difficult, Min: 10-12, AACSB: Analytic, AICPA BB: None, AICPA FN: Measurement, AICPA PC: Problem Solving, IMA: Investment Decisions, IFRS: None (a) Calculation of rent: 7.72173 × 1.05 = 8.10782 (present value of a 10-rent annuity due at 5%.) $900,000 ÷ 8.10782 = $111,004. (b) Interest Revenue during 2017: Rent No. Date Cash Received Interest Revenue Lease Receivable 1 1/1/2017 111,004 - 788,996 2 7/1/2017 111,004 39,449 717,441 None 13/31/17 None 35,872 75,321 Ch. 7 1. Travel advances should be reported as a. supplies. b. cash because they represent the equivalent of money. c. investments. d. none of these answers are correct. 2. What is a compensating balance? a. Savings account balances. b. Margin accounts held with brokers. c. Temporary investments serving as collateral for outstanding loans. d. Minimum deposits required to be maintained in connection with a borrowing arrangement. 3. Under which section of the balance sheet is "cash restricted for plant expansion" reported? a. Current assets. b. Non-current assets. c. Current liabilities. d. Stockholders' equity. 4. A cash equivalent is a short-term, highly liquid investment that is readily convertible into known amounts of cash and a. is acceptable as a means to pay current liabilities. b. has a current market value that is greater than its original cost c. bears an interest rate that is at least equal to the prime rate of interest at the date of liquidation. d. is so near its maturity that it presents insignificant risk of changes in interest rates. 5. Bank overdrafts, if material, should be a. reported as a deduction from the current asset section. b. reported as a deduction from cash. c. netted against cash and a net cash amount reported. d. reported as a current liability. 6. When a company has cash available in another account in the same bank at which an overdraft has occurred, the company will: a. offset the overdraft against cash account. b. report the same in the notes to financial statement. c. report the bank overdraft amount as account payable. d. classify the bank overdraft as compensating balance. 7. Which of the following statements is correct regarding receivables? a. Receivables are written promises of the purchaser to pay for goods or services. b. Receivables are claims held against customers and others for money, goods, or services. c. Receivables are non-financial assets. d. Receivables that are expected to be collected within a year are classified as noncurrent. 8. What is the preferable presentation of accounts receivable from officers, employees, or affiliated companies on a balance sheet? a. As offsets to capital. b. By means of footnotes only. c. As assets but separately from other receivables. d. As trade notes and accounts receivable if they otherwise qualify as current assets. 9. What is the normal journal entry for recording bad debt expense under the allowance method? a. Debit Allowance for Doubtful Accounts, credit Accounts Receivable. b. Debit Allowance for Doubtful Accounts, credit Bad Debt Expense. c. Debit Bad Debt Expense, credit Allowance for Doubtful Accounts. d. Debit Accounts Receivable, credit Allowance for Doubtful Accounts. 10. What is the normal journal entry when writing-off an account as uncollectible under the allowance method? a. Debit Allowance for Doubtful Accounts, credit Accounts Receivable. b. Debit Allowance for Doubtful Accounts, credit Bad Debt Expense. c. Debit Bad Debt Expense, credit Allowance for Doubtful Accounts. d. Debit Accounts Receivable, credit Allowance for Doubtful Accounts. 11. Which of the following is included in the normal journal entry to record the collection of accounts receivable previously written off when using the allowance method? a. Debit Allowance for Doubtful Accounts, credit Accounts Receivable. b. Debit Allowance for Doubtful Accounts, credit Bad Debt Expense. c. Debit Bad Debt Expense, credit Allowance for Doubtful Accounts. d. Debit Accounts Receivable, credit Allowance for Doubtful Accounts. 12. The advantage of relating a company's bad debt expense to its outstanding accounts receivable is that this approach a. gives a reasonably correct statement of receivables in the balance sheet. b. best relates bad debt expense to the period of sale. c. is the only generally accepted method for valuing accounts receivable. d. makes estimates of uncollectible accounts unnecessary. 13. What is imputed interest? a. Interest based on the stated interest rate. b. Interest based on the implicit interest rate. c. Interest based on the average interest rate. d. Interest based on the coupon rate. 14. Antique Company has notes receivable that have a fair value of $920,000 and a carrying amount of $710,000. Antique decides on December 31, 2017, to use the fair value option for these recently-acquired receivables. The adjusting entry to record this change will include a: a. debit to Unrealized Holding Gain or LossIncome for $210,000. b. credit to Notes Receivable for $210,000. c. credit to Unrealized Holding Gain or LossIncome for $210,000. d. debit to Notes Receivable for $920,000. 15. What is "recourse" as it relates to selling receivables? a. The obligation of the seller of the receivables to pay the purchaser in case the debtor fails to pay. b. The obligation of the purchaser of the receivables to pay the seller in case the debtor fails to pay c. The obligation of the seller of the receivables to pay the purchaser in case the debtor returns the product related to the sale. d. The obligation of the purchaser of the receivables to pay the seller if all of the receivables are collected. 16. Which of the following is true when accounts receivable are factored without recourse? a. The transaction may be accounted for either as a secured borrowing or as a sale, depending upon the substance of the transaction. b. The receivables are used as collateral for a promissory note issued to the factor by the owner of the receivables. c. The factor assumes the risk of collectibility and absorbs any credit losses in collecting the receivables. d. The financing cost (interest expense) should be recognized ratably over the collection period of the receivables. 17. Which of the following statements is incorrect regarding the classification of accounts and notes receivable? a. Segregation of the different types of receivables is required if they are material. b. Disclose any loss contingencies that exist on the receivables. c. Any discount or premium resulting from the determination of present value in notes receivable transactions is an asset or liability respectively. d. Valuation accounts should be ap¬propriately offset against the proper receivable accounts. 18. Of the following conditions, which is the only one that is not required if the transfer of receivables with recourse is to be accounted for as a sale? a. The transferor is obligated to make a genuine effort to identify those receiv¬ables that are uncollectible. b. The transferor surrenders control of the future economic benefits of the receivables. c. The transferee cannot require the transferor to repurchase the receivables. d. The transferor's obligation under the recourse provisions can be reasonably estimated. 19. How is days to collect accounts receivable determined? a. 365 days divided by accounts receivable turnover. b. Net sales divided by 365. c. Net sales divided by average net trade receivables. d. Accounts receivable turnover divided by 365 days. 20. What is a possible reason for accounts receivable turnover to increase from one year to the next year? a. Decreased credit sales during a recession. b. Write-off uncollectible receivables. c. Granting credit to customers with lower credit quality. d. Improved collection process. 21. Which of the following is an appropriate reconciling item to the balance per bank in a bank reconciliation? a. Bank service charge. b. Deposit in transit. c. Bank interest. d. Chargeback for NSF check. 22. Which of the following statements is false? a. The imprest petty cash system in effect adheres to the rule of disbursement by check. b. Entries are made to the Petty Cash account only to increase or decrease the size of the fund or to adjust the balance if not replenished at year-end. c. The Petty Cash account is debited when the fund is replenished. d. All of these answers are false. 23. A Cash Over and Short account a. is not generally accepted. b. is debited when the petty cash fund proves out over. c. is debited when the petty cash fund proves out short. d. is a contra account to Cash. 24. The journal entries for a bank reconciliation a. are taken from the "balance per bank" section only. b. may include a debit to Office Expense for bank service charges. c. may include a credit to Accounts Receivable for an NSF check. d. may include a debit to Accounts Payable for an NSF check. 25. When preparing a bank reconciliation, bank credits are a. added to the bank statement balance. b. deducted from the bank statement balance. c. added to the balance per books. d. deducted from the balance per books. 26. Kennison Company has cash in bank of $20,000, restricted cash in a separate account of $3,000, and a bank overdraft in an account at another bank of $1,000. Kennison should report cash of a. $19,000. b. $20,000. c. $22,000. d. $23,000. 27. AG Inc. made a $25,000 sale on account with the following terms: 1/15, n/30. If the company uses the net method to record sales made on credit, how much should be recorded as revenue? a. $24,500. b. $24,750. c. $25,000. d. $25,250. 28. On July 22, Peter sold $23,500 of inventory items on credit with the terms 2/15, net 30. Payment on $15,000 sales was received on August 1 and the remaining payment was received on August 12. Assuming Peter uses the gross method of accounting for sales discounts, which one of the following entries was made on August 1 to record the cash received? a. Cash 14,700 Sales Discount 300 Accounts Receivable 15,000 b. Cash 15,000 Accounts Receivable 15,000 c. Cash 14,700 Accounts Receivable 14,700 d. Accounts Receivable 300 Sales Discount Forfeited 300 29. Wellington Corp. has outstanding accounts receivable totaling $1.27 million as of December 31 and sales on credit during the year of $6.4 million. There is also a debit balance of $6,000 in the allowance for doubtful accounts. If the company estimates that 2% of its accounts receivable will be uncollectible, what will be the balance in the allowance for doubtful accounts after the year-end adjustment to record bad debt expense? a. $19,400. b. $31,400. c. $25,400. d. $25,280. 30. Wellington Corp. has outstanding accounts receivable totaling $6.5 million as of December 31 and sales on credit during the year of $24 million. There is also a credit balance of $12,000 in the allowance for doubtful accounts. If the company estimates that 6% of its outstanding receivables will be uncollectible, what will be the amount of bad debt expense recognized for the year? a. $ 402,000. b. $ 390,000. c. $1,440,000. d. $ 378,000. 31. Wellington Corp. has outstanding accounts receivable totaling $6 million as of December 31 and sales on credit during the year of $30 million. There is also a debit balance of $24,000 in the allowance for doubtful accounts. If the company estimates that 8% of its outstanding receivables will be uncollectible, what will be the balance in the allowance for doubtful accounts after the year-end adjustment to record bad debt expense? a. $2,400,000. b. $ 456,000. c. $ 480,000. d. $ 504,000. 32. At the close of its first year of operations, December 31, 2017, Ming Company had accounts receivable of $1,620,000, after deducting the related allowance for doubtful accounts. During 2017, the company had charges to bad debt expense of $270,000 and wrote off, as uncollectible, accounts receivable of $120,000. What should the company report on its balance sheet at December 31, 2017, as accounts receivable before the allowance for doubtful accounts? a. $2,010,000 b. $1,770,000 c. $1,470,000 d. $1,320,000 33. Lester Company received a seven-year zero-interest-bearing note on February 22, 2017, in exchange for property it sold to Porter Company. There was no established exchange price for this property and the note has no ready market. The prevailing rate of interest for a note of this type was 6% on February 22, 2017, 6.5% on December 31, 2017, 6.7% on February 22, 2018, and 7% on December 31, 2018. What interest rate should be used to calculate the interest revenue from this transaction for the years ended December 31, 2017 and 2018, respectively? a. 0% and 0% b. 6% and 6% c. 6% and 7.7% d. 6.5% and 7% 34. Jones Company has notes receivable that have a fair value of $950,000 and a carrying amount of $1,250,000. Jones decides on December 31, 2017, to use the fair value option for these recently-acquired receivables. Which of the following entries will be made on December 31, 2017 to record the unrealized holding gain/loss? a. Unrealized Holding Gain or LossEquity 300,000 Notes Receivable 300,000 b. Unrealized Holding Gain or LossIncome 300,000 Notes Receivable 300,000 c. Notes Receivable 300,000 Unrealized Holding Gain or LossIncome 300,000 d. Notes Receivable 300,000 Unrealized Holding Gain or LossEquity 300,000 35. Sun Inc. factors $6,000,000 of its accounts receivables without recourse for a finance charge of 5%. The finance company retains an amount equal to 10% of the accounts receivable for possible adjustments. Sun estimates the fair value of the recourse liability at $230,000. What would be recorded as a gain (loss) on the transfer of receivables? a. Loss of $300,000. b. Gain of $530,000. c. Loss of $1,130,000. d. Loss of $230,000. 36. Sun Inc. factors $6,000,000 of its accounts receivables with recourse for a finance charge of 3%. The finance company retains an amount equal to 10% of the accounts receivable for possible adjustments. Sun estimates the fair value of the recourse liability at $300,000. What would be recorded as a gain (loss) on the transfer of receivables? a. Gain of $180,000. b. Loss of 480,000. c. Gain of $1,080,000. d. Loss of $300,000. 37. Geary Co. assigned $1,600,000 of accounts receivable to Kwik Finance Co. as security for a loan of $1,340,000. Kwik charged a 2% commission on the amount of the loan; the interest rate on the note was 10%. During the first month, Geary collected $440,000 on assigned accounts after deducting $1,520 of discounts. Geary accepted returns worth $5,400 and wrote off assigned accounts totaling $11,920. The amount of cash Geary received from Kwik at the time of the assignment was a. $1,206,000. b. $1,308,000. c. $1,313,200. d. $1,340,000. 38. During the year Tulip reported net sales of $960,000. The company had accounts receivable of $75,000 at the beginning of the year and $120,000 at the end of the year Compute Tulip’s average collection period (assume 365 days a year.) a. 28.5 days b. 37.2 days. c. 45.7 days. d. 74.2 days. 39. If a petty cash fund is established in the amount of $300, and contains $180 in cash and $115 in receipts for disbursements when it is replenished, the journal entry to record replenishment should include credits to the following accounts a. Petty Cash, $90. b. Petty Cash, $120. c. Cash, $115; Cash Over and Short, $5. d. Cash, $120. 40. In preparing its bank reconciliation for the month of April 2017, Henke, Inc. has the following information available. Balance per bank statement, 4/30/17 $102,420 NSF check returned with 4/30/17 bank statement 1,350 Deposits in transit, 4/30/17 15,000 Outstanding checks, 4/30/17 15,600 Bank service charges for April 60 What should be the correct balance of cash at April 30, 2017? a. $103,110 b. $101,820 c. $100,470 d. $100,410 MULTIPLE CHOICE—CPA Adapted 41. On the December 31, 2017 balance sheet of Vanoy Co., the current receivables consisted of the following: Trade accounts receivable $ 65,000 Allowance for uncollectible accounts (2,000) Claim against shipper for goods lost in transit (November 2017) 3,000 Selling price of unsold goods sent by Vanoy on consignment at 130% of cost (not included in Vanoy 's ending inventory) 26,000 Security deposit on lease of warehouse used for storing some inventories 30,000 Total $122,000 At December 31, 2017, the correct total of Vanoy's current net receivables was a. $66,000. b. $92,000. c. $96,000. d. $122,000. 42. Ace Co. prepared an aging of its accounts receivable at December 31, 2017 and determined that the net realizable value of the receivables was $900,000. Additional information is available as follows: Allowance for uncollectible accounts at 1/1/17—credit balance $102,000 Accounts written off as uncollectible during 2017 69,000 Accounts receivable at 12/31/17 975,000 Uncollectible accounts recovered during 2017 15,000 For the year ended December 31, 2017, Ace's bad debt expense would be a. $75,000. b. $69,000. c. $48,000. d. $27,000. 43. For the year ended December 31, 2017, Dent Co. estimated its allowance for uncollectible accounts using the year-end aging of accounts receivable. The following data are available: Allowance for uncollectible accounts, 1/1/17 $126,000 Provision for uncollectible accounts during 2017 90,000 Uncollectible accounts written off, 11/30/17 104,000 Estimated uncollectible accounts per aging, 12/31/17 156,000 After year-end adjustment, the bad debt expense for 2017 should be a. $104,000. b. $90,000. c. $156,000. d. $134,000. 44. Nenn Co.'s allowance for uncollectible accounts was $190,000 at the end of 2017 and $180,000 at the end of 2016. For the year ended December 31, 2017, Nenn reported bad debt expense of $31,000 in its income statement. What amount did Nenn debit to the appropriate account in 2017 to write off actual bad debts? a. $10,000 b. $21,000 c. $31,000 d. $41,000 45. Under the allowance method of recognizing uncollectible accounts, the entry to write off an uncollectible account a. increases the allowance for uncollectible accounts. b. has no effect on the allowance for uncollectible accounts. c. has no effect on net income. d. decreases net income. 46. The following accounts were abstracted from Starr Co.'s unadjusted trial balance at December 31, 2017: Debit Credit Accounts receivable $750,000 Allowance for uncollectible accounts 8,000 Net credit sales $3,000,000 Starr estimates that 6% of the gross accounts receivable will become uncollectible. After adjustment at December 31, 2017, the allowance for uncollectible accounts should have a credit balance of a. $180,000. b. $168,000. c. $57,000. d. $45,000. 47. On January 1, 2017, West Co. exchanged equipment for an $800,000 zero-interest-bearing note due on January 1, 2020. The prevailing rate of interest for a note of this type at January 1, 2017 was 10%. The present value of $1 at 10% for three periods is 0.75. What amount of interest revenue should be included in West's 2018 income statement? a. $0 b. $60,000 c. $66,000 d. $80,000 48. On June 1, 2017, Yang Corp. loaned Gant $500,000 on a 12% note, payable in five annual installments of $100,000 beginning January 2, 2018. In connection with this loan, Gant was required to deposit $5,000 in a zero-interest-bearing escrow account. The amount held in escrow is to be returned to Gant after all principal and interest payments have been made. Interest on the note is payable on the first day of each month beginning July 1, 2017. Gant made timely payments through November 1, 2017. On January 2, 2018, Yang received payment of the first principal installment plus all interest due. At December 31, 2017, Yang's interest receivable on the loan to Gant should be a. $0. b. $5,000. c. $10,000. d. $15,000. 49. Which of the following is a method to generate cash from accounts receivable? Assignment Factoring a. Yes No b. Yes Yes c. No Yes d. No No 50. In preparing its August 31, 2017 bank reconciliation, Bing Corp. has available the following information: Balance per bank statement, 8/31/17 $25,650 Deposit in transit, 8/31/17 3,900 Return of customer's check for insufficient funds, 8/30/17 600 Outstanding checks, 8/31/17 2,750 Bank service charges for August 100 At August 31, 2017, Bing's correct cash balance is a. $26,800. b. $26,200. c. $26,100. d. $24,500. 51. Tresh, Inc. had the following bank reconciliation at March 31, 2017: Balance per bank statement, 3/31/17 $74,400 Add: Deposit in transit 20,600 95,000 Less: Outstanding checks 25,200 Balance per books, 3/31/17 $69,800 Data per bank for the month of April 2017 follow: Deposits $87,400 Disbursements 99,400 All reconciling items at March 31, 2017 cleared the bank in April. Outstanding checks at April 30, 2017 totaled $12,000. There were no deposits in transit at April 30, 2017. What is the cash balance per books at April 30, 2017? a. $50,400 b. $57,800 c. $62,400 d. $71,000 Problem 1 Kohl Company lent $66,116 to Hemingway, Inc, accepting Hemingway's 2-year, $80,000, zero-interest-bearing note. The implied interest rate is 10%. Prepare Kohl's journal entries for the initial transaction, recognition of interest each year, and the collection of $80,000 at maturity. Notes Receivable 80,000 Discount on Notes Receivable 13,884 Cash 66,116 Discount on Notes Receivable 6,612 Interest Revenue 6,612 ($66,116*10%) Discount on Notes Receivable 7,273 Interest Revenue 7,273 ($66,116+$6,612)*10% Cash 80,000 Notes Receivable 80,000 Problem 2—Entries for bad debt expense. The trial balance before adjustment of Risen Company reports the following balances: Dr. Cr. Accounts receivable $300,000 Allowance for doubtful accounts $ 5,000 Sales (all on credit) 1,700,000 Sales returns and allowances 80,000 Instructions (a) Prepare the entry for estimated bad debts assuming that doubtful accounts are estimated to be 6% of gross accounts receivable. (b) Assume that all the information above is the same, except that the Allowance for Doubtful Accounts has a debit balance of $5,000 instead of a credit balance. How will this difference affect the journal entry in part (a)? (c) What is the theoretical justification for the percentage-of-receivables method used to estimate bad debts? Ans: NA, LO: 3, Bloom: AP, Difficulty: Difficult, Min: 15-20, AACSB: Analytic, AICPA BB: None, AICPA FN: Measurement, AICPA PC: Problem Solving, IMA: Reporting, IFRS: None A Bad Debt Expense 13,000 Allowance for Doubtful Accounts 13,000 Gross receivables 300,000 Rate 6% Total Allowance needed 18,000 Present allowance (5,000) Bad Debt Expense 13,000 B Bad Debt Expense 23,000 Allowance for Doubtful Accounts 23,000 Gross receivables 300,000 Rate 6% Total Allowance needed 18,000 Present allowance 5,000 Bad Debt Expense 23,000 C percentage-of-receivables method estimates bad debts based on the balance in the accounts receivable account. This method focuses on the balance sheet and attempts to value the account receivable at their net realizable value. Ch. 8 1. Lawson Manufacturing Company has the following account balances at year end: Office supplies $ 4,000 Raw materials 27,000 Work-in-process 59,000 Finished goods 109,000 Prepaid insurance 6,000 What amount should Lawson report as inventories in its balance sheet? a. $109,000. b. $113,000. c. $195,000. d. $199,000. 2. Elkins Corporation uses the perpetual inventory and the gross method. On March 1, it purchased $50,000 of inventory, terms 2/10, n/30. On March 3, Elkins returned goods that cost $5,000. On March 9, Elkins paid the supplier. On March 9, Elkins should credit a. purchase discounts for $1,000. b. inventory for $1,000. c. purchase discounts for $900. d. inventory for $900. 3. Malone Corporation uses the perpetual inventory and the gross method. On March 1, it purchased $80,000 of inventory, terms 2/10, n/30. On March 3, Malone returned goods that cost $8,000. On March 9, Malone paid the supplier. On March 9, Malone should credit a. purchase discounts for $1,600. b. inventory for $1,600. c. purchase discounts for $1,440. d. inventory for $1,440. 4. Bell Inc. took a physical inventory at the end of the year and determined that $780,000 of goods were on hand. In addition, Bell, Inc. determined that $60,000 of goods that were in transit that were shipped f.o.b. shipping point were actually received two days after the inventory count and that the company had $90,000 of goods out on consignment. What amount should Bell report as inventory at the end of the year? a. $780,000. b. $860,000. c. $870,000. d. $930,000. 5. Bell Inc. took a physical inventory at the end of the year and determined that $840,000 of goods were on hand. In addition, the following items were not included in the physical count. Bell, Inc. determined that $96,000 of goods purchased were in transit that were shipped f.o.b. destination (goods were actually received by the company three days after the inventory count).The company sold $40,000 worth of inventory f.o.b. destination. What amount should Bell report as inventory at the end of the year? a. $840,000. b. $936,000. c. $880,000. d. $976,000. 6. The following information is available for Naab Company for 2017: Freight-in $ 60,000 Purchase returns 150,000 Selling expenses 460,000 Ending inventory 520,000 The cost of goods sold is equal to 400% of selling expenses. What is the cost of goods available for sale? a. $1,840,000. b. $2,300,000. c. $2,370,000. d. $2,360,000. Use the following information for questions 7 and 8. The following information was available from the inventory records of Rich Company for January: Units Unit Cost Total Cost Balance at January 1 9,000 $9.77 $87,930 Purchases: January 6 6,000 10.30 61,800 January 26 8,100 10.71 86,751 Sales: January 7 (7,500) January 31 (11,100) Balance at January 31 4,500 7. Assuming that Rich does not maintain perpetual inventory records, what should be the inventory at January 31, using the weighted-average inventory method, rounded to the nearest dollar? a. $47,270. b. $46,067. c. $46,170. d. $46,620. 8. Assuming that Rich maintains perpetual inventory records, what should be the inventory at January 31, using the moving-average inventory method, rounded to the nearest dollar? a. $47,270. b. $46,067. c. $46,170. d. $46,620. 9. June Corp. sells one product and uses a perpetual inventory system. The beginning inventory consisted of 80 units that cost $20 per unit. During the current month, the company purchased 480 units at $20 each. Sales during the month totaled 360 units for $43 each. What is the cost of goods sold using the LIFO method? a. $1,600. b. $7,200. c. $9,600. d. $15,480. 10. Checkers uses the periodic inventory system. For the current month, the beginning inventory consisted of 7,200 units that cost $12 each. During the month, the company made two purchases: 3,000 units at $13 each and 12,000 units at $13.50 each. Checkers also sold 12,900 units during the month. Using the average cost method, what is the amount of cost of goods sold for the month? a. $167,055. b. $173,700. c. $161,850. d. $167,700. 11. Checkers uses the periodic inventory system. For the current month, the beginning inventory consisted of 7,200 units that cost $12 each. During the month, the company made two purchases: 3,000 units at $13 each and 12,000 units at $13.50 each. Checkers also sold 12,900 units during the month. Using the FIFO method, what is the ending inventory? a. $120,438. b. $111,600. c. $125,550. d. $113,700. 12. Chess Top uses the periodic inventory system. For the current month, the beginning inventory consisted of 480 units that cost $65 each. During the month, the company made two purchases: 720 units at $68 each and 360 units at $70 each. Chess Top also sold 1,200 units during the month. Using the FIFO method, what is the amount of cost of goods sold for the month? a. $81,048. b. $78,000. c. $81,960. d. $80,160. 13. Checkers uses the periodic inventory system. For the current month, the beginning inventory consisted of 7,200 units that cost $12 each. During the month, the company made two purchases: 3,000 units at $13 each and 12,000 units at $13.50 each. Checkers also sold 12,900 units during the month. Using the LIFO method, what is the ending inventory? a. $120,438. b. $111,600. c. $125,550. d. $113,700. 14. Chess Top uses the periodic inventory system. For the current month, the beginning inventory consisted of 480 units that cost $65 each. During the month, the company made two purchases: 720 units at $68 each and 360 units at $70 each. Chess Top also sold 1,200 units during the month. Using the LIFO method, what is the amount of cost of goods sold for the month? a. $81,048. b. $78,000. c. $81,960. d. $80,160. 15. Milford Company had 600 units of “Tank” in its inventory at a cost of $6 each. It purchased 900 more units of “Tank” at a cost of $9 each. Milford then sold 1,050 units at a selling price of $15 each. The LIFO liquidation overstated normal gross profit by a. $ -0- b. $450. c. $900. d. $1,350. 16. Wise Company adopted the dollar-value LIFO method on January 1, 2017, at which time its inventory consisted of 6,000 units of Item A @ $5.00 each and 3,000 units of Item B @ $16.00 each. The inventory at December 31, 2017 consisted of 12,000 units of Item A and 7,000 units of Item B. The most recent actual purchases related to these items were as follows: Quantity Items Purchase Date Purchased Cost Per Unit A 12/7/17 2,000 $ 6.00 A 12/11/17 10,000 5.75 B 12/15/17 7,000 17.00 Using the double-extension method, what is the price index for 2017 that should be computed by Wise Company? a. 108.33% b. 109.59% c. 111.05% d. 220.51% 17. Opera Corp. uses the dollar-value LIFO method of computing its inventory cost. Data for the past three years is as follows: Year ended Inventory at Price December 31. End-of-year Prices Index 2016 $650,000 1.00 2017 1,260,000 1.05 2018 1,350,250 1.10 What is the 2016 inventory balance using dollar-value LIFO? a. $650,000. b. $619,040. c. $1,227,270. d. $1,350,250. MULTIPLE CHOICE—CPA Adapted 18. How should the following costs affect a retailer's inventory valuation? Freight-in Interest on Inventory Loan a. Increase No effect b. Increase Increase c. No effect Increase d. No effect No effect 19. The following information applied to Howe, Inc. for 2017: Merchandise purchased for resale $410,000 Freight-in 8,000 Freight-out 5,000 Purchase returns 2,000 Howe's 2017 inventoriable cost was a. $410,000. b. $413,000. c. $416,000. d. $421,000. 20. The following information was derived from the 2017 accounting records of Perez Co.: Perez's Goods Perez's Central Warehouse Held by Consignees Beginning inventory $130,000 $ 14,000 Purchases 625,000 70,000 Freight-in 10,000 Transportation to consignees 5,000 Freight-out 30,000 8,000 Ending inventory 145,000 20,000 Perez's 2017 cost of sales was a. $620,000. b. $650,000. c. $684,000. d. $689,000. 21. Dole Corp.'s accounts payable at December 31, 2017, totaled $900,000 before any necessary year-end adjustments relating to the following transactions: • On December 27, 2017, Dole wrote and recorded checks to creditors totaling $350,000 causing an overdraft of $100,000 in Dole's bank account at December 31, 2017. The checks were mailed out on January 10, 2018. • On December 28, 2017, Dole purchased and received goods for $150,000, terms 2/10, n/30. Dole records purchases and accounts payable at net amounts. The invoice was recorded and paid January 3, 2018. • Goods shipped f.o.b. destination on December 20, 2017 from a vendor to Dole were received January 2, 2018. The invoice cost was $65,000. At December 31, 2017, what amount should Dole report as total accounts payable? a. $1,462,000. b. $1,397,000. c. $1,150,000. d. $1,050,000. 22. The balance in Moon Co.'s accounts payable account at December 31, 2017 was $980,000 before any necessary year-end adjustments relating to the following: • Goods were in transit to Moon from a vendor on December 31, 2017. The invoice cost was $40,000. The goods were shipped f.o.b. shipping point on December 29, 2017 and were received on January 4, 2018. • Goods shipped f.o.b. destination on December 21, 2017 from a vendor to Moon were received on January 6, 2018. The invoice cost was $25,000. • On December 27, 2017, Moon wrote and recorded checks to creditors totaling $30,000 that were mailed on January 10, 2018. In Moon's December 31, 2017 balance sheet, the accounts payable should be a. $1,010,000. b. $1,020,000. c. $1,045,000. d. $1,050,000. 23. Kerr Co.'s accounts payable balance at December 31, 2017 was $1,600,000 before considering the following transactions: • Goods were in transit from a vendor to Kerr on December 31, 2017. The invoice price was $70,000, and the goods were shipped f.o.b. shipping point on December 29, 2017. The goods were received on January 4, 2018. • Goods shipped to Kerr, f.o.b. shipping point on December 20, 2017, from a vendor were lost in transit. The invoice price was $50,000. On January 5, 2018, Kerr filed a $50,000 claim against the common carrier. In its December 31, 2017 balance sheet, Kerr should report accounts payable of a. $1,720,000. b. $1,670,000. c. $1,650,000. d. $1,600,000. 24. Walsh Retailers purchased merchandise with a list price of $150,000, subject to trade discounts of 20% and 10%, with no cash discounts allowable. Walsh should record the cost of this merchandise as a. $105,000. b. $108,000. c. $117,000. d. $150,000. 25. On June 1, 2017, Penny Corp. sold merchandise with a list price of $70,000 to Linn on account. Penny allowed trade discounts of 30% and 20%. Credit terms were 2/15, n/40 and the sale was made f.o.b. shipping point. Penny prepaid $1,000 of delivery costs for Linn as an accommodation. On June 12, 2017, Penny received from Linn a remittance in full payment amounting to a. $38,416. b. $39,788. c. $39,416. d. $39,186. 26. Groh Co. recorded the following data pertaining to raw material X during January 2017: Units Date Received Cost Issued On Hand 1/1/17 Inventory $2.00 3,200 1/11/17 Issue 1,600 1,600 1/22/17 Purchase 4,000 $2.35 5,600 The moving-average unit cost of X inventory at January 31, 2017 is a. $2.17. b. $2.21. c. $2.25. d. $2.35. 27. During periods of rising prices, a perpetual inventory system would result in the same dollar amount of ending inventory as a periodic inventory system under which of the following inventory cost flow methods? FIFO LIFO a. Yes No b. Yes Yes c. No Yes d. No No 28. Hite Co. was formed on January 2, 2017, to sell a single product. Over a two-year period, Hite's acquisition costs have increased steadily. Physical quantities held in inventory were equal to three months' sales at December 31, 2017, and zero at December 31, 2018. Assuming the periodic inventory system, the inventory cost method which reports the highest amount of each of the following is Inventory Cost of Sales December 31, 2017 2018 a. LIFO FIFO b. LIFO LIFO c. FIFO FIFO d. FIFO LIFO 29. Keck Co. had 300 units of product A on hand at January 1, 2017, costing $21 each. Purchases of product A during January were as follows: Date Units Unit Cost Jan. 10 400 $22 18 500 23 28 200 24 A physical count on January 31, 2017 shows 400 units of product A on hand. The cost of the inventory at January 31, 2017 under the LIFO method is a. $9,400. b. $8,900. c. $8,500. d. $8,200. 30. When the double-extension approach to the dollar-value LIFO inventory cost flow method is used, the inventory layer added in the current year is multiplied by an index number. How would the following be used in the calculation of this index number? Ending inventory Ending inventory at current year cost at base year cost a. Numerator Denominator b. Numerator Not used c. Denominator Numerator d. Not used Denominator 31. Farr Co. adopted the dollar-value LIFO inventory method on December 31, 2017. Farr's entire inventory constitutes a single pool. On December 31, 2017, the inventory was $960,000 under the dollar-value LIFO method. Inventory data for 2018 are as follows: 12/31/18 inventory at year-end prices $1,320,000 Relevant price index at year end (base year 2017) 110 Using dollar value LIFO, Farr's inventory at December 31, 2018 is a. $1,056,000. b. $1,224,000. c. $1,200,000. d. $1,320,000. Problem 1—Recording purchases at net amounts. Flint Co. records purchase discounts lost and uses perpetual inventories. Prepare journal entries in general journal form for the following: (a) Purchased merchandise costing $3,500 with terms 2/10, n/30. (b) Payment was made thirty days after the purchase. (a) Inventory (.98 × $3,500)....................................3,430 Accounts Payable..........................................................3,430 (b) Accounts Payable..............................................3,430 Purchase Discounts Lost.......................................70 Cash..............................................................................3,500 Problem 2—FIFO and LIFO inventory methods. During June, the following changes in inventory item 27 took place: June 1 Balance 1,400 units @ $36 14 Purchased 800 units @ $54 24 Purchased 700 units @ $45 8 Sold 400 units @ $75 10 Sold 1,000 units @ $60 29 Sold 500 units @ $66 Perpetual inventories are maintained. Instructions What is the cost of the ending inventory for item 27 under the following methods? (Show calculations.) (a) FIFO. (b) LIFO. A 700 X $ 45.00 $ 31,500.00 300 X $ 54.00 $ 16,200.00 1000.00 $ 47,700.00 B 800 X $ 54.00 $ 43,200.00 200 X $ 45.00 $ 9,000.00 1000.00 $ 52,200.00 Problem 3—FIFO and LIFO periodic inventory methods. The Rock Shop shows the following data related to an item of inventory: Inventory, January 1 300 units @ $5.00 Purchase, January 9 900 units @ $5.40 Purchase, January 19 210 units @ $6.00 Inventory, January 31 300 units Instructions (a) What value should be assigned to the ending inventory using FIFO? (b) What value should be assigned to cost of goods sold using LIFO? A 210 X $ 6.00 $ 1,260.00 90 X $ 5.40 $ 486.00 300.00 $ 1,746.00 B 210 X $ 6.00 $ 1,260.00 900 X $ 5.40 $ 4,860.00 1110.00 $ 6,120.00 Problem 4—Dollar-value LIFO method. Part A. Judd Company has a beginning inventory in year one of $1,400,000 and an ending inventory of $1,694,000. The price level has increased from 100 at the beginning of the year to 110 at the end of year one. Calculate the ending inventory under the dollar-value LIFO method. Part B. At the end of year two, Judd's inventory is $1,886,000 in terms of a price level of 115 which exists at the end of year two. Calculate the inventory at the end of year two continuing the use of the dollar-value LIFO method. Part A Computation of Ending Inventory Year One Ending Inventory at Base-Year Price Layers at Base-Year Prices X Price Index = Ending Inventory at Dollar-Value LIFO 1694000 / 1.10 = 1540000 1,400,000 X 1.00 = 1,400,000 1540000 140,000 X 1.10 = 154,000 1,554,000 Part B Computation of Ending Inventory Year One Ending Inventory at Base-Year Price Layers at Base-Year Prices X Price Index = Ending Inventory at Dollar-Value LIFO 1886000 / 1.15 = 1640000 1,400,000 X 1.00 = 1,400,000 1640000 140,000 X 1.10 = 154,000 100,000 X 1.15 = 115,000 1,669,000 [Show More]

Last updated: 1 year ago

Preview 1 out of 39 pages

Instant download

Buy this document to get the full access instantly

Instant Download Access after purchase

Add to cartInstant download

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Nov 21, 2020

Number of pages

39

Written in

Additional information

This document has been written for:

Uploaded

Nov 21, 2020

Downloads

0

Views

126

ans.png)

.png)

.png)

(1) answers.png)

answers.png)