Accounting > Solutions Guide > CHAPTER 22 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, AND MULTINATIONAL CONSIDERATIONS: ANSWERS (All)

CHAPTER 22 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, AND MULTINATIONAL CONSIDERATIONS: ANSWERS

Document Content and Description Below

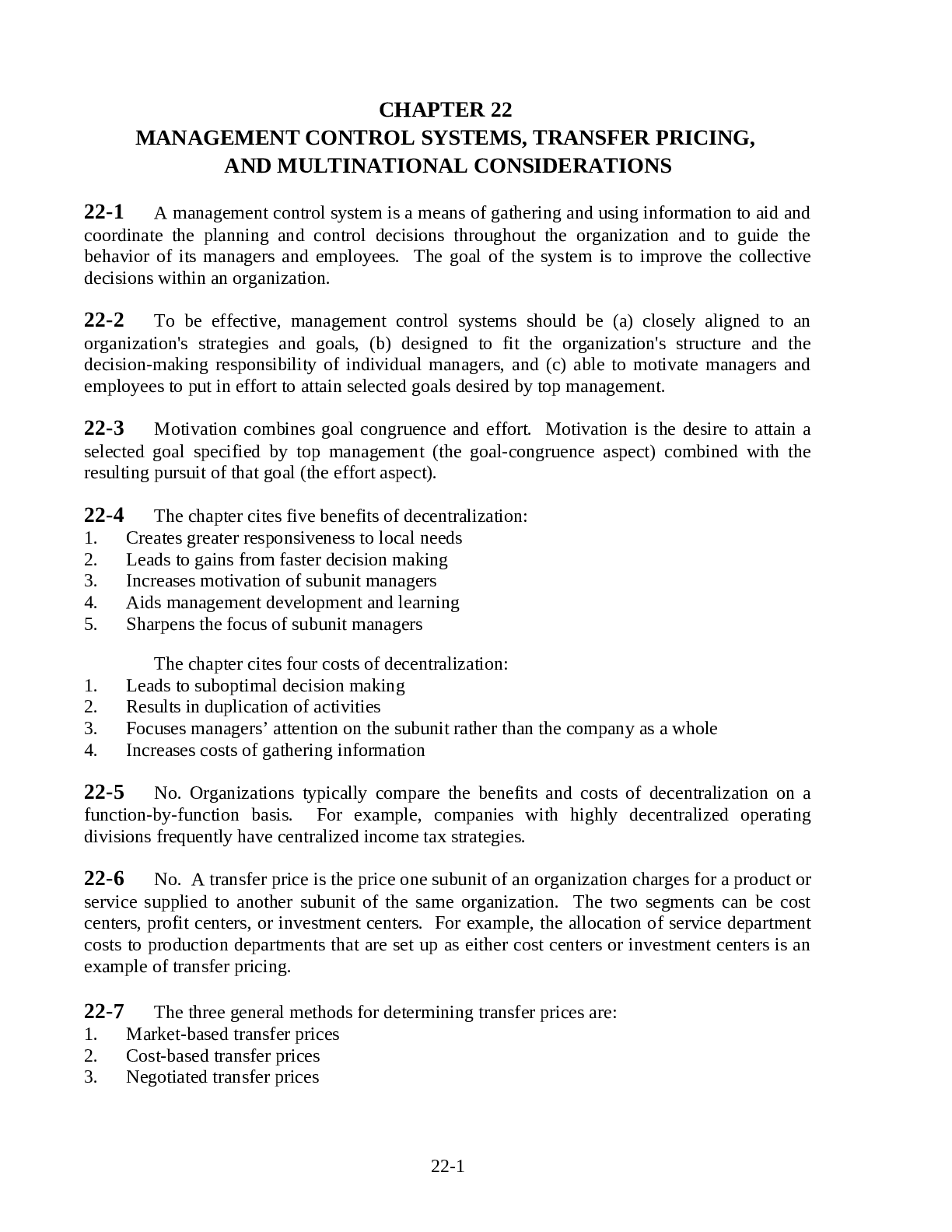

22-1 A management control system is a means of gathering and using information to aid and coordinate the planning and control decisions throughout the organization and to guide the behavior of its m... anagers and employees. The goal of the system is to improve the collective decisions within an organization. 22-2 To be effective, management control systems should be (a) closely aligned to an organization's strategies and goals, (b) designed to fit the organization's structure and the decision-making responsibility of individual managers, and (c) able to motivate managers and employees to put in effort to attain selected goals desired by top management. 22-3 Motivation combines goal congruence and effort. Motivation is the desire to attain a selected goal specified by top management (the goal-congruence aspect) combined with the resulting pursuit of that goal (the effort aspect). 22-4 The chapter cites five benefits of decentralization: 1. Creates greater responsiveness to local needs 2. Leads to gains from faster decision making 3. Increases motivation of subunit managers 4. Aids management development and learning 5. Sharpens the focus of subunit managers The chapter cites four costs of decentralization: 1. Leads to suboptimal decision making 2. Results in duplication of activities 3. Focuses managers’ attention on the subunit rather than the company as a whole 4. Increases costs of gathering information 22-5 No. Organizations typically compare the benefits and costs of decentralization on a function-by-function basis. For example, companies with highly decentralized operating divisions frequently have centralized income tax strategies. 22-6 No. A transfer price is the price one subunit of an organization charges for a product or service supplied to another subunit of the same organization. The two segments can be cost centers, profit centers, or investment centers. For example, the allocation of service department costs to production departments that are set up as either cost centers or investment centers is an example of transfer pricing. 22-7 The three general methods for determining transfer prices are: 1. Market-based transfer prices 2. Cost-based transfer prices 3. Negotiated transfer prices [Show More]

Last updated: 1 year ago

Preview 1 out of 48 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jun 25, 2021

Number of pages

48

Written in

Additional information

This document has been written for:

Uploaded

Jun 25, 2021

Downloads

0

Views

64

.png)