Economics > QUESTIONS & ANSWERS > DeVry University, Keller Graduate School of Management - BUSN 278FINALS6. Graded A (All)

DeVry University, Keller Graduate School of Management - BUSN 278FINALS6. Graded A

Document Content and Description Below

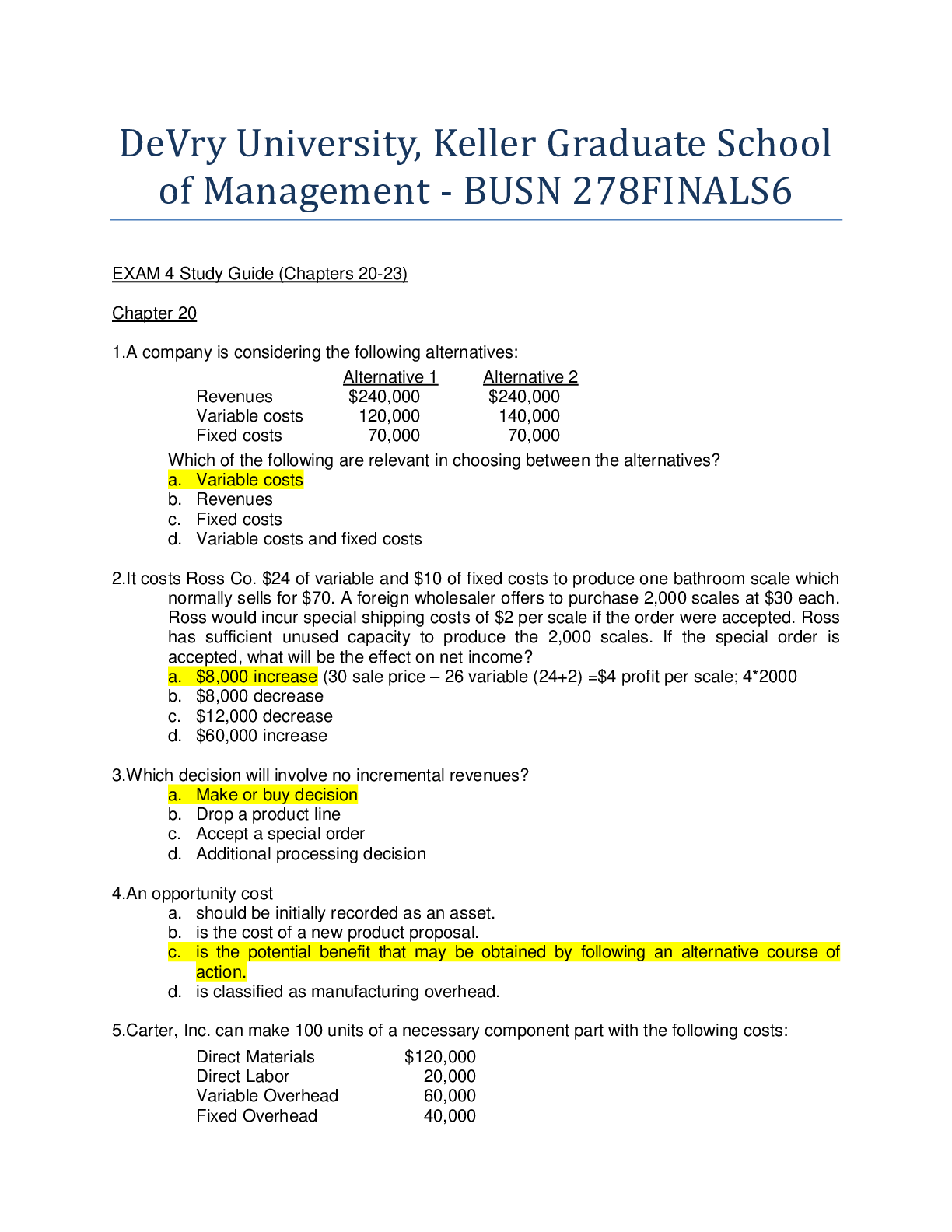

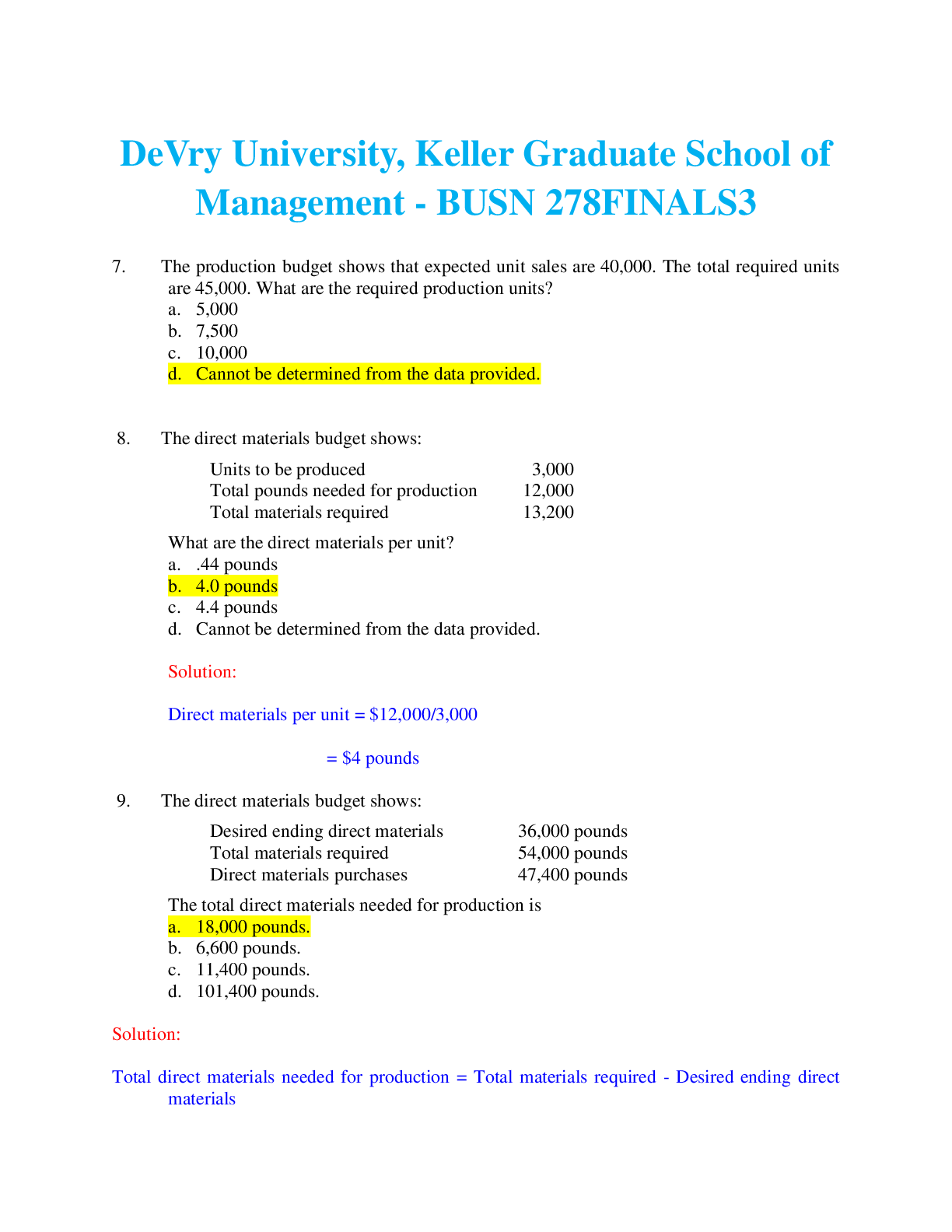

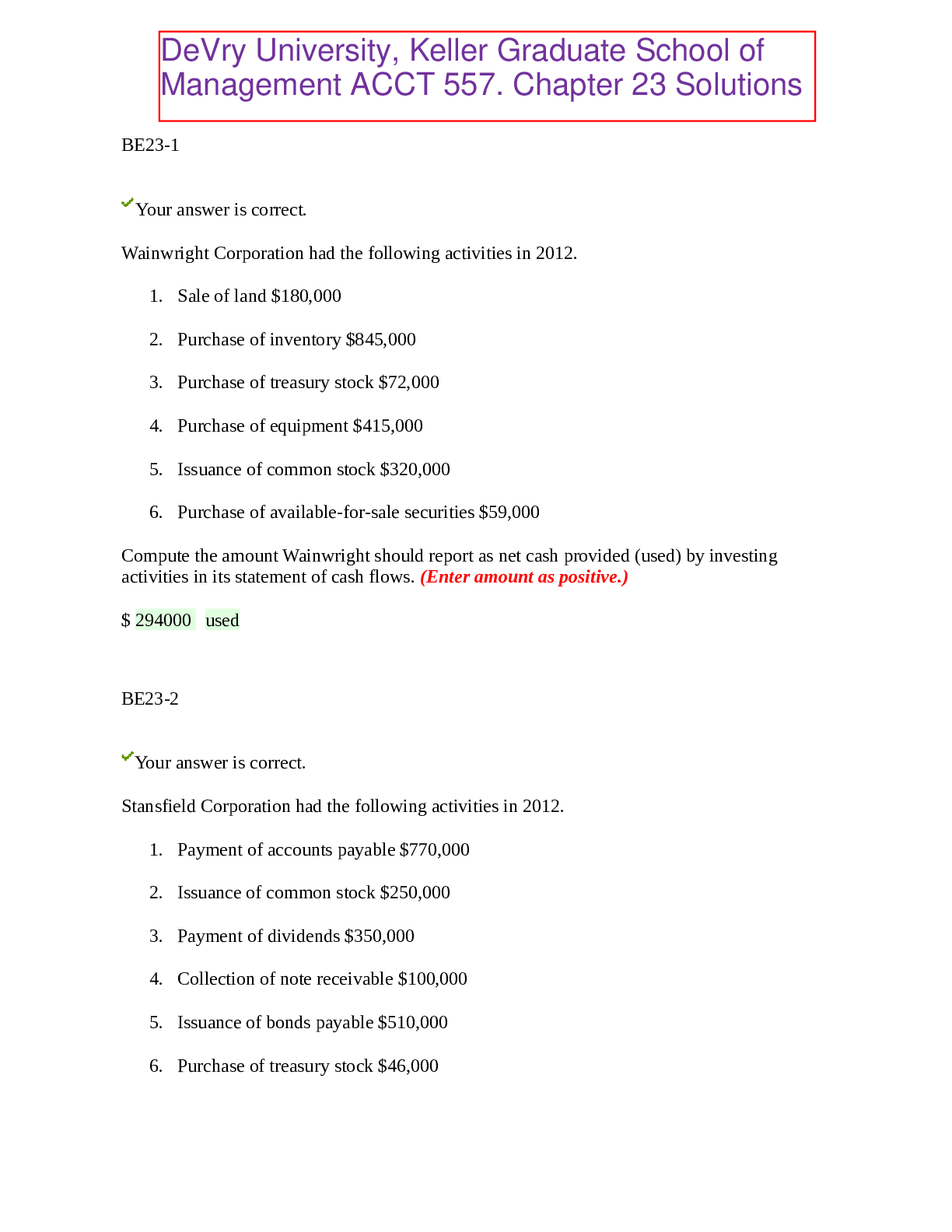

DeVry University, Keller Graduate School of Management - BUSN 278FINALS6 EXAM 4 Study Guide (Chapters 20-23) Chapter 20 1. A company is considering the following alternatives: Alternative 1... Alternative 2 Revenues $240,000 $240,000 Variable costs 120,000 140,000 Fixed costs 70,000 70,000 Which of the following are relevant in choosing between the alternatives? a. Variable costs b. Revenues c. Fixed costs d. Variable costs and fixed costs 2. It costs Ross Co. $24 of variable and $10 of fixed costs to produce one bathroom scale which normally sells for $70. A foreign wholesaler offers to purchase 2,000 scales at $30 each. Ross would incur special shipping costs of $2 per scale if the order were accepted. Ross has sufficient unused capacity to produce the 2,000 scales. If the special order is accepted, what will be the effect on net income? a. $8,000 increase (30 sale price – 26 variable (24+2) =$4 profit per scale; 4*2000 b. $8,000 decrease c. $12,000 decrease d. $60,000 increase 3. Which decision will involve no incremental revenues? a. Make or buy decision b. Drop a product line c. Accept a special order d. Additional processing decision 4. An opportunity cost a. should be initially recorded as an asset. b. is the cost of a new product proposal. c. is the potential benefit that may be obtained by following an alternative course of action. d. is classified as manufacturing overhead. 5. Carter, Inc. can make 100 units of a necessary component part with the following costs: Direct Materials $120,000 Direct Labor 20,000 Variable Overhead 60,000 Fixed Overhead 40,000 If Carter can purchase the component externally for $220,000 and only $10,000 of the fixed costs can be avoided, what is the correct make-or-buy decision? a. Make and save $10,000 (120k+20k+60k+40k=240k make;220k+30k fixed=250k buy b. Buy and save $10,000 c. Make and save $30,000 d. Buy and save $30,000 6. Corny produces corn chips. The cost of one batch is below: Direct materials $36.00 Direct labor 26.00 Variable overhead 22.00 Fixed overhead 28.00 An outside supplier has offered to produce the corn chips for $50 per batch. How much will Corny save if it accepts the offer? a. $4.00 per batch b. $34.00 per batch (36+26+22=84 make; 84 make – 50 buy =34 savings c. $62.00 per batch d. $12.00 per batch 7. Mink Manufacturing is unsure of whether to sell its product assembled or unassembled. The unit cost of the unassembled product is $60 and Mink would sell it for $130. The cost to assemble the product is estimated at $42 per unit and the company believes the market would support a price of $170 on the assembled unit. What decision should Mink make? a. Sell before assembly, the company will be better off by $2 per unit. b. Sell before assembly, the company will be better off by $40 per unit. c. Process further, the company will be better off by $58 per unit. d. Process further, the company will be better off by $28 per unit. (130-60=70 unassembled; 60+42=102 cost to assemble; 170-102=68 assem; 70-68=2) 8. Maynard, Inc. has old inventory on hand that cost $24,000. Its scrap value is $32,000. The inventory could be sold for $80,000 if manufactured further at an additional cost of $24,000. What should Maynard do? a. Sell the inventory for $32,000 scrap value b. Dispose of the inventory to avoid any further decline in value c. Hold the inventory at its $24,000 cost d. Manufacture further and sell it for $80,000 (32k-24k=8k as is; 24k+24k=48k cost to manufacture further; 80k-48k=32k profit for further manufacturing; 32k>8k 9. Walk Manufacturing gathered the following data about the three products that it produces: Present Estimated Additional Estimated Sales Product Sales Value Processing Costs if Processed Further A $24,000 $16,000 $42,000 B 28,000 10,000 36,000 C 22,000 6,000 32,000 Which of the products should not be processed further? a. Product A b. Product B (cost = 28k+10k = 38k cost; sales = 36k; cost > sale price c. Product C d. Products A and C 10. Justin Industries produces three versions of tires: Supreme, Advanced, and Basic. A condensed segmented income statement for a recent period follows: Supreme Advanced Basic Total Sales $1,000,000 $400,000 $130,000 $1,530,000 Variable expenses 650,000 280,000 116,000 1,046,000 Contribution margin 350,000 120,000 14,000 484,000 Fixed expenses 150,000 70,000 44,000 264,000 Net income (loss) $200,000 $ 50,000 $(30,000) $220,000 Assume none of the fixed expenses for the Basic line are avoidable. What will be total net income if the line is dropped? a. $250,000 b. $206,000 (the 14k CM will be lost, reducing net income by 14k; 220k-14k=206k) c. $210,000 d. $280,000 11. Tex's Manufacturing Company can make 100 units of a necessary component part with the following costs: Direct Materials $120,000 Direct Labor 25,000 Variable Overhead 45,000 Fixed Overhead 30,000 If Tex's Manufacturing Company can purchase the component externally for $190,000 and only $5,000 of the fixed costs can be avoided, what is the correct make-or-buy decision? a. Buy and save $5,000 (Make – 120k+25k+45k+30k=220k; Buy-190k+25k=215k) b. Make and save $5,000 c. Make and save $15,000 d. Buy and save $15,000 12. A cost that cannot be changed by any present or future decision is a(n) a. incremental cost. b opportunity cost. c. sunk cost. d. variable cost. 13. Clemente Inc. incurs the following costs to produce 10,000 units of a subcomponent: Direct materials $8,400 Direct labor 11,250 Variable overhead 12,600 Fixed overhead 16,200 An outside supplier has offered to sell Clemente the subcomponent for $2.85 a unit. If Clemente accepts the offer, by how much will net income increase (decrease)? a. $3,750 (8400+11250+12600=32250; 10000*2.85=28500; 32250-28500=3750) b. $19,950 c. $(8,850) d. $(2,850) 14. Incremental analysis would be appropriate for a. acceptance of an order at a special price. b. a retain or replace equipment decision. c. a sell or process further decision. d. all of these. 15. In incremental analysis, a. costs are not relevant if they change between alternatives. b. all costs are relevant if they change between alternatives. c. only fixed costs are relevant. d. only variable costs are relevant. 16. Cyprus Corp. has excess capacity. Under what situations should the company accept a special order for less than the current selling price? a. Never b. When additional fixed costs must be incurred to accommodate the order c. When the company thinks it can use the cheaper materials without the customer's knowledge d. When incremental revenues exceed incremental costs 17. Allan Co. can produce 100 units of a component part with the following costs: Direct Materials $60,000 Direct Labor 26,000 Variable Overhead 64,000 Fixed Overhead 44,000 If Allan Co. can purchase the units externally for $160,000, by what amount will its total costs change? a. An increase of $160,000 b. An increase of $10,000 (60k+26k+64k=150k to produce; 160k buy > 150k produce c. An increase of $34,000 d. A decrease of $44,000 Chapter 21 1. The production budget shows expected unit sales of 32,000. Beginning finished goods units are 5,600. Required production units are 33,600. What are the desired ending finished goods units? a. 4,000 b. 5,600 c. 6,400 d. 7,200 (5,600+33,600-32,000=x, x=7,200) 2.Doe Manufacturing plans to sell 4,000 purple lawn chairs during May, 3,800 in June, and 4,000 during July. The company keeps 15% of the next month’s sales as ending inventory. How many units should Doe produce during June? a. 3,830 (3,800*.15=570 beg June; 4000*.15=600 end June; 570+x-3800=600, x=3830) b. 4,400 c. 3,770 d. Not enough information to determine. 3. Kam Department Store reported the following information for 2012: October November December Budgeted sales $930,000 $870,000 $1,080,000 • All sales are on credit. • Customer amounts on account are collected 50% in the month of sale and 50% in the following month. How much cash will Kam receive in November? a. $435,000 b. $975,000 c. $900,000 (930,000/2=465,000; 870,000/2=435,000; 465,000+435,000=900,000) d. $870,000 4. The following information was taken from Southgate Industry’s cash budget for the month of July: Beginning cash balance $300,000 Cash receipts 190,000 Cash disbursements 340,000 If the company has a policy of maintaining a minimum end of the month cash balance of $250,000, the amount the company would have to borrow is a. $100,000. (300,000+190,000-340,000=150,000; 250k-150k=100k) b. $50,000. c. $150,000. d. $60,000. 5. Why are budgets useful in the planning process? a. They provide management with information about the company's past performance. b. They help communicate goals and provide a basis for evaluation. c. They guarantee the company will be profitable if it meets its objectives. d. They enable the budget committee to earn their paycheck. 6. The most common budget period is a. one month. b. three months. c. six months. d. one year. 7. The direct materials budget details 1. the quantity of direct materials to be purchased. 2. the cost of direct materials to be purchased. a. 1 b. 2 c. both 1 and 2 d. neither 1 nor 2 8. On January 1, Kale Company has a beginning cash balance of $42,000. During the year, the company expects cash disbursements of $340,000 and cash receipts of $290,000. If Kale requires an ending cash balance of $40,000, the company must borrow a. $32,000. b. $40,000. c. $48,000. (42000+290000-340000=(8000); 40000+8000=48000) d. $92,000. 9. The production budget shows expected unit sales are 100,000. The required production units are 104,000. What are the beginning and desired ending finished goods units, respectively? Beginning Units Ending Units a. 10,000 6,000 b. 6,000 10,000 (Make 104,000, Sell 100,000 = 4,000 Increase) c. 4,000 10,000 d. 10,000 4,000 10. Pell Manufacturing is preparing its direct labor budget for May. Projections for the month are that 33,400 units are to be produced and that direct labor time is three hours per unit. If the labor cost per hour is $12, what is the total budgeted direct labor cost for May? a. $1,159,200. b. $1,180,800. c. $1,202,400. (33,400*3*12) d. $1,296,000. 11. The budget that is often considered to be the most important financial budget is the a. cash budget. b. capital expenditure budget. c. budgeted income statement. d. budgeted balance sheet. 12. Beginning cash balance plus total receipts a. equals ending cash balance. b. must equal total disbursements. c. equals total available cash. d. is the excess of available cash over disbursements. 13. The projection of financial position at the end of the budget period is found on the a. budgeted income statement. b. cash budget. c. budgeted balance sheet. d. sales budget. 14. The starting point in preparing a master budget is the preparation of the a. production budget. b. sales budget. c. purchasing budget. d. personnel budget. 15. A master budget consists of a. an interrelated long-term plan and operating budgets. b. financial budgets and a long-term plan. c. interrelated financial budgets and operating budgets. d. all the accounting journals and ledgers used by a company. Chapter 22 1. A major element in budgetary control is a. the preparation of long-term plans. b. the comparison of actual results with planned objectives. c. the valuation of inventories. d. approval of the budget by the stockholders. 2. If costs are not responsive to changes in activity level, then these costs can be best described as a. mixed. b. flexible. c. variable. d. fixed. 3. A flexible budget a. is prepared when management cannot agree on objectives for the company. b. projects budget data for various levels of activity. c. is only useful in controlling fixed costs. d. cannot be used for evaluation purposes because budgeted data are adjusted to reflect actual results. 4. What is the primary difference between a static budget and a flexible budget? a. The static budget contains only fixed costs, while the flexible budget contains only variable costs. b. The static budget is prepared for a single level of activity, while a flexible budget is adjusted for different activity levels. c. The static budget is constructed using input from only upper level management, while a flexible budget obtains input from all levels of management. d. The static budget is prepared only for units produced, while a flexible budget reflects the number of units sold. 5. Which one of the following would be the same total amount on a flexible budget and a static budget if the activity level is different for the two types of budgets? a. Direct materials cost b. Direct labor cost c. Variable manufacturing overhead d. Fixed manufacturing overhead 6. Best Shingle's budgeted manufacturing costs for 25,000 squares of shingles are: Fixed manufacturing costs $12,000 Variable manufacturing costs $16.00 per square Best produced 20,000 squares of shingles during March. How much are budgeted total manufacturing costs in March? a. $320,000 b. $412,000 c. $400,000 d. $332,000 (20000*$16=320,000 variable; 320,000+12,000=332,000) 7. At 9,000 direct labor hours, the flexible budget for indirect materials is $18,000. If $18,700 are incurred at 9,200 direct labor hours, the flexible budget report should show the following difference for indirect materials: a. $700 unfavorable. b. $700 favorable. c. $300 favorable. d. $300 unfavorable. (18000/9000=2; 2*9200=18400; 18700-18400=300 U) 8.Nikoto Steel Co. budgeted manufacturing costs for 50,000 tons of steel are: Fixed manufacturing costs $50,000 per month Variable manufacturing costs $12.00 per ton of steel Nikoto produced 40,000 tons of steel during March. How much is the flexible budget for total manufacturing costs for March? a. $520,000 b. $650,000 c. $480,000 d. $530,000 (40000*12=480000; 480000+50000=530000) 9. Stone Industries uses flexible budgets. At normal capacity of 8,000 units, budgeted manufacturing overhead is: $64,000 variable and $180,000 fixed. If Stone had actual overhead costs of $250,000 for 9,000 units produced, what is the difference between actual and budgeted costs? a. $2,000 unfavorable b. $2,000 favorable (64k/8k=8; 9k*8=72,000; 72k+180k=252,000; 250k-252k=2,000F) c. $6,000 unfavorable d. $8,000 favorable 10. If a company plans to sell 24,000 units of product but sells 30,000, the most appropriate comparison of the cost data associated with the sales will be by a budget based on a. the original planned level of activity. b. 27,000 units of activity. c. 30,000 units of activity. d. 24,000 units of activity. 11. At 18,000 direct labor hours, the flexible budget for indirect materials is $36,000. If $37,400 are incurred at 18,400 direct labor hours, the flexible budget report should show the following difference for indirect materials: a. $1,400 unfavorable. b. $1,400 favorable. c. $600 favorable. d. $600 unfavorable. (36000/18000=2; 2*18400=36800; 37400-36800=600U) 12. A department has budgeted monthly manufacturing overhead cost of $540,000 plus $3 per direct labor hour. If a flexible budget report reflects $1,044,000 for total budgeted manufacturing cost for the month, the actual level of activity achieved during the month was a. 528,000 direct labor hours. b. 168,000 direct labor hours. (1044000-540000=504000; 504000/3=168000) c. 348,000 direct labor hours. d. Cannot be determined from the information provided. Chapter 23 1. The difference between a budget and a standard is that a. a budget expresses what costs were, while a standard expresses what costs should be. b. a budget expresses management's plans, while a standard reflects what actually happened. c. a budget expresses a total amount, while a standard expresses a unit amount. d. standards are excluded from the cost accounting system, whereas budgets are generally incorporated into the cost accounting system. 2. An unfavorable materials quantity variance would occur if a. more materials were purchased than were used. b. actual pounds of materials used were less than the standard pounds allowed. c. actual labor hours used were greater than the standard labor hours allowed. d. actual pounds of materials used were greater than the standard pounds allowed. 3. Hofburg’s standard quantities for 1 unit of product include 2 pounds of materials and 1.5 labor hours. The standard rates are $4 per pound and $14 per hour. The standard overhead rate is $16 per direct labor hour. The total standard cost of Hofburg’s product is a. $29. b. $34. c. $45. d. $53. (2*4=$8 materials; 1.5*14=$21 labor; 1.5*16=$24 OH; 8+21+24=53) 4. A company developed the following per-unit standards for its product: 2 pounds of direct materials at $4 per pound. Last month, 1,000 pounds of direct materials were purchased for $3,800. The direct materials price variance for last month was a. $3,800 favorable. b. $200 favorable. (4*1,000=4,000 standard; 4,000 standard – 3,800 actual=200F) c. $100 favorable. d. $200 unfavorable. 5. The per-unit standards for direct labor are 2 direct labor hours at $12 per hour. If in producing 1,200 units, the actual direct labor cost was $25,600 for 2,000 direct labor hours worked, the total direct labor variance is a. $960 unfavorable. b. $3,200 favorable. (24*1,200=28,800; 28,800 standard-25,600 actual=3,200F) c. $2,000 unfavorable. d. $3,200 unfavorable. 6. Edgar, Inc. has a materials price standard of $2.00 per pound. Three thousand pounds of materials were purchased at $2.20 a pound. The actual quantity of materials used was 3,000 pounds, although the standard quantity allowed for the output was 2,700 pounds. Edgar, Inc.'s materials price variance is a. $60 U. b. $600 U. (AQ*AP-AQ*SP) (3000*2.2=6600)-(3000*2=6000); 6600-6000=600U c. $540 U. d. $600 F. 7. Monster Company produces a product requiring 3 direct labor hours at $20.00 per hour. During January, 2,000 products are produced using 6,300 direct labor hours. Monster’s actual payroll during January was $122,850. What is the labor quantity variance? a. $2,850 U b. $6,000 F c. $3,150 F d. $6,000 U (AQ*SP-SQ*SP) (6300*20=126k)-(6000*20=120k); 126k-120k=6,000U 8. Scorpion Production Company planned to use 1 yard of plastic per unit budgeted at $81 a yard. However, the plastic actually cost $80 per yard. The company actually made 1,300 units, although it had planned to make only 1,100 units. Total yards used for production were 1,320. How much is the total materials variance? a. $16,200 U b. $1,620 U c. $1,320 F d. $300 U (AQ*AP)-(SQ*SP) (1320*80)-(1300*81); 105,600-105,300=300U 9. If actual costs are greater than standard costs, there is a(n) a. normal variance. b. unfavorable variance. c. favorable variance. d. error in the accounting system. 10. A company developed the following per-unit standards for its product: 2 pounds of direct materials at $4 per pound. Last month, 1,000 pounds of direct materials were purchased for $3,800. The direct materials price variance for last month was a. $3,800 favorable. b. $200 favorable. (AQ*AP-AQ*SP) (1,000*3.8)-(1,000*4); 3800-4000=200F c. $100 favorable. d. $200 unfavorable. 11.The per-unit standards for direct materials are 2 gallons at $4 per gallon. Last month, 5,600 gallons of direct materials that actually cost $21,200 were used to produce 3,000 units of product. The direct materials quantity variance for last month was a. $1,600 favorable. (AQ*SP-SQ*SP) (5600*4)-(6000*4); 22400-24000=1600F b. $1,200 favorable. c. $1,600 unfavorable. d. $2,800 unfavorable. 12. The standard rate of pay is $10 per direct labor hour. If the actual direct labor payroll was $58,800 for 6,000 direct labor hours worked, the direct labor price (rate) variance is a. $1,200 unfavorable. b. $1,200 favorable. (AQ*AP)-(SQ*SP) (6000*9.8)-(6000*10); 58800-60000=1200F c. $1,500 unfavorable. d. $1,500 favorable. 13. The formula for the materials price variance is a. (AQ × SP) – (SQ × SP). b. (AQ × AP) – (AQ × SP). c. (AQ × AP) – (SQ × SP). d. (AQ × SP) – (SQ × AP). 14. The formula for the materials quantity variance is a. (SQ × AP) – (SQ × SP). b. (AQ × AP) – (AQ × SP). c. (AQ × SP) – (SQ × SP). d. (AQ × AP) – (SQ × SP). 15. The formula for the labor price variance is a. (AH) x (SR) less (SH) x (SR). b. (AH) x (AR) less (AH) x (SR). c. (AH) x (AR) less (SH) x (SR). d. (AH) x (SR) less (AH) x (SR). 16. Dillon has a standard of 2 hours of labor per unit, at $18 per hour. In producing 2,000 units, Dillon used 3,850 hours of labor at a total cost of $70,455. Dillon's labor quantity variance is a. $1,155 U. b. $1,555 F. c. $2,700 F. (AH*SR)-(SH*SR) (3850*18)-(4000*18); 69300-72000=2700F d. $2,895 F. 17. Dillon has a standard of 2 hours of labor per unit, at $18 per hour. In producing 2,000 units, Dillon used 3,850 hours of labor at a total cost of $70,455. Dillon's total labor variance is a. $1,155 U. b. $1,200 U. c. $1,555 F. (AH*AR)-(SH*SR) (3850*18.3)-(4000*18); 70455-72000=1555F d. $2,895 F. 18. Dillon has a standard of 2 hours of labor per unit, at $18 per hour. In producing 2,000 units, Dillon used 3,850 hours of labor at a total cost of $70,455. Dillon's labor price variance is a. $1,155 U. (AH*AR)-(AH*SR) (3850*18.3)-(3850*18); 70455-69300=1155U b. $1,200 U. c. $1,555 F. d. $2,895 F. [Show More]

Last updated: 1 year ago

Preview 1 out of 11 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

May 18, 2020

Number of pages

11

Written in

Additional information

This document has been written for:

Uploaded

May 18, 2020

Downloads

0

Views

62

.png)

.png)

.png)

.png)