Financial Accounting > QUESTIONS & ANSWERS > SUNY Buffalo State College MGA 314 CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION (All)

SUNY Buffalo State College MGA 314 CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION

Document Content and Description Below

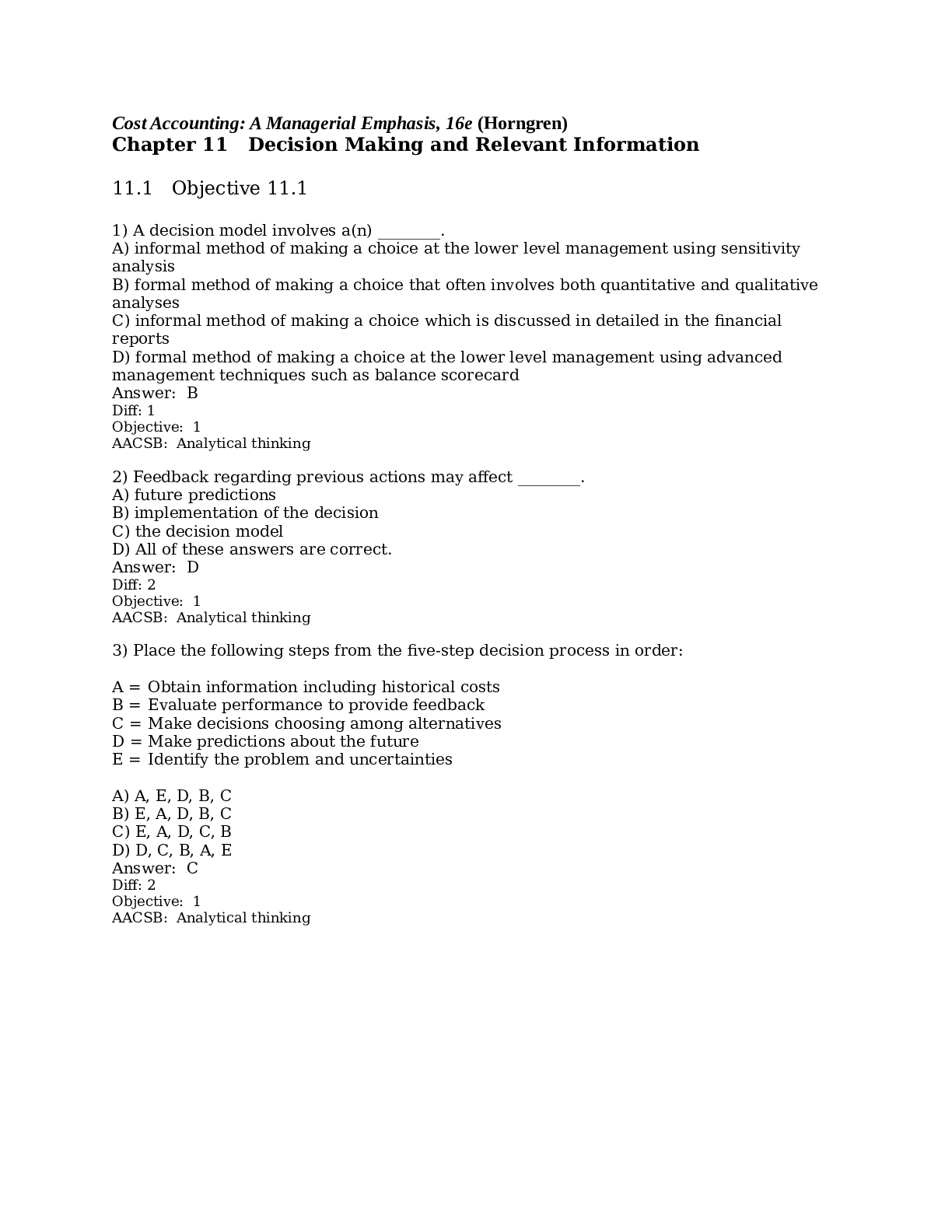

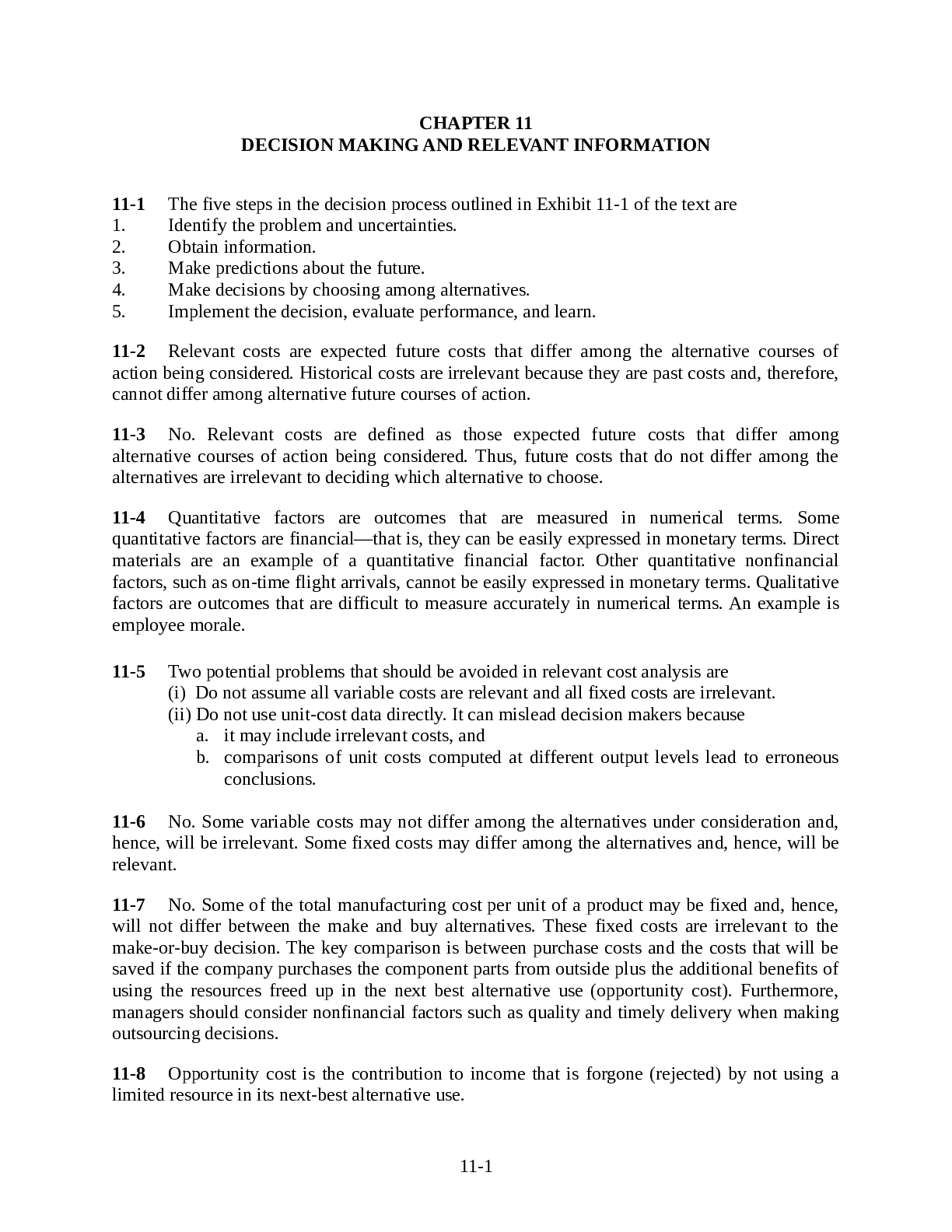

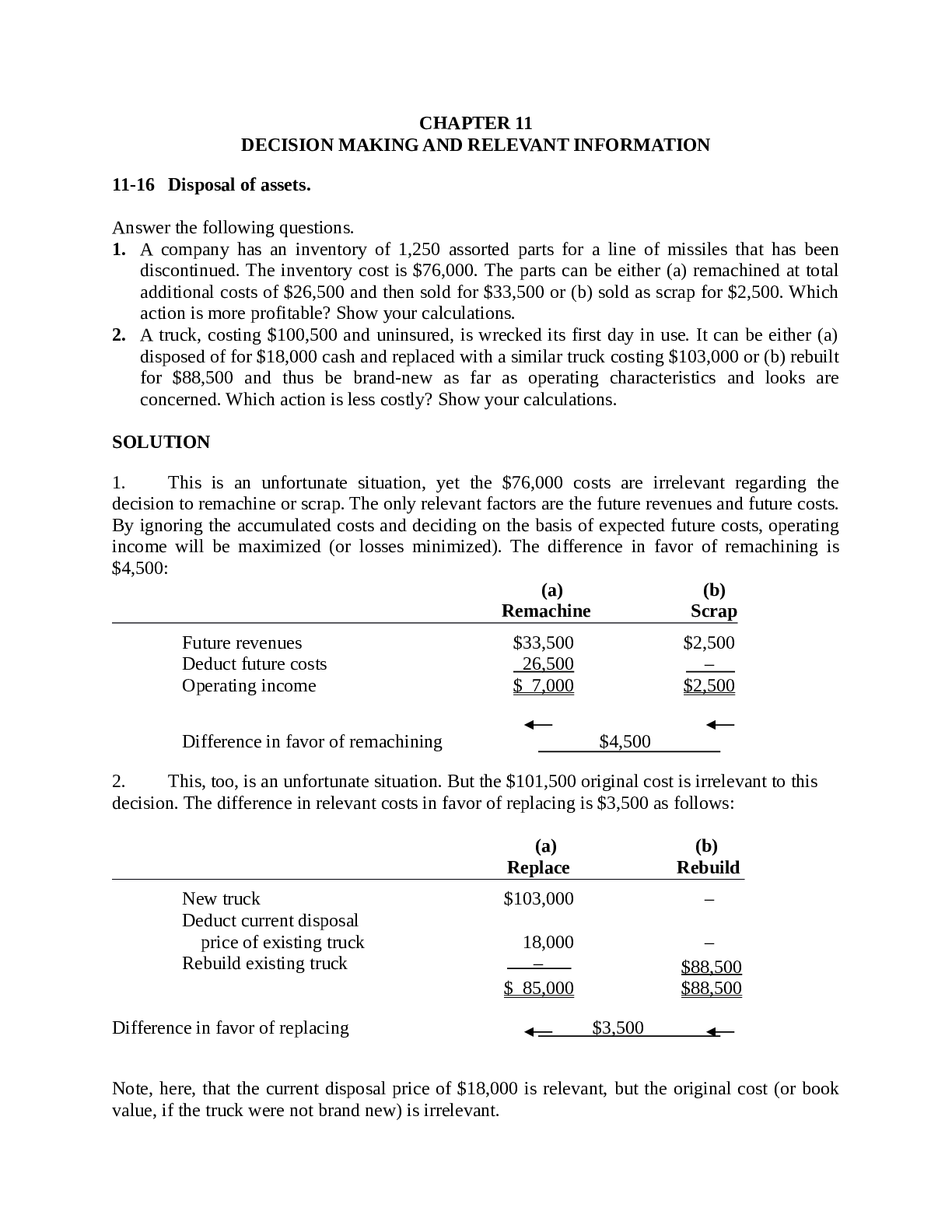

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 11-1 The five steps in the decision process outlined in Exhibit 11-1 of the text are 1. Identify the problem and uncertainties. 2. Obtain inform... ation. 3. Make predictions about the future. 4. Make decisions by choosing among alternatives. 5. Implement the decision, evaluate performance, and learn. 11-2 Relevant costs are expected future costs that differ among the alternative courses of action being considered. Historical costs are irrelevant because they are past costs and, therefore, cannot differ among alternative future courses of action. 11-3 No. Relevant costs are defined as those expected future costs that differ among alternative courses of action being considered. Thus, future costs that do not differ among the alternatives are irrelevant to deciding which alternative to choose. 11-4 Quantitative factors are outcomes that are measured in numerical terms. Some quantitative factors are financial––that is, they can be easily expressed in monetary terms. Direct materials are an example of a quantitative financial factor. Other quantitative nonfinancial factors, such as on-time flight arrivals, cannot be easily expressed in monetary terms. Qualitative factors are outcomes that are difficult to measure accurately in numerical terms. An example is employee morale. 11-5 Two potential problems that should be avoided in relevant cost analysis are (i) Do not assume all variable costs are relevant and all fixed costs are irrelevant. (ii) Do not use unit-cost data directly. It can mislead decision makers because a. it may include irrelevant costs, and b. comparisons of unit costs computed at different output levels lead to erroneous conclusions. 11-6 No. Some variable costs may not differ among the alternatives under consideration and, hence, will be irrelevant. Some fixed costs may differ among the alternatives and, hence, will be relevant. 11-7 No. Some of the total manufacturing cost per unit of a product may be fixed and, hence, will not differ between the make and buy alternatives. These fixed costs are irrelevant to the make-or-buy decision. The key comparison is between purchase costs and the costs that will be saved if the company purchases the component parts from outside plus the additional benefits of using the resources freed up in the next best alternative use (opportunity cost). Furthermore, managers should consider nonfinancial factors such as quality and timely delivery when making outsourcing decisions. 11-8 Opportunity cost is the contribution to income that is forgone (rejected) by not using a limited resource in its next-best alternative use. 11-111-9 No. When deciding on the quantity of inventory to buy, managers must consider both the purchase cost per unit and the opportunity cost of funds invested in the inventory. For example, the purchase cost per unit may be low when the quantity of inventory purchased is large, but the benefit of the lower cost may be more than offset by the high opportunity cost of the funds invested in acquiring and holding inventory. 11-10 No. Managers should aim to get the highest contribution margin per unit of the constraining (that is, scarce, limiting, or critical) factor. The constraining factor is what restricts or limits the production or sale of a given product (for example, availability of machine-hours). 11-11 No. For example, if the revenues that will be lost exceed the costs that will be saved, the branch or business segment should not be shut down. Shutting down will only increase the loss. Allocated costs and fixed costs that will not be saved are irrelevant to the shut-down decision. 11-12 Cost written off as depreciation is irrelevant when it pertains to a past cost such as equipment already purchased. But the purchase cost of ne [Show More]

Last updated: 1 year ago

Preview 1 out of 43 pages

Instant download

Buy this document to get the full access instantly

Instant Download Access after purchase

Add to cartInstant download

Also available in bundle (2)

Cost Accounting: A Managerial Emphasis, 16e (Horngren) QUESTIONS AND ANSWERS-A COMPREHENSIVE COLLECTION CO,PLETE FOR EXAM PREPARATION- GRADED A+

Cost Accounting: A Managerial Emphasis, 16e (Horngren) QUESTIONS AND ANSWERS-A COMPREHENSIVE COLLECTION CO,PLETE FOR EXAM PREPARATION- GRADED A+

By d.occ 2 years ago

$53

13

ACCOUNTING QUESTIONS, SOLUTIONS & EXPLANATIONS-VERIFIED BY EXPERTS-A COMPLETE GUIDE FOR EAXAM PREPARATION-GRADED A+

ACCOUNTING QUESTIONS, SOLUTIONS & EXPLANATIONS-VERIFIED BY EXPERTS-A COMPLETE GUIDE FOR EAXAM PREPARATION-GRADED A+

By d.occ 2 years ago

$45

8

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jul 09, 2021

Number of pages

43

Written in

Additional information

This document has been written for:

Uploaded

Jul 09, 2021

Downloads

0

Views

76

.png)

.png)

Med Surg test Questions and Answers with Explanations, 100% Correct, Download to Score A.png)

.png)