Finance > QUESTIONS & ANSWERS > Questions and Answers: Chapter 9--Inventory and Cost of Goods Sold. (All)

Questions and Answers: Chapter 9--Inventory and Cost of Goods Sold.

Document Content and Description Below

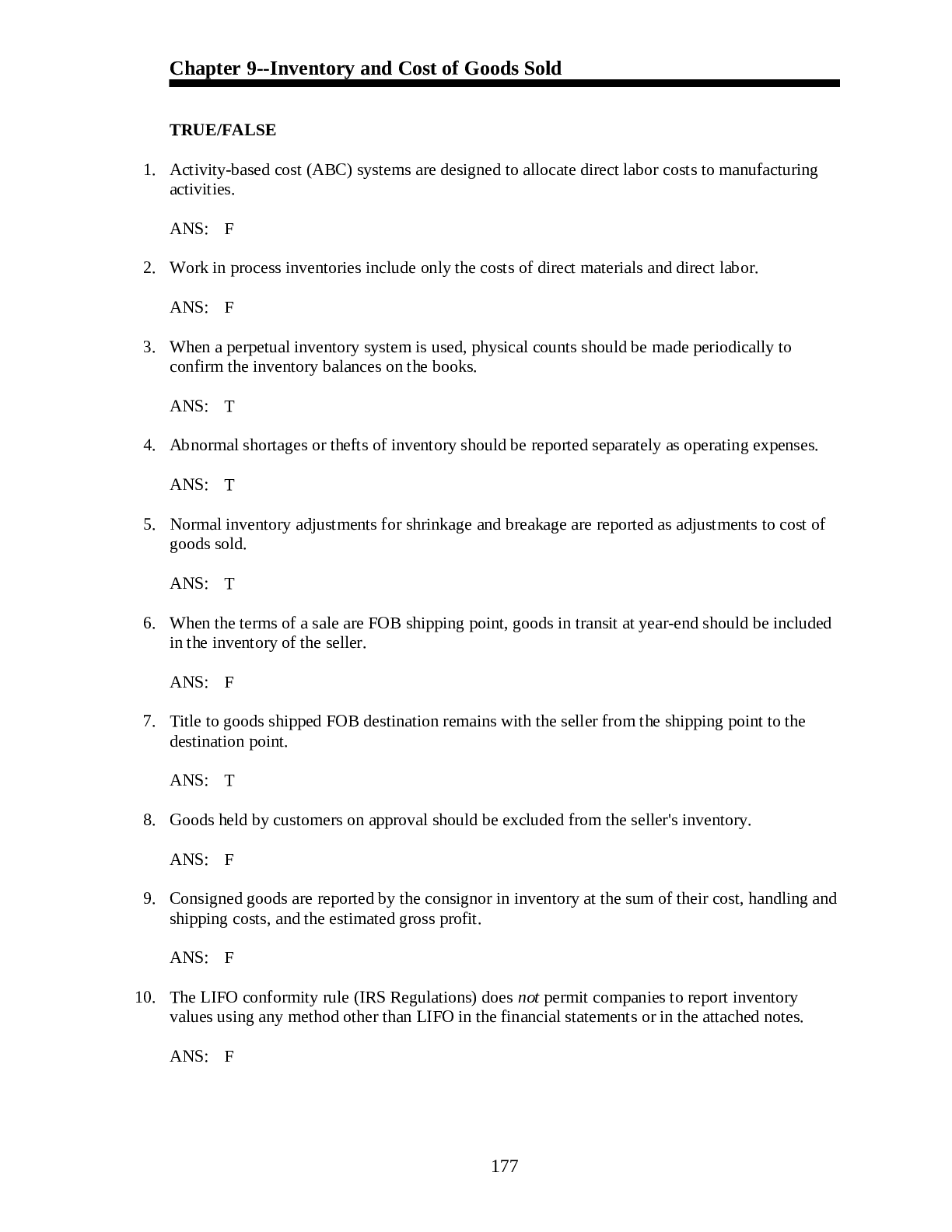

Chapter 9--Inventory and Cost of Goods Sold TRUE/FALSE 1. Activity-based cost (ABC) systems are designed to allocate direct labor costs to manufacturing activities. 2. Work in process invento... ries include only the costs of direct materials and direct labor. 3. When a perpetual inventory system is used, physical counts should be made periodically to confirm the inventory balances on the books. 4. Abnormal shortages or thefts of inventory should be reported separately as operating expenses. 5. Normal inventory adjustments for shrinkage and breakage are reported as adjustments to cost of goods sold. 6. When the terms of a sale are FOB shipping point, goods in transit at year-end should be included in the inventory of the seller. 7. Title to goods shipped FOB destination remains with the seller from the shipping point to the destination point. 8. Goods held by customers on approval should be excluded from the seller's inventory. 9. Consigned goods are reported by the consignor in inventory at the sum of their cost, handling and shipping costs, and the estimated gross profit. 10. The LIFO conformity rule (IRS Regulations) does not permit companies to report inventory values using any method other than LIFO in the financial statements or in the attached notes. 177 11. In a period of rising prices, the use of FIFO relates the current high costs of acquiring goods with rising sales prices. As a result, FIFO tends to have a stabilizing effect on gross profit margins. 12. The gross method of accounting for purchase discounts is theoretically preferable to the net method. 13. The gross method of accounting for purchase discounts reflects the fact that discounts not taken are in effect credit-related expenditures incurred for failure to pay within the discount period. 14. The specific identification method is a highly objective approach to matching historical costs with revenues. 15. Specific identification as an inventory method matches the flow of recorded costs to the physical flow of goods. 16. LIFO assumes a cost flow that closely parallels the usual physical flow of goods sold. 17. With FIFO, inventories are reported on the balance sheet at or near their current value. 18. Unlike other inventory cost methods, the average cost approach provides the same unit cost for items of equal utility. 19. FIFO provides income tax savings during periods of falling prices. 20. The gross profit method is based on an assumed relationship between gross profit and net sales. 21. The gross profit method is an alternative inventory costing method used in the preparation of annual financial statements. 22. The gross profit method is useful when a periodic inventory system is used and inventories are required for interim financial statements. 178 23. In applying the gross profit method of estimating inventory, the gross profit may be stated as either a percentage of sales or a percentage of cost. 24. The markup percentage on sales can be expressed as the gross margin percentage less the cost percentage. 25. Overstating ending inventory will affect the balance sheet, but not the income statement. 26. Under the lower-of-cost-or-market rule, market value is always the lowest of three amounts-- replacement cost, floor, and ceiling. 27. Overstating purchases will cause the gross margin to be understated by the same amount. 28. The lower-of-cost-or-market method may be applied to each inventory item, to major classes or categories of inventory items, or to the inventory as a whole. 29. Application of lower of cost or market to individual items results in a higher inventory valuation than application to classes of inventory or inventory as a whole. 30. In valuing inventories at the lower of cost or market, the ceiling limitation is applied so that inventories are not valued at more than their net realizable value. 31. Overstating ending inventory in Period 1 will cause ending inventory in Period 2 to be understated by the same amount. MULTIPLE CHOICE 1. The use of the gross profit method assumes a. the amount of gross profit is the same as in prior years. b. sales and cost of goods sold have not changed from previous years. c. inventory values have not increased from previous years. d. the relationship between selling price and cost of goods sold is similar to prior years. 179 2. The gross profit method of estimating inventory would not be useful when a. a periodic system is in use and inventories are required for interim statements. b. inventories have been destroyed or lost by fire, theft, or other casualty, and the specific data required for inventory valuation are not available. c. there is a significant change in the mix of products being sold. d. the relationship between gross profit and sales remains stable over time. 3. The gross profit method of inventory valuation is invalid when a. there is substantial increase in the quantity of inventory during the year. b. there is substantial increase in the cost of inventory during the year. c. the gross margin percentage changes significantly during the year. d. all ending inventory is destroyed by fire before it can be counted. 4. When the current year's ending inventory amount is overstated, a. the current year's cost of goods sold is overstated. b. the current year's total assets are understated. c. the current year's net income is overstated. d. the next year's income is overstated. 5. If the ending inventory balance is understated, net income of the same period a. will be overstated. b. will be understated. c. will be unaffected. d. cannot be determined from the above information. 6. An overstatement of ending inventory in Period 1 would result in income of Period 2 being a. overstated. b. understated. c. correctly stated. d. The answer cannot be determined from the information given. 7. Which statement is true about the gross profit method? a. It may not be used to estimate inventories for annual statements. b. It may not be used to estimate inventories for interim statements. c. It may not be used by insurers of inventory. d. It may not be used for internal estimates of inventory. 8. Which of the following will result if the current year's ending inventory amount is understated in the cost of goods sold calculation? a. Cost of goods sold will be overstated. b. Total assets will be overstated. c. Net income will be overstated. d. Both a and c. 180 9. If ending inventory on December 31, 2004, is overstated by $30,000, what is the effect on net income for 2005? a. Net income is overstated by $30,000. b. Net income is understated by $30,000. c. Net income is overstated by $60,000. d. The answer cannot be determined from the information given. 10. The retail inventory method is characterized by a. the recording of sales at cost. b. the recording of purchases at selling price. c. the reporting of year-end inventory at retail in the financial statements. d. the recording of markups at retail and markdowns at cost. 11. What is the maximum amount at which inventory can be valued when the goods have experienced a permanent decline in value? a. Historical cost b. Sales price c. Net realizable value d. Net realizable value reduced by a normal profit margin 12. Net realizable value can be defined as a. selling price. b. selling price less costs to complete and sell. c. selling price plus costs to complete and sell. d. acquisition cost plus costs to complete and sell. 13. A markup of 25 percent on cost is equivalent to what markup on selling price? (rounded) a. 15 percent b. 20 percent c. 25 percent d. 33 percent 14. When would the replacement cost of inventory be used as the market value under the lower-ofcost-or-market method? a. Always. b. When replacement cost is above net realizable value. c. When replacement cost is below net realizable value and above net realizable value less normal profit margin. d. When replacement cost is below net realizable value less normal profit margin. 181 15. If the replacement cost of a unit of inventory has declined below original cost, but the replacement cost exceeds net realizable value, the amount to be used for purposes of inventory valuation is a. net realizable value. b. original cost. c. market value. d. net realizable value less a normal profit margin. 16. Under generally accepted accounting principles, the lower-of-cost-or-market procedure for assigning a value to inventory can be assigned to a. total inventory. b. groups of similar inventory items. c. individual inventory items. d. all of the above. 17. The lower-of-cost-or-market inventory procedure would be expected to result in the lowest inventory valuation when applied to a. total inventory. b. groups of similar inventory items. c. individual inventory items. d. none of the above. 18. When valuing raw materials inventory at lower of cost or market, what is the general meaning of the term "market"? a. Net realizable value b. Net realizable value less a normal profit margin c. Current replacement cost d. Discounted present value 19. An example of an inventory accounting policy that should be disclosed is the a. effect of inventory profits caused by inflation. b. classification of inventory into raw materials, work in process, and finished goods. c. identification of major suppliers. d. method used for inventory costing. 20. Hardy Company is a wholesale electronics distributor. On December 31, 2005, it prepared the following partial income statement: Gross sales ............................... $600,400 Sales discounts ........................... 400 Net sales ................................. $600,000 Cost of goods sold: Beginning inventory ..................... $200,000 Net purchases ........................... 300,000 182 Given this information, if Hardy Company's gross margin is 30 percent of net sales, what is the correct ending inventory balance? a. $80,000 b. $120,000 c. $180,000 d. $500,000 21. Miller Company needs an estimate of its ending inventory balance. The following information is available: Cost Retail Sales revenue ............................. $180,000 Beginning inventory ....................... $ 35,000 62,000 Net purchases ............................. 100,000 135,000 Gross margin percentage ................... 30% Given this information, when using the gross margin estimation method, ending inventory is approximately a. $1,000. b. $9,000. c. $19,000. d. $11,650. 22. The following information is available for the Becca Company for the three months ended June 30 of this year: Inventory, April 1 of this year ...................... $1,200,000 Purchases ............................................ 4,500,000 Freight-in ........................................... 300,000 Sales ................................................ 6,400,000 The gross margin was 25 percent of sales. What is the estimated inventory balance at June 30? a. $880,000 b. $933,000 c. $1,200,000 d. $1,500,000 23. Petersen Menswear, Inc. maintains a markup of 60 percent based on cost. The company's selling and administrative expenses average 30 percent of sales. Annual sales were $1,440,000. Petersen's cost of goods sold and operating profit for the year are | Cost of | Operating | Goods Sold | Profit a. $864,000 $144,000 b. $864,000 $432,000 c. $900,000 $108,000 d. $900,000 $432,000 183 24. On October 31, a flood at Payne Company's only warehouse caused severe damage to its entire inventory. Based on recent history, Payne has a gross profit of 25 percent of net sales. The following information is available from Payne's records for the ten months ended October 31: Inventory, January 1 .................................. $ 520,000 Purchases ............................................. 4,120,000 Purchase returns ...................................... 60,000 Sales ................................................. 5,600,000 Sales discounts ....................................... 400,000 A physical inventory disclosed usable damaged goods which Payne estimates can be sold for $70,000. Using the gross profit method, the estimated cost of goods sold for the ten months ended October 31 should be a. $680,000. b. $3,830,000. c. $3,900,000. d. $4,200,000. 25. The following information appears in Olsen Company's records for the year ended December 31: Inventory, January 1 .................................. $ 325,000 Purchases ............................................. 1,150,000 Purchase returns ...................................... 40,000 Freight-in ............................................ 30,000 Sales ................................................. 1,700,000 Sales discounts ....................................... 10,000 Sales returns ......................................... 15,000 On December 31, a physical inventory revealed that the ending inventory was only $210,000. Olsen's gross profit on net sales has remained constant at 30 percent in recent years. Olsen suspects that some inventory may have been pilfered by one of the company's employees. At December 31, what is the estimated cost of missing inventory? a. $75,000 b. $82,500 c. $210,000 d. $292,500 26. Davis Company's accounting records indicated the following information: Inventory, 1/1/05..................................... 1,000,000 Purchases during 2005 ................................. 5,000,000 Sales during 2005 ..................................... 6,400,000 A physical inventory taken on December 31, 2005, revealed actual ending inventory at cost was $1,150,000. Davis' gross profit on sales has regularly been about 25 percent in recent years. The company believes some inventory may have been stolen during the year. What is the estimated amount of missing inventory at December 31, 2005? a. $50,000 b. $200,000 c. $350,000 d. $450,000 184 27. On June 19, 2005, a fire destroyed the entire uninsured merchandise inventory of the Allen Merchandising Company. The following data are available: Inventory, January 1 .................................. $ 80,000 Purchases, January 1 through June 19 .................. 560,000 Sales, January 1 through June 19 ...................... 776,000 Markup percentage on cost ............................. 25% What is the approximate inventory loss as a result of the fire? a. $19,200 b. $27,200 c. $34,000 d. $58,000 28. Commodity X sells for $12.00; selling expenses are $2.40; normal profit is $3.00. If the cost of Commodity X is $7.80 and the replacement cost is $6.00, the lower of cost or market is a. $5.40. b. $6.00. c. $6.60. d. $7.80. 29. The following information is available for Torino Corp. for its most recent year: Net sales ............................................. $3,600,000 Freight-in ............................................ 90,000 Purchase discounts .................................... 50,000 Ending inventory ...................................... 240,000 The gross margin is 40 percent of net sales. What is the cost of goods available for sale? a. $1,680,000 b. $1,920,000 c. $2,400,000 d. $2,440,000 30. Venus Inc. carries Product A in inventory on December 31 at its unit cost of $22.50. Because of a sharp decline in demand for the product, the selling price is reduced to $24.00 per unit. Venus' normal profit margin on Product A is $4.80, disposal costs are $3.00 per unit, and the replacement cost is $15.90. Under the rule of lower of cost or market, Venus' December 31 inventory of Product A should be valued at a unit cost of a. $15.90. b. $16.20. c. $21.00. d. $22.50. 31. A company sells four products: I, II, III, and IV. The company values all inventories using the lower-of-cost-or-market procedure. The company has consistently experienced a profit margin of 20 percent of sales and expects this rate to hold for the future. Additional information, shown below, is available for the most recent year as of December 31. 185 | Original | Cost to | Estimated Cost | Expected Selling | | Product | Cost | Replace | to Sell | Prices | I | $60 | $70 | $10 | $100 | II | 70 | 90 | 20 | 120 | III | 80 | 60 | 10 | 60 | IV | 90 | 80 | 20 | 90 Using the lower-of-cost-or-market procedure, what is the reported inventory value at December 31 for one unit of Product I? a. $60 b. $70 c. $80 d. $90 32. A company sells four products: I, II, III, and IV. The company values all inventories using the lower-of-cost-or-market procedure. The company has consistently experienced a profit margin of 20 percent of sales and expects this rate to hold for the future. Additional information, shown below, is available for the most recent year as of December 31. | Original | Cost to | Estimated Cost | Expected Selling | | Product | Cost | Replace | to Sell | Prices | I | $60 | $70 | $10 | $100 | II | 70 | 90 | 20 | 120 | III | 80 | 60 | 10 | 60 | IV | 90 | 80 | 20 | 90 Using the lower-of-cost-or-market procedure, what is the reported inventory value at December 31 for one unit of Product II? a. $70 b. $76 c. $90 d. $96 33. The Garrett Corporation uses the lower-of-cost-or-market method to value inventory. Data regarding the items in work-in-process inventory are presented below. Markers Pens Highlighters Historical cost ................ $24,000 $18,880 $30,000 Selling price .................. 36,000 36,000 36,000 Estimated cost to complete ..... 4,800 4,800 6,800 Replacement cost ............... 20,800 16,800 31,800 Normal profit margin as a percentage of selling price .... 25% 25% 10% The value for cost to be used in the lower-of-cost-or-market comparison for the markers is a. $20,800. b. $23,400. c. $24,000. d. $31,200. 186 34. The Garrett Corporation uses the lower-of-cost-or-market method to value inventory. Data regarding the items in work-in-process inventory are presented below. Markers Pens Highlighters Historical cost ................ $24,000 $18,880 $30,000 Selling price .................. 36,000 36,000 36,000 Estimated cost to complete ..... 4,800 4,800 6,800 Replacement cost ............... 20,800 16,800 31,800 Normal profit margin as a percentage of selling price .... 25% 25% 10% When valuing the pens, the market value to be used in the lower-of-cost-or- market comparison is a. $22,200. b. $31,200. c. $16,800. d. $18,800. 35. The Garrett Corporation uses the lower-of-cost-or-market method to value inventory. Data regarding the items in work-in-process inventory are presented below. Markers Pens Highlighters Historical cost ................ $24,000 $18,880 $30,000 Selling price .................. 36,000 36,000 36,000 Estimated cost to complete ..... 4,800 4,800 6,800 Replacement cost ............... 20,800 16,800 31,800 Normal profit margin as a percentage of selling price .... 25% 25% 10% The inventory valuation for highlighters using the lower-of-cost-or-market method is a. $25,600. b. $29,200. c. $31,800. d. $30,000. 36. The following information is available for the Neptune Company for the three months ended March 31 of this year: Inventory, January 1 .................................. $ 450,000 Purchases ............................................. 1,700,000 Freight-in ............................................ 100,000 Sales ................................................. 2,400,000 The gross margin was estimated to be 25 percent of sales. What is the estimated inventory balance at March 31? a. $350,000 b. $450,000 c. $562,500 d. $600,000 187 37. Elrond Company began operations in 2003. During the first two years of operations, Elrond made undiscovered errors in taking its year-end inventories that understated 2003 ending inventory by $40,000 and overstated 2004 ending inventory by $50,000. The combined effect of these errors on reported income is 2003 2004 2005 a. understated $40,000 overstated $50,000 not affected b. understated $40,000 overstated $10,000 not affected c. understated $40,000 overstated $90,000 understated $50,000 d. overstated $40,000 understated $50,000 overstated $10,000 38. Elrond Company began operations in 2003. During the first two years of operations, Elrond made undiscovered errors in taking its year-end inventories that overstated 2003 ending inventory by $50,000 and overstated 2004 ending inventory by $40,000. The combined effect of these errors on reported income is 2003 2004 2005 a. overstated $50,000 overstated $90,000 understated $40,000 b. overstated $50,000 overstated $40,000 not affected c. understated $50,000 understated $90,000 not affected d. overstated $50,000 understated $10,000 understated $40,000 39. Elrond Company began operations in 2003. During the first two years of operations, Elrond made undiscovered errors in taking its year-end inventories that overstated 2003 ending inventory by $50,000 and understated 2004 ending inventory by $40,000. The combined effect of these errors on reported income is 2003 2004 2005 a. understated $50,000 overstated $90,000 understated $40,000 b. overstated $50,000 understated $90,000 not affected c. overstated $50,000 understated $40,000 not affected d. overstated $50,000 understated $90,000 overstated $40,000 40. Jupiter Company prepares monthly income statements. A physical inventory is taken only at year-end; hence, month-end inventories must be estimated. All sales are made on account. The rate of markup on cost is 50 percent. The following information relates to the month of May: Accounts receivable, May 1 ............................ $20,000 Accounts receivable, May 31 ........................... 30,000 Collection of accounts receivable during May .......... 50,000 Inventory, May 1 ...................................... 36,000 Purchases of inventory during May ..................... 32,000 188 The estimated cost of the May 31 inventory is a. $24,000. b. $28,000. c. $38,000. d. $44,000. 41. A company sells four products: I, II, III and IV. The company values all inventories using the lower-of-cost-or-market procedure. The company has consistently experienced a profit margin of 20 percent of sales and expects this rate to hold for the future. Additional information, shown below, is available for the most recent year as of December 31. | Original | Cost to | Estimated Cost | Expected Selling | | Product | Cost | Replace | to Sell | Prices | I | $60 | $70 | $10 | $100 | II | 70 | 90 | 20 | 120 | III | 80 | 60 | 10 | 60 | IV | 90 | 80 | 20 | 90 Using the lower-of-cost-or-market procedure, what is the reported inventory value at December 31 for one unit of Product III? a. $50 b. $60 c. $70 d. $80 42. A company sells four products: I, II, III, and IV. The company values all inventories using the lower-of-cost-or-market procedure. The company has consistently experienced a profit margin of 20 percent of sales and expects this rate to hold for the future. Additional information, shown below, is available for the most recent year as of December 31. | Original | Cost to | Estimated Cost | Expected Selling | | Product | Cost | Replace | to Sell | Prices | I | $60 | $70 | $10 | $100 | II | 70 | 90 | 20 | 120 | III | 80 | 60 | 10 | 60 | IV | 90 | 80 | 20 | 90 Using the lower-of-cost-or-market procedure, what is the reported inventory value at December 31 for one unit of Product IV? a. $60 b. $70 c. $80 d. $90 43. Which of the following would not be included in the cost of work in process inventory? a. Cost of electricity to operate factory equipment b. Maintenance costs of factory equipment c. Depreciation on office equipment in the sales manager's office d. Depreciation on factory equipment 189 44. The term LIFO reserve refers to a. a cost flow assumption for valuing inventory. b. a special fund set aside to cover LIFO liquidations. c. inventory pools used in the dollar-value LIFO method. d. the difference between the ending inventory amount under LIFO and the ending inventory amount under another inventory cost flow assumption. 45. Which of the following statements is true? a. A company must use the FIFO cost flow assumption for taxes as well as for financial accounting and reporting. b. A company may use FIFO for inventory valuation purposes on the balance sheet provided that LIFO cost of goods sold is reported on the income statement. c. Application of LIFO for financial reporting purposes must strictly follow IRS regulations relating to LIFO. d. LIFO is the only inventory method that must be used for financial reporting purposes if used for tax purposes. 46. If a company experiences a liquidation of a LIFO inventory layer in the second quarter that is expected to be restored by the end of the annual financial reporting period, the company should a. treat the layer as if it were liquidated and include in cost of goods sold the expected replacement cost of the inventory sold. b. deplete the LIFO layer as if the interim period were an annual period. c. change to an alternative inventory cost method, such as FIFO, so that the problem of LIFO liquidation is not encountered. d. delay the recognition of both revenue and cost of goods sold on the inventory involved until a final determination of the LIFO inventory can be made at the end of the annual period. 47. Which of the following would not be reported as inventory? a. Land acquired for resale by a real estate firm b. Stocks and bonds held for resale by a brokerage firm c. Partially completed goods held by a manufacturing company d. Machinery acquired by a manufacturing company for use in the production process 48. Goods on consignment are a. included in the consignee's inventory. b. recorded in a consignment out account which is an inventory account. c. recorded in a consignment in account which is an inventory account. d. All of the above. 49. Which of the following describes the flow of product costs through the inventory accounts of a manufacturer? a. Raw materials, goods in process, factory overhead, finished goods b. Raw materials, goods in process, finished goods 190 c. Raw materials, direct labor, factory overhead, finished goods d. Raw materials, direct labor, factory overhead 50. Western Manufacturing Company uses a perpetual inventory system for its raw materials. The inventory records reflect a raw materials balance of $378,500 at December 31. A physical inventory taken on that date revealed raw materials of $375,750. How will the $2,750 difference affect raw materials inventory and cost of goods sold, assuming it is attributed to normal shrinkage? Raw Materials Cost of Goods Sold a. Increase Decrease b. Decrease No effect c. Decrease Increase d. No effect Increase 51. Cost of goods sold is equal to a. the cost of inventory on hand at the end of a period plus net purchases minus the cost of inventory on hand at the beginning of a period. b. the cost of inventory on hand at the beginning of a period minus net purchases plus the cost of inventory on hand at the end of a period. c. the cost of inventory on hand at the beginning of a period plus net sales minus the cost of inventory on hand at the end of a period. d. the cost of inventory on hand at the beginning of a period plus net purchases minus the cost of inventory on hand at the end of a period. 52. Goods on consignment should be included in the inventory of a. the consignor but not the consignee. b. the consignee but not the consignor. c. both the consignor and the consignee. d. neither the consignor nor the consignee. 53. The use of a discounts lost account implies that the recorded cost of a purchased inventory item is its a. invoice price. b. invoice price plus the purchase discount lost. c. invoice price less the purchase discount taken. d. invoice price less the purchase discount allowable whether taken or not. 54. A company using a periodic inventory system neglected to record a purchase of merchandise on account at year-end. This merchandise was omitted from the year-end physical count. How will these errors affect inventory at year-end and cost of goods sold for the year? 191 Cost of | Inventory | Goods Sold | a. | No effect Understate b. No effect Overstate c. Understate Understate d. Understate No effect 55. Which inventory costing method would not be appropriate for a manufacturer using a perpetual inventory system? a. First-in, first-out b. Last-in, first-out c. Average cost d. Dollar-value LIFO 56. If goods shipped FOB destination are in transit at the end of the year, they should be included in the inventory balance of the a. seller. b. common carrier. c. buyer. d. bank. 57. In a period of falling prices, the use of which of the following inventory cost flow methods would typically result in the highest cost of goods sold? a. FIFO b. LIFO c. Weighted average cost d. Specific identification 58. The specific identification method of inventory costing a. eliminates all opportunity for profit manipulation. b. matches the flow of recorded costs with the physical flow of goods. c. can be used only with a perpetual inventory system. d. is a violation of generally accepted accounting principles. 59. Merchandise shipped FOB shipping point on the last day of the year should ordinarily be included in a. the buyer's inventory balance. b. the seller's inventory balance. c. neither the buyer's nor seller's inventory balance. d. both the buyer's and the seller's inventory balances. 192 60.Which inventory pricing method best approximates specific identification in most manufacturing situations? a. Activity-based costing b. FIFO c. Average cost d. LIFO 61. In a period of rising prices, the inventory cost allocation method that tends to result in the lowest reported net income is a. LIFO. b. FIFO. c. moving average. d. weighted average. 62. The Allen Company makes the following entry in its accounting records: Inventory ................................. 200 Cost of Goods Sold ........................ 200 This entry would be made when a. merchandise is sold and the periodic inventory method is used. b. merchandise is sold and the perpetual inventory method is used. c. merchandise is returned and the perpetual inventory method is used. d. merchandise is returned and the periodic inventory method is used. 63. Which of the following is not true of the perpetual inventory method? a. Purchases are recorded as debits to the inventory account. b. The entry to record a sale includes a debit to Cost of Goods Sold and a credit to Inventory. c. After a physical inventory count, Inventory is credited for any missing inventory. d. Purchase returns are recorded by debiting Accounts Payable and crediting Purchase Returns and Allowances. 64. Goods in transit at year-end purchased FOB shipping point were appropriately recorded in the purchases account but were incorrectly excluded from the ending inventory. What effect will this omission have on the company's assets, liabilities, and retained earnings at year-end? a. No effect, no effect, overstated b. No effect, no effect, understated c. Understated, no effect, overstated d. Understated, no effect, understated 193 65. A company records inventory at the gross invoice price. Theoretically, how should the following affect the costs in inventory? | Warehousing | Cash Discounts | Costs | Available a. Increase Decrease b. No effect Decrease c. No effect No effect d. Increase No effect 66. When using the periodic inventory method, which of the following generally would not be separately accounted for in the computation of cost of goods sold? a. Trade discounts applicable to purchases during the period b. Cash (purchase) discounts taken during the period c. Purchase returns and allowances of merchandise during the period d. Cost of transportation-in for merchandise purchases during the period 67. A firm using the perpetual inventory method returned defective merchandise costing $2,000 to one of its suppliers. The entry to record this transaction will include a debit to a. Accounts Receivable. b. Inventory. c. Purchase Returns and Allowances. d. Accounts Payable. 68. The average cost method is applicable to which of the following inventory systems? Periodic Perpetual a. Yes Yes b. Yes No c. No Yes d. No No 69. The LIFO inventory cost flow method may be applied to which of the following inventory systems? | Periodic | Perpetual | a. | No No b. No Yes c. Yes Yes d. Yes No 194 70. Which of the following inventory costing methods reports most closely the current cost of inventory on the balance sheet? a. FIFO b. Specific identification c. Weighted average d. LIFO 71. Which of the following will occur when inventory costs are decreasing? a. LIFO will result in lower net income and lower ending inventory than will FIFO. b. FIFO will result in lower net income and lower ending inventory than will LIFO. c. LIFO will result in a lower net income, but a higher ending inventory, than will FIFO. d. FIFO will result in a lower net income, but a higher ending inventory, than will LIFO. 72. During periods of rising prices, when the FIFO inventory cost flow method is used, a perpetual inventory system would a. not be permitted. b. result in a higher ending inventory than a periodic inventory system. c. result in the same ending inventory as a periodic inventory system. d. result in a lower ending inventory than a periodic inventory system. 73. Which of the inventory cost flow assumptions provides the best measure of earnings, where "best" means most appropriate for predicting future earnings, when prices have been declining? a. FIFO b. Specific identification c. LIFO d. Average cost 74. Assume that a company records purchases net of discount. If the company bought merchandise valued at $10,000 on credit terms 3/15, net 30, the entry to record a payment for half of the purchase within the discount period would include a debit to a. Accounts Payable for $4,850 and a credit to Cash for $4,850. b. Accounts Payable for $5,000 and a credit to Cash for $5,000. c. Accounts Payable for $4,850 and to Interest Expense for $150, and a credit to Cash for $5,000. d. Accounts Payable for $5,000 and to Interest Revenue for $150 and to Cash for $5,000. 75. On August 1, Stephan Company recorded purchases of inventory of $80,000 and $100,000 under credit terms of 2/15, net 30. The payment due on the $80,000 purchase was remitted on August 14. The payment due on the $100,000 purchase was remitted on August 29. Under the net method and the gross method, these purchases should be included at what respective net amounts in the determination of cost of goods available for sale? 195 | Net Method | Gross Method | a. | $178,400 $176,400 b. $176,400 $176,400 c. $176,400 $178,400 d. $180,000 $176,400 76. Ami Retailers purchased merchandise with a list price of $100,000, subject to a trade discount of 20 percent and credit terms of 2/10, n/30. At what amount should Ami record the cost of this merchandise if the gross method is used? a. $100,000 b. $80,000 c. $98,000 d. $78,400 77. With LIFO, cost of goods sold is $195,000, and ending inventory is $45,000. If FIFO ending inventory is $65,000, how much is FIFO cost of goods sold? a. $215,000 b. $195,000 c. $175,000 d. $65,000 78. Holdaway Co., a manufacturer, had inventories at the beginning and end of its current year as follows: Beginning End Raw materials ............................. $11,000 $15,000 Work in process ........................... 20,000 24,000 Finished goods ............................ 12,500 9,000 During the year, the following costs and expenses were incurred: Raw materials purchased ............................... $150,000 Direct labor cost ..................................... 60,000 Indirect factory labor ................................ 30,000 Taxes and depreciation on factory building ............ 10,000 Taxes and depreciation on sales room and office ....... 7,500 Sales salaries ........................................ 20,000 Office salaries ....................................... 12,000 Utilities (60% applicable to factory, 20% to sales room, and 20% to office) .................................... 25,000 Holdaway's cost of goods sold for the year is a. $257,000. b. $260,500. c. $261,000. d. $269,500. 196 79. Barlow Company's Accounts Payable balance at December 31, 2005, was $1,800,000 before considering the following transactions: • Goods were in transit from a vendor to Barlow on December 31, 2005. The invoice price was $100,000, and the goods were shipped FOB shipping point on December 29, 2005. The goods were received on January 4, 2006. • Goods shipped to Barlow FOB shipping point on December 20, 2005, from a vendor were lost in transit. The invoice price was $50,000. On January 5, 2006, Barlow filed a $50,000 claim against the common carrier. In its December 31, 2005, balance sheet, Barlow should report Accounts Payable of a. $1,950,000. b. $1,900,000. c. $1,850,000. d. $1,800,000. 80. Miller Inc. is a wholesaler of office supplies. The activity for Model III calculators during August is shown below: Balance/ Date Transaction Units Cost August 1 Inventory 2,000 $36.00 7 Purchase 3,000 37.20 12 Sales 3,600 21 Purchase 4,800 38.00 22 Sales 3,800 29 Purchase 1,600 38.60 If Miller Inc. uses a FIFO periodic inventory system, the ending inventory of Model III calculators at August 31 is reported as a. $150,080. b. $150,160. c. $152,288. d. $152,960. 81. Miller Inc. is a wholesaler of office supplies. The activity for Model III calculators during August is shown below: Balance/ Date Transaction Units Cost August 1 Inventory 2,000 $36.00 7 Purchase 3,000 37.20 12 Sales 3,600 21 Purchase 4,800 38.00 22 Sales 3,800 29 Purchase 1,600 38.60 197 If Miller Inc. uses a LIFO periodic inventory system, the ending inventory of Model III calculators at August 31 is reported as a. $146,400. b. $150,080. c. $150,160. d. $152,960. 82. Miller Inc. is a wholesaler of office supplies. The activity for Model III calculators during August is shown below: Balance/ Date Transaction Units Cost August 1 Inventory 2,000 $36.00 7 Purchase 3,000 37.20 12 Sales 3,600 21 Purchase 4,800 38.00 22 Sales 3,800 29 Purchase 1,600 38.60 If Miller Inc. uses a LIFO cost perpetual inventory system, the ending inventory of Model III calculators at August 31 is reported as a. $146,400. b. $150,080. c. $150,160. d. $152,960. 83. Miller Inc. is a wholesaler of office supplies. The activity for Model III calculators during August is shown below: Balance/ Date Transaction Units Cost August 1 Inventory 2,000 $36.00 7 Purchase 3,000 37.20 12 Sales 3,600 21 Purchase 4,800 38.00 22 Sales 3,800 29 Purchase 1,600 38.60 If Miller Inc. uses a FIFO cost perpetual inventory system, the ending inventory of Model III calculators at August 31 is reported as a. $150,080. b. $150,160. c. $152,232. d. $152,960. 84. Stephens Inc. is a wholesaler of photography equipment. The activity for the VTC cameras during July follows: Balance/ Date Transaction Units Cost | July 1 | Inventory | 2,000 | $36.00 | 7 | Purchase | 3,000 | 37.00 198 12 Sales 3,600 21 Purchase 5,000 37.88 22 Sales 3,800 29 Purchase 1,600 38.11 If Stephens Inc. uses the average cost method to account for inventory, the ending inventory of VTC cameras at July 31 is reported as a. $153,400. b. $156,912. c. $158,736. d. $159,464. 85. Stephens Inc. is a wholesaler of photography equipment. The activity for the VTC cameras during July is shown below: Balance/ Date Transaction Units Cost July 1 Inventory 2,000 $36.00 7 Purchase 3,000 37.00 12 Sales 3,600 21 Purchase 5,000 37.88 22 Sales 3,800 29 Purchase 1,600 38.11 If Stephens Inc. uses a moving average perpetual inventory system, the ending inventory of the VTC cameras at July 31 is reported as a. $153,400. b. $156,912. c. $158,736. d. $159,464. 86. The following information is available for Lyman Company: Cost of goods sold for 2005 ........................... $1,200,000 Inventories at December 31, 2004 ...................... 350,000 Inventories at December 31, 2005 ...................... 310,000 Assuming that a business year consists of 360 days, the number of days' sales in average inventories for 2005 was a. 49.5. b. 93. c. 99. d. 105. 87. Following are the account balances from Fulton Company's income statement: Inventory, January 1, 2005 ............................ $30,000 Purchases ............................................. 40,000 Purchase Returns and Allowances ....................... 5,000 Purchase Discounts .................................... 4,000 199 Freight-In ............................................ 5,000 Inventory, December 31, 2005 .......................... 15,000 Freight-Out ........................................... 6,000 Given this information, the cost of goods sold during 2005 is a. $51,000. b. $46,000. c. $56,000. d. $66,000. 88. Following are the account balances from Jackson Company's income statement: Inventory, January 1, 2005 ............................ $35,000 Purchases ............................................. 35,000 Purchase Returns and Allowances ....................... 2,000 Purchase Discounts .................................... 4,000 Freight-In ............................................ 5,000 Inventory, December 31, 2005 .......................... 10,000 Freight-Out ........................................... 6,000 Given this information, the cost of merchandise available for sale during 2005 is a. $65,000. b. $59,000. c. $69,000. d. $61,000. 89. From the following information, determine the amount of freight-in. Beginning Inventory ................................... $20,000 Purchases ............................................. 41,000 Purchase Returns and Allowances ....................... 3,000 Purchase Discounts .................................... 4,000 Freight-In ............................................ ? Cost of Goods Available for Sale ...................... 55,000 Ending Inventory ...................................... ? Cost of Goods Sold .................................... 22,000 a. $3,000 b. $4,000 c. $2,000 d. $1,000 90. From the following information, determine the amount of ending inventory. Beginning Inventory ................................... $20,000 Purchases ............................................. 41,000 Purchase Returns and Allowances ....................... 3,000 Purchase Discounts .................................... 4,000 Freight-In ............................................ ? Cost of Goods Available for Sale ...................... 55,000 Ending Inventory ...................................... ? 200 Cost of Goods Sold .................................... 22,000 a. $23,000 b. $32,000 c. $33,000 d. $22,000 91. The following information was obtained from the accounts of McKay Company: Inventory, January 1 .................................. $30,000 Purchases ............................................. 45,000 Purchase Returns and Allowances ....................... 5,000 Purchase Discounts .................................... 4,000 Freight-In ............................................ 5,000 Inventory, December 31 ................................ 20,000 Freight-Out ........................................... 6,000 Given this information, the cost of goods sold during the year is a. $46,000. b. $41,000. c. $51,000. d. $61,000. 92. During the year, The Hill Company purchased $1,920,000 of inventory. The cost of goods sold for the year was $1,800,000 and the ending inventory at December 31 was $360,000. What was the inventory turnover for the year? a. 5.0 b. 5.3 c. 6.0 d. 6.4 93. The following information was obtained from the accounts of Cox Company: Beginning Inventory .................................. $20,000 Purchases ............................................ 40,000 Purchase Returns and Allowances ...................... 2,000 Purchase Discounts ................................... 4,000 Freight-In ........................................... 5,000 Ending Inventory ..................................... 10,000 Freight-Out .......................................... 6,000 Given this information, the cost of goods available for sale is a. $65,000. b. $59,000. c. $69,000. d. $61,000. 94. Selected information from the accounting records of Thayer Company is as follows: Net sales for 2005 ................................... $900,000 201 Cost of goods sold for 2005 .......................... 600,000 Inventory at December 31, 2004 ....................... 180,000 Inventory at December 31, 2005 ....................... 156,000 Thayer's inventory turnover for 2005 is a. 5.36 times. b. 3.85 times. c. 3.67 times. d. 3.57 times. 95. The following information applied to Landon Company for 2005: Merchandise purchased for resale ..................... $300,000 Freight-in ........................................... 7,500 Interest on notes payable to vendors ................. 3,000 Purchase returns ..................................... 1,500 Landon's inventoriable cost for 2005 was a. $309,000. b. $307,500. c. $306,000. d. $301,500. 96. Purchases and sales during a recent period for Coleman, Inc. were: Purchases During the Period Sales During the Period | 1st Purchase 2nd Purchase 3rd Purchase 4th Purchase | 500 units 1,000 units 500 units 500 units 2,500 units | @ @ @ @ | $2 $3 $4 $5 | 1st Sale 2nd Sale 3rd Sale 4th Sale | 600 units 750 units 500 units 500 units 2,350 units | @ @ @ @ $7 $8 $9 $10 Beginning inventory was 100 units at $1 each. Given this information, what is the ending inventory if the periodic FIFO costing alternative is used? a. $400 b. $500 c. $1,250 d. $3,100 97. Purchases and sales during a recent period for Coleman, Inc. were: Purchases During the Period Sales During the Period 1st Purchase 500 units @ $2 1st Sale 600 units @ $7 2nd Purchase 1,000 units @ $3 2nd Sale 750 units @ $8 3rd Purchase 500 units @ $4 3rd Sale 500 units @ $9 4th Purchase 500 units @ $5 4th Sale 500 units @ $10 2,500 units 2,350 units 202 Beginning inventory was 100 units at $1 each. Given this information, what is the ending inventory if the periodic LIFO costing alternative is used? a. $400 b. $500 c. $1,250 d. $3,100 98. Purchases and sales during a recent period for Coleman, Inc. were Purchases During the Period Sales During the Period | 1st Purchase 2nd Purchase 3rd Purchase 4th Purchase | 500 units 1,000 units 500 units 500 units 2,500 units | @ @ @ @ | $2 $3 $4 $5 | 1st Sale 2nd Sale 3rd Sale 4th Sale | 600 units 750 units 500 units 500 units 2,350 units | @ @ @ @ | $7 $8 $9 $10 Beginning inventory was 100 units at $1 each. Given this information, what is the cost per unit available for sale during the year when using the average cost method (rounded to the nearest cent)? a. $2.61 b. $3.10 c. $3.31 d. $3.53 99. The following information was taken from Frandsen Company's accounting records: Increase in raw materials inventory ................... $ 7,500 Decrease in finished goods inventory .................. 17,500 Raw materials purchase ................................ 215,000 Direct-labor payroll .................................. 100,000 Factory overhead ...................................... 150,000 Freight-out ........................................... 22,500 There was no work-in-process inventory at the beginning or end of the year. Frandsen's cost of goods sold is a. $497,500. b. $487,500. c. $482,500. d. $475,000. 100. The following information is available for Hudson Company: Disbursements for purchases ........................... $290,000 Increase in trade accounts payable .................... 25,000 Decrease in merchandise inventory ..................... 10,000 Cost of goods sold was a. $325,000. b. $305,000. c. $275,000. d. $255,000. 203 101. The following information is available for Carter Corporation for the month of June: Beginning Inventory ............. 8 units @ $20.00 = $160 Purchased, June 3 ............... 5 units @ $22.00 = $110 Purchased, June 5 ............... 7 units @ $24.00 = $168 Sold, June 9 .................... 9 units Purchased, June 15 .............. 8 units @ $26.00 = $208 Sold, June 19 ................... 7 units Given this information, the ending inventory balance using the average cost method is a. $276. b. $302. c. $368. d. $386. 102. Janice's Sporting Goods had the following inventory records for one line of skis for the month of January: Beginning Inventory ............. 70 pairs @ $100 per pair = $7,000 Sales (Jan. 1 - Jan. 7) ......... 50 pairs Purchase (Jan. 8) ............... 46 pairs @ $104 per pair = $4,784 Sales (Jan. 9 - Jan. 16) ........ 49 pairs Purchase (Jan. 17) .............. 62 pairs @ $110 per pair = $6,820 Sales (Jan. 18 - Jan. 29) ....... 56 pairs Purchase (Jan. 30) .............. 18 pairs @ $112 per pair = $2,016 Assuming the periodic LIFO inventory method is used, what is the cost of Janice's ending inventory? a. $4,124 b. $4,268 c. $4,376 d. $4,100 103. Gordon Company's inventory at June 30, 2005, was $75,000 based on a physical count of goods priced at cost, and before any necessary year-end adjustment relating to the following: • Included in the physical count were goods billed to a customer FOB shipping point on June 30, 2005. These goods had a cost of $1,500 and were picked up by the carrier on July 10, 2005. • Goods shipped FOB destination on June 28, 2005, from a vendor to Gordon were received on July 3, 2005. The invoice cost was $2,500. What amount should Gordon report as inventory on its June 30, 2005, balance sheet? a. $73,500 b. $74,000 c. $75,000 d. $76,500 204 104. The balance in Master Company's accounts payable account at December 31, 2005, was $1,100,000 before considering the following information: • Goods shipped FOB shipping point on December 20, 2005, from a vendor to Master were lost in transit. The invoice cost of $20,000 was not recorded by Master. On January 6, 2006, Master filed a $20,000 claim against the common carrier. • On December 27, 2005, a vendor authorized Master to return, for full credit, goods shipped and billed at $35,000 on December 2, 2005. The returned goods were shipped by Master on December 27, 2005. A $35,000 credit memo was received and recorded by Master on January 6, 2006. What amount should Master report as accounts payable in its December 31, 2005, balance sheet? a. $1,120,000 b. $1,115,000 c. $1,085,000 d. $1,065,000 105. The balance in Stockwell Company's accounts payable account on December 31, 2005, was $1,225,000 before the following information was considered: • Goods shipped FOB destination on December 21, 2005, from a vendor to Stockwell were lost in transit. The invoice cost of $45,000 was not recorded by Stockwell. On December 28, 2005, Stockwell notified the vendor of the lost shipment. • Goods were in transit from a vendor to Stockwell on December 31, 2005. The invoice cost was $60,000, and the goods were shipped FOB shipping point on December 28, 2005. Stockwell received the goods on January 6, 2006. What amount should Stockwell report as accounts payable in its December 31, 2005, balance sheet? a. $1,330,000 b. $1,285,000 c. $1,270,000 d. $1,225,000 106. The following information is available from Preston Company's 2005 accounting records: Purchases ............................................ $530,000 Purchase discounts ................................... 10,000 Beginning inventory .................................. 160,000 Ending inventory ..................................... 215,000 Freight-out .......................................... 40,000 Preston's 2005 cost of goods sold is a. $465,000. b. $475,000. c. $505,000. d. $585,000. 205 107. Campbell's Clothing Store sells jeans. During January 2005, its inventory records for one brand of designer jeans were as follows: Beginning Inventory .................... 10 pairs @ $ 20 = $ 200 January 6 Purchase ..................... 4 pairs @ 25 = 100 January 10 Sale ........................ 5 pairs January 15 Purchase .................... 7 pairs @ 30 = 210 January 20 Sale ........................ 10 pairs January 25 Purchase .................... 4 pairs @ 30 = 120 Using this information, periodic FIFO cost of goods sold is a. $330. b. $300. c. $430. d. $250. 108. Campbell's Clothing Store sells jeans. During January 2005, its inventory records for one brand of designer jeans were as follows: Beginning Inventory .................... 10 pairs @ $ 20 = $ 200 January 6 Purchase ..................... 4 pairs @ 25 = 100 January 10 Sale ........................ 5 pairs January 15 Purchase .................... 7 pairs @ 30 = 210 January 20 Sale ........................ 10 pairs January 25 Purchase .................... 4 pairs @ 30 = 120 Using this information, periodic LIFO cost of goods sold is a. $360. b. $300. c. $330. d. $430. 109. Campbell's Clothing Store sells jeans. During January 2005, its inventory records for one brand of designer jeans were as follows: Beginning Inventory .................... 10 pairs @ $ 20 = $ 200 January 6 Purchase ..................... 4 pairs @ 25 = 100 January 10 Sale ........................ 5 pairs January 15 Purchase .................... 7 pairs @ 30 = 210 January 20 Sale ........................ 10 pairs January 25 Purchase .................... 4 pairs @ 30 = 120 Using this information, the cost of goods sold using the average cost method is a. $378. b. $358. c. $265. d. $236. 206 110. Selected information from the 2005 and 2004 financial statements of BN Company is presented below: (in thousands) As of December 31 2005 2004 Cash .................................... $ 21 $ 35 Accounts receivable (net) ............... 60 98 Inventory ............................... 105 142 Prepaid expenses ........................ 5 3 Cash sales .............................. 750 675 | Credit sales (percent of cash sales) .... Cost of goods sold (percent of total sales) | 82% | 85% | 60% | 58% | Net income .............................. 30 38 BN Company's merchandise inventory turnover for 2005 is a. 3.43. b. 5.68. c. 6.63. d. 6.79. MATCHING Select the term that best fits each of the following definitions and descriptions: a. Product costs b. Consigned goods c. LIFO reserve d. Net method e. Dollar-value LIFO inventory method f. Factory overhead g. Raw materials h. Trade discount i. Perpetual inventory system j. FIFO k. LIFO l. FOB destination m. Gross method n. Work in process o. LIFO conformity rule p. LIFO inventory pools q. Specific identification r. Periodic inventory system s. FOB shipping point t. Period costs u. NIFO 1. Terms under which title to merchandise transfers to the purchaser when the goods are received. 2. A method of inventory valuation that reports inventory after consideration of any purchase discounts. 3. A discount that converts a list price to the price a purchaser is actually charged. 207 4. The classification of inventory into items having common characteristics. The LIFO historical cost method is then applied to each grouping. 5. All manufacturing costs except direct materials and direct labor. 6. Inventory that is partially processed and requires additional work before it can be sold. 7. A cost flow assumption that normally approximates the actual physical flow of the merchandise. 8. A regulation that requires the use of LIFO for financial reporting purposes if LIFO is used for income tax purposes. 9. The inventory method that matches the cost flow to the physical flow of the asset. 10. A valuation method that reports the inventory cost before the consideration of purchase discounts. 11. Records that provide a continuous summary of inventory activity. 12. Costs that are recognized as expenses during the period in which they are incurred. 13. The historical cost flow assumption that best matches current cost to current revenues. 14. Inventory that is physically located at a dealer, but the title is retained by the shipper until the merchandise is sold. PROBLEMS 1. The following data relate to the records of Powell Corp. for the month of September: Sales ................................................. $160,000 Beginning inventory ................................... $ 20,000 Purchases ............................................. 180,000 Goods available for sale .............................. $200,000 Using these data, estimate the cost of ending inventory for each situation below: (1) Markup is 50 percent on cost. (2) Markup is 60 percent on sales. (3) Markup is 25 percent on cost. (4) Markup is 40 percent on sales. 3 percentage points higher than the one earned in 2004. Salvaged undamaged merchandise was marked to sell at $24,000, while damaged merchandise marked to sell at $16,000 had an estimated net realizable value of $3,600. Determine the company's inventory loss due to the fire that occurred on December 31, 2005. 3. Kingston Company reported the following net income amounts: 209 2002 ........................................ $52,000 2003 ........................................ $38,000 2004 ........................................ $66,000 In 2005, the company discovered errors that been made in computing the ending inventories for 2002 and 2003, as follows: 2002 Ending inventory understated by $4,000. 2003 Ending inventory understated by $8,000. Compute the correct net incomes for (1) 2002, (2) 2003, and (3) 2004. 4. On May 17, it was discovered that a material amount of inventory had been stolen. A physical count discloses that $55,000 of merchandise was on hand as of May 17. The following additional data is available from the accounting records: Inventory, January 1 ................................... $ 62,000 Purchases, January 1 - May 17 (includes $4,000 shipped FOB shipping point May 16, received May 19) .......... 114,000 Sales (goods delivered to customers), January 1 - May 17 90,000 Records indicate that the company's gross profit has averaged 40 percent of selling prices. Estimate the amount of loss due to theft. 5. Boston Company reported the following net income amounts: 210 2002 ...................................... $42,000 2003 ...................................... $67,000 2004 ...................................... $78,000 In 2005, the company discovered errors that had been made in computing the ending inventories for 2002 and 2003, as follows: 2002 Ending inventory overstated by $9,000. 2003 Ending inventory understated by $6,000. Compute the correct net incomes for (1) 2002, (2) 2003, and (3) 2004. 6. The 49ers Company began its operations in early 2005. The company carries five different types of inventory which are listed below along with other relevant data. The company values its inventory at the lower of cost or market. At December 31, 2005, 49ers has exactly one unit of each item in ending inventory. | Estimated | Normal Profit | | Actual | Replacement | Selling | Estimated | Margin on | | Item | Cost | Cost | Price | Cost to Sell | Selling Price 1 $12.00 $13.00 $20.00 $4.00 20% 2 14.00 10.00 10.00 2.00 10% 3 16.00 10.00 20.00 6.00 15% 4 18.00 15.00 24.00 2.00 25% 5 20.00 22.00 30.00 4.00 30% (1) Complete the following information using the lower-of-cost-or-market method as of December 31, 2005. 211 | Item | Ceiling | Floor | Market | LCM | 1 | | | | | 2 | | | | | 3 | | | | | 4 | | | | | 5 | | | | (2) Compute the inventory loss, if any, 49ers should show in 2005 using the lower-ofcost-or-market method applied on an individual items basis. (3) Prepare the adjusting entry, if any, required as of December 31, 2005, assuming all such entries are made directly to the inventory account. 7. The Steelers Company had its entire inventory destroyed when a fire swept through the company's warehouse. Fortunately, the accounting records were locked in a fireproof safe and were not damaged. The following information for the period up to the date of the fire was taken from the accounting records: Sales ................................................. $486,400 Purchases ............................................. 295,000 Beginning inventory ................................... 147,800 Purchase returns ...................................... 16,600 Freight-in ............................................ 8,200 (1) Assuming that the gross profit has averaged 25 percent of selling price, what is the 212 estimated value of the inventory destroyed in the fire? Show all calculations in good form. (2) Assuming that the markup percentage on cost is 28 percent, what is the estimated value of the inventory destroyed in the fire? Show all calculations in good form. 8. Current generally accepted accounting principles state that a departure from the cost basis of pricing inventory is required when the utility of the goods is no longer as great as its cost. Accordingly, the lower-of-cost-or-market rule is applied to inventories such that, if market is less than cost, an adjustment is made to record the loss and to restate ending inventory at the lower value. What effect would the failure to apply the lower-of-cost-or-market method have on the income statement in current and future periods? 9. The inventory account of Duke Company at December 31, 2005, included the following items: Inventory Amount Merchandise out on consignment at sales price (including markup of 35% on selling price) ......... $15,000 Goods purchased, in transit (shipped FOB shipping point) ....................... 6,000 Goods held by Duke on consignment .................... 4,500 Goods out on approval (sales price $6,000, cost $4,000) ....................................... 6,000 213 Based on this information, the inventory account at December 31, 2005, should be reduced by what amount? 10. The following data relate to the first three years of operation for the Lewis Company: 2005 2006 2007 Net income under FIFO ........... $30,000 $45,000 $16,000 Net income under LIFO ........... 12,000 32,000 12,000 Ending inventory under FIFO ..... 55,000 67,000 71,000 Compute the ending inventory under LIFO for each year. (Ignore income taxes.) 11. The following information is available for the Fister Company for 2005: Freight-in ............................................ $ 50,000 Purchase returns ...................................... 185,000 Selling expenses ...................................... 357,000 Ending inventory ...................................... 117,000 The cost of goods sold is equal to 400% of selling expenses. Compute the cost of goods available for sale. 14. Edwards Sporting Goods began operations February 1, 2005. Edwards sells footballs to high schools and colleges throughout the country. The company uses a periodic system. A summary of inventory records for the month of February appears below: Inventory Records--Footballs | Terms of | Units | Gross Price | | Date | Purchase | Received | on Invoice | February 2 February 17 | 3/10, net 30 net 30 | 800 600 | $30,000 22,560 | February 26 | 2/10, net 45 | 550 | 20,490 All footballs are sold for $47.50. Edwards takes all discounts that are offered and uses the net method for recording purchases. On February 28, there were 470 footballs on hand. (1) Compute the ending inventory cost under FIFO. (2) Compute the gross margin on sales under LIFO. (3) Compute the ending inventory cost under LIFO. (4) Give the journal entry to record the February 2 purchase. 15. The Clayton Music Company was formed on December 1, 2004. The following information is available from Clayton's inventory records: Units Unit Cost Balance at January 1, 2005 ................ 4,800 $14.25 Purchases: January 17, 2005 .......................... 9,000 15.00 March 12, 2005 ............................ 7,200 16.50 June 23, 2005 ............................. 3,600 15.75 November 15, 2005 ......................... 5,400 17.25 The company uses a periodic inventory system, and a physical inventory on November 30, 2005, shows 9,600 units on hand. Prepare schedules to compute the ending inventory at November 30, 2005, under each of the following inventory methods: (1) FIFO. (2) LIFO. (3) Average cost. 17. Two reasons often advanced for the adoption of LIFO inventory costing for financial reporting are the improved matching of current costs with current revenue during periods of rising prices and the reduction of income tax payments. Nonetheless, the number of companies using LIFO has not increased over the last several years. Some companies actually have switched from LIFO to FIFO over the last several years. Identify reasons why a company would change from LIFO to FIFO for financial reporting purposes. 18. The following data are available for Castle Gate Company: Unit Units Cost Total Cost | Beginning inventory (base layer of LIFO inventory) ............ | 20,000 | $1.00 | $ 20,000 Purchases ....................... 80,000 $1.50 120,000 Total available for sale ........ 100,000 $140,000 Sales (88,000 units, costed on LIFO basis) from: Purchases 80,000 ............. $1.50 $120,000 Base inventory layer ......... 8,000 $1.00 8,000 Cost of goods sold .............. 88,000 $128,000 Ending inventory ................ 12,000 $1.00 $ 12,000 The company has experienced a temporary LIFO liquidation by not maintaining the base year inventory of 20,000 units. The company uses a perpetual inventory system. Prepare the entries to account for the temporary liquidation and the replacement of the liquidated units assuming that 8,000 units will be replaced at $1.60 per unit 219 [Show More]

Last updated: 1 year ago

Preview 1 out of 44 pages

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Apr 27, 2021

Number of pages

44

Written in

Additional information

This document has been written for:

Uploaded

Apr 27, 2021

Downloads

0

Views

150

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)